短期利率模型之Cox-Ingersoll-Ross模型

前言

上篇文章对Vasicek模型进行了简单的介绍,本偏文章则要对短期利率模型中的Cox-Ingersoll-Ross模型进行介绍

一、Cox-Ingersoll-Ross模型

Cox-Ingersoll-Ross模型是用于解决Vasicek模型出现负利率问题的单因素模型。

Cox-Ingersoll-Ross模型计算公式为(The equation for the CIR model is expressed as follows:)

其中:

rt=Instantaneous interest rate at time t(t时刻的瞬时利率)

a=Rate of mean reversion(回归速度)

b=Mean of the interest rate(长期平均水平。在长期水平下产生一系列r的轨道值)

Wt =Wiener process (random variable modeling the market risk factor/风险中性框架下的维纳过程)

σ=Standard deviation of the interest rate (measure of volatility/标准差参数)

二、Cox-Ingersoll-Ross模型的python量化

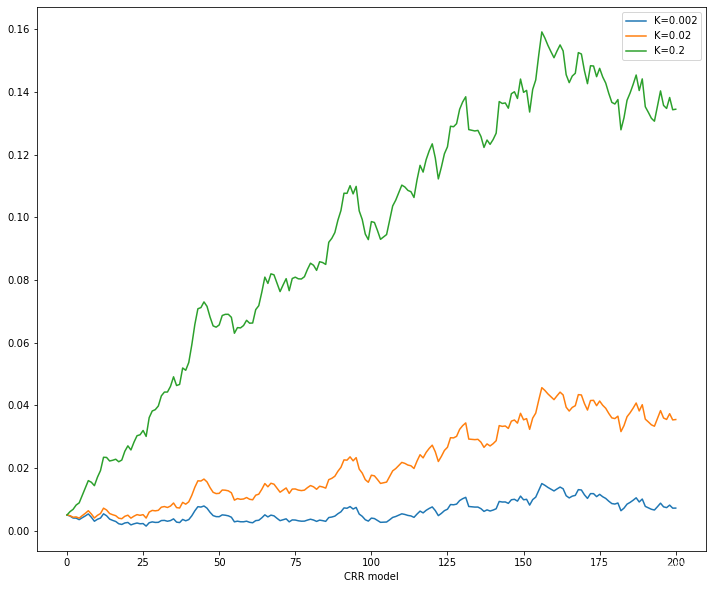

# CIR模型

# CIR模型是用于解决Vasicek模型负利率的问题

import math

import numpy as np

def CIR(r0,K,theta,sigma,T=1,N=10,seed=777):

np.random.seed(seed)

df=T/float(N)

rates=[r0]

for i in range(N):

dr=K*(theta-rates[-1])*dt+sigma*math.sqrt(rates[-1])*math.sqrt(dt)*np.random.normal()

rates.append(rates[-1]+dr)

return range(N+1),rates

import matplotlib.pyplot as plt

plt.figure(figsize=(12,10))

for K in [0.002,0.02,0.2]:

x,y=CIR(0.005,K,0.15,sigma,T=10,N=200,seed=777)

plt.plot(x,y,label='K=%s'%K)

plt.legend(loc=0)

plt.xlabel('CRR model')

总结

本章介绍了Cox-Ingersoll-Ross模型,Cox-Ingersoll-Ross模型是用于解决Vasicek模型出现负利率问题的单因素模型。