data.csv提取码:yccr文件中存储了股票的信息, 其中第4-8列,即EXCEL表格中的D-H列,

分别为股票的开盘价,最高价,最低价,收盘价,成交量。

分析角度:

-

计算成交量加权平均价格

概念:成交量加权平均价格,英文名VWAP(Volume-Weighted Average Price,成交量加权平均价格)是一个非常重要的经

济学量,代表着金融资产的“平均”价格。 某个价格的成交量越大,该价格所占的权重就越大。VWAP就是以成交量为权重计算出来的加权平均值。 -

计算最大值和最小值: 计算股价近期最高价的最大值和最低价的最小值

-

计算股价近期最高价的最大值和最小值的差值;----(极差)

计算股价近期最低价的最大值和最小值的差值 -

计算收盘价的中位数

-

计算收盘价的方差

-

计算对数收益率, 股票收益率、年波动率及月波动率

***收盘价的分析常常是基于股票收益率的。

股票收益率又可以分为简单收益率和对数收益率。

简单收益率:是指相邻两个价格之间的变化率。

对数收益率:是指所有价格取对数后两两之间的差值。

# [1, 2,3 4] ======>[-1, ]

***使用的方法: NumPy中的diff函数可以返回一个由相邻数组元素的差值构成的数组。

不过需要注意的是,diff返回的数组比收盘价数组少一个元素。***在投资学中,波动率是对价格变动的一种度量,历史波动率可以根据历史价格数据计算得出。计算历史波动率时,需要用

到对数收益率。

年波动率等于对数收益率的标准差除以其均值,再乘以交易日的平方根,通常交易日取252天。

月波动率等于对数收益率的标准差除以其均值,再乘以交易月的平方根。通常交易月取12月。 -

获取该时间范围内交易日周一、周二、周三、周四、周五分别对应的平均收盘价

-

平均收盘价最低,最高分别为星期几

import numpy as np

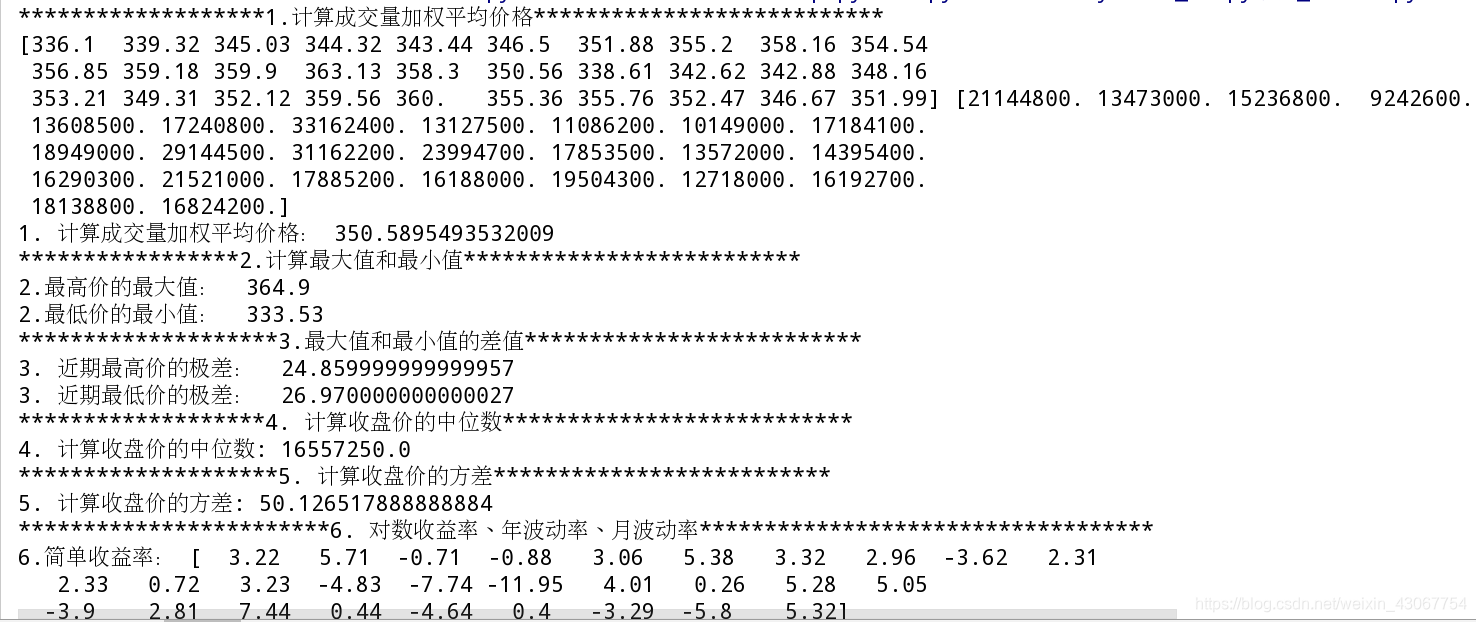

print("*******************1.计算成交量加权平均价格***************************")

params1 = dict(

fname="doc/data.csv",

delimiter=",",

usecols=(6, 7),

unpack=True)

# delimiter 分隔符 usecols 6-7列

# 收盘价,成交量,**params1 解包字典

endPrice, countNum = np.loadtxt(**params1)

# print(endPrice, countNum)

# average加权平均值

VWAP = np.average(endPrice, weights=countNum)

print("1. 计算成交量加权平均价格:", VWAP)

输出:

*******************1.计算成交量加权平均价格***************************

1. 计算成交量加权平均价格: 350.5895493532009

print("*****************2.计算最大值和最小值**************************")

params2 = dict(

fname="doc/data.csv",

delimiter=",",

usecols=(4, 5),

unpack=True)

# 最高价和最低价

highPrice, lowPrice = np.loadtxt(**params2)

# 最高价的最大值和最低价的最小值

print("2.最高价的最大值: ", highPrice.max())

print("2.最低价的最小值: ", lowPrice.min())

输出:

*****************2.计算最大值和最小值**************************

2.最高价的最大值: 364.9

2.最低价的最小值: 333.53

print("********************3.最大值和最小值的差值**************************")

# 计算股价近期最高价的最大值和最小值的差值;----(极差)

# 计算股价近期最低价的最大值和最小值的差值

print("3. 近期最高价的极差: ", np.ptp(highPrice))

print("3. 近期最低价的极差: ", np.ptp(lowPrice))

print("*******************4. 计算收盘价的中位数***************************")

# 计算收盘价的中位数

print("4. 计算收盘价的中位数:", np.median(countNum))

print("********************5. 计算收盘价的方差**************************")

# 计算收盘价的方差

print("5. 计算收盘价的方差:", np.var(endPrice))

输出:

********************3.最大值和最小值的差值**************************

3. 近期最高价的极差: 24.859999999999957

3. 近期最低价的极差: 26.970000000000027

*******************4. 计算收盘价的中位数***************************

4. 计算收盘价的中位数: 16557250.0

********************5. 计算收盘价的方差**************************

5. 计算收盘价的方差: 50.126517888888884

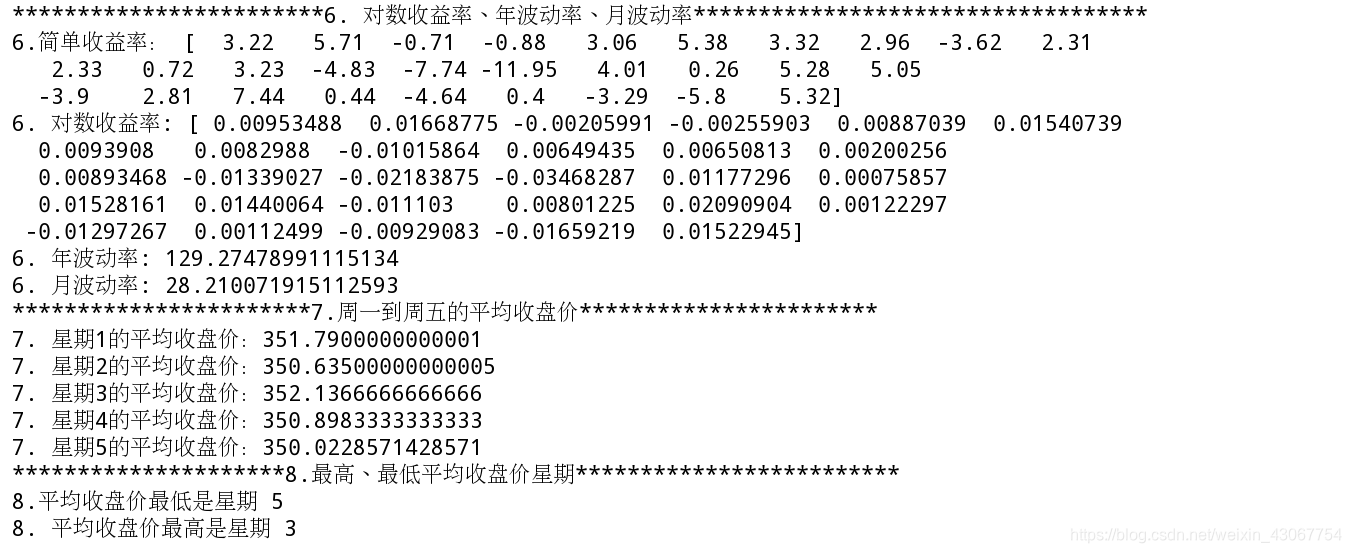

print("************************6. 对数收益率、年波动率、月波动率***********************************")

# 简单收益率:两两之差

simpleReturn = np.diff(endPrice)

print(simpleReturn)

# 对数收益率: 所有价格取对数后两两之间的差值。

logReturn = np.diff(np.log(endPrice))

print("6. 对数收益率:", logReturn)

# 年波动率等于对数收益率的标准差除以其均值,再乘以交易日的平方根,通常交易日取252天。

annual_vol = logReturn.std()/logReturn.mean()*np.sqrt(252)

print("6. 年波动率:", annual_vol)

# 月波动率等于对数收益率的标准差除以其均值,再乘以交易月的平方根。通常交易月取12月。

month_vol = logReturn.std()/logReturn.mean()*np.sqrt(12)

print("6. 月波动率:", month_vol)

输出:

************************6. 对数收益率、年波动率、月波动率***********************************

6.简单收益率: [ 3.22 5.71 -0.71 -0.88 3.06 5.38 3.32 2.96 -3.62 2.31

2.33 0.72 3.23 -4.83 -7.74 -11.95 4.01 0.26 5.28 5.05

-3.9 2.81 7.44 0.44 -4.64 0.4 -3.29 -5.8 5.32]

6. 对数收益率: [ 0.00953488 0.01668775 -0.00205991 -0.00255903 0.00887039 0.01540739

0.0093908 0.0082988 -0.01015864 0.00649435 0.00650813 0.00200256

0.00893468 -0.01339027 -0.02183875 -0.03468287 0.01177296 0.00075857

0.01528161 0.01440064 -0.011103 0.00801225 0.02090904 0.00122297

-0.01297267 0.00112499 -0.00929083 -0.01659219 0.01522945]

6. 年波动率: 129.27478991115134

6. 月波动率: 28.210071915112593

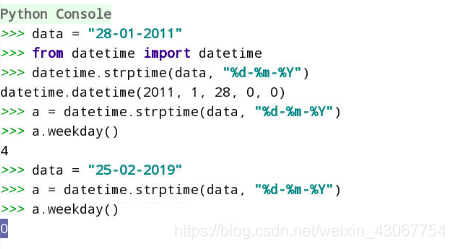

做第七题时需要知道如何获取星期数:

print("***********************7.周一到周五的平均收盘价***********************")

def get_week(date):

"""根据传入的日期28-01-2011获取星期数, 0-星期一"""

from datetime import datetime

# 默认传入的不是字符串, 是bytes类型;

date = date.decode('utf-8')

return datetime.strptime(date, "%d-%m-%Y").weekday()

params3 = dict(

fname="doc/data.csv",

delimiter=",",

usecols=(1, 6),

converters={1: get_week},

unpack=True)

# 星期数和收盘价

week, endPrice = np.loadtxt(**params3)

allAvg = []

for weekday in range(5):

average = endPrice[week == weekday].mean()

allAvg.append(average)

print("7. 星期%s的平均收盘价:%s" % (weekday + 1, average))

输出:

*********************8.最高、最低平均收盘价星期*************************

8.平均收盘价最低是星期 5

8. 平均收盘价最高是星期 3

完整代码:

import numpy as np

print("*******************1.计算成交量加权平均价格***************************")

params1 = dict(

fname="doc/data.csv",

delimiter=",",

usecols=(6, 7),

unpack=True)

# delimiter 分隔符 usecols 6-7列

#

# 收盘价,成交量,**params1 解包字典

endPrice, countNum = np.loadtxt(**params1)

print(endPrice, countNum)

# average加权平均值

VWAP = np.average(endPrice, weights=countNum)

print("1. 计算成交量加权平均价格:", VWAP)

print("*****************2.计算最大值和最小值**************************")

params2 = dict(

fname="doc/data.csv",

delimiter=",",

usecols=(4, 5),

unpack=True)

#

# # 最高价和最低价

highPrice, lowPrice = np.loadtxt(**params2)

#

# # 最高价的最大值和最低价的最小值

print("2.最高价的最大值: ", highPrice.max())

print("2.最低价的最小值: ", lowPrice.min())

print("********************3.最大值和最小值的差值**************************")

# 计算股价近期最高价的最大值和最小值的差值;----(极差)

# 计算股价近期最低价的最大值和最小值的差值

print("3. 近期最高价的极差: ", np.ptp(highPrice))

print("3. 近期最低价的极差: ", np.ptp(lowPrice))

print("*******************4. 计算收盘价的中位数***************************")

# 计算收盘价的中位数

print("4. 计算收盘价的中位数:", np.median(countNum))

print("********************5. 计算收盘价的方差**************************")

# 计算收盘价的方差

print("5. 计算收盘价的方差:", np.var(endPrice))

print("************************6. 对数收益率、年波动率、月波动率***********************************")

# 简单收益率:两两之差

simpleReturn = np.diff(endPrice)

print('6.简单收益率:',simpleReturn)

# 对数收益率: 所有价格取对数后两两之间的差值。

logReturn = np.diff(np.log(endPrice))

print("6. 对数收益率:", logReturn)

# 年波动率等于对数收益率的标准差除以其均值,再乘以交易日的平方根,通常交易日取252天。

annual_vol = logReturn.std()/logReturn.mean()*np.sqrt(252)

print("6. 年波动率:", annual_vol)

# 月波动率等于对数收益率的标准差除以其均值,再乘以交易月的平方根。通常交易月取12月。

month_vol = logReturn.std()/logReturn.mean()*np.sqrt(12)

print("6. 月波动率:", month_vol)

print("***********************7.周一到周五的平均收盘价***********************")

def get_week(date):

"""根据传入的日期28-01-2011获取星期数, 0-星期一"""

from datetime import datetime

# 默认传入的不是字符串, 是bytes类型;

date = date.decode('utf-8')

return datetime.strptime(date, "%d-%m-%Y").weekday()

params3 = dict(

fname="doc/data.csv",

delimiter=",",

usecols=(1, 6),

converters={1: get_week},

unpack=True)

# 星期数和收盘价

week, endPrice = np.loadtxt(**params3)

allAvg = []

for weekday in range(5):

average = endPrice[week == weekday].mean()

allAvg.append(average)

print("7. 星期%s的平均收盘价:%s" % (weekday + 1, average))

print("*********************8.最高、最低平均收盘价星期*************************")

# [12, 23, 34, 45, 56]

print("8.平均收盘价最低是星期", np.argmin(allAvg) + 1)

print("8. 平均收盘价最高是星期", np.argmax(allAvg) + 1)