【Reference】

1. B站:清华计算机博士带你学-Python金融量化分析

2. Tushare 官网(作者ID:492952)

本博客所包含的项目代码基本参考Reference1,并对其中tushare API的更新做了对应的修改。全部代码已上传至作者的 github,下文中仅针对代码思路做一个知识梳理

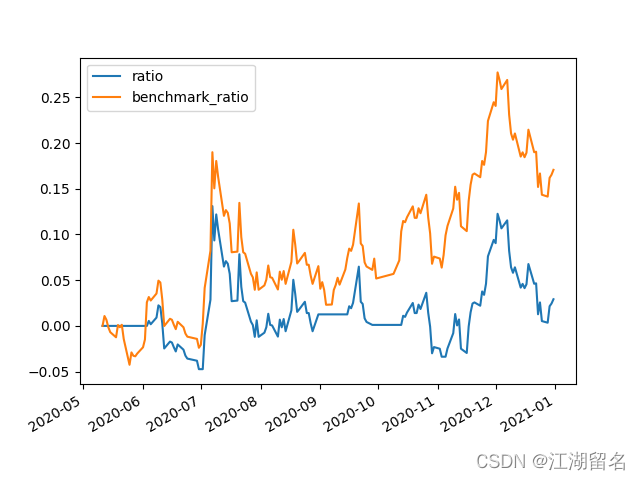

1. 回测需求 & 效果展示

以中国平安(601318.SH)为买卖对象,检验双均线策略在 2020-05-10 至 2021-01-01 的收益情况。效果如下:

2. 代码框架

2.1 对象

(1) 存储账户信息、回测信息

账户信息:现金,所持股票

回测信息:

- 开始/结束日期

- 当前日期

- 基准:一般会以一只股票或一个指数为基准,用于比较策略优劣性

- 开始至结束之间所有交易日的信息

class Context:

def __init__(self, cash, start_date, end_date):

# 账户信息

self.cash = cash # 现金

self.positions = {

} # 持有的股票信息

# 回测信息

self.start_date = start_date

self.end_date = end_date

self.dt = start_date

self.benchmark = None

self.date_range = trade_cal[(trade_cal['is_open'] == '1') & \

(trade_cal['cal_date'] >= start_date) & \

(trade_cal['cal_date'] <= end_date)]['cal_date'].values

其中,trade_cal 存储了所有交易日的日期信息。可通过 tushare 包的 pro.trade_cal() 获取

(2) 存储其他全局变量

class G:

pass

2.2 函数

(0) 主体函数

def run():

initialize(context) # 初始化

# 创建一个DataFrame,储存画图所需数据

plt_df = pd.DataFrame(index=pd.to_datetime(context.date_range), columns=['value'])

# 存储股票的上一个交易日的价格信息,避免以为股票停牌而无法获取价格

last_prices = {

}

# 回测开始时的股票价格,用于计算之后的价格变动曲线

initial_value = context.cash

for dt in context.date_range:

context.dt = dt # 更新当前时间

handle_data(context)

# 计算账户价值 = 现金 + 持仓股票

value = context.cash

for stock in context.positions.keys():

try:

data = get_today_data(stock)

last_prices[stock] = data['open']

except KeyError:

# 如果取不到,说明当日停牌,取上一个交易日的价格

price = last_prices[stock]

value += price * context.positions[stock].amount

plt_df.loc[dt, 'value'] = value

# 绘制策略

plt_df['ratio'] = (plt_df['value'] - initial_value) / initial_value

# 绘制基准

bm_df = attribute_daterange_history(context.benchmark, context.start_date, context.end_date)

bm_init = bm_df['open'][0]

plt_df['benchmark_ratio'] = (bm_df['open'] - bm_init) / bm_init

plt_df[['ratio', 'benchmark_ratio']].plot()

plt.show()

(1) 初始化函数

- 设置目标股票

- 设置基准

- 设置双均线信息(g.p1 & g.p2)

- 获取目标股票的历史数据:在以下代码中,

hist_1获取的是回测开始日期前g.p2天的数据,hist_2获取的是回测开始至结束之间的数据。将两者合并后即可得到双均线回测所需要的所有股票价格数据

def initialize(context):

g.security = '601318.SH'

set_benchmark('601318.SH')

g.p1 = 5

g.p2 = 60

hist_1 = attribute_history(g.security, g.p2)

hist_2 = attribute_daterange_history(g.security, context.start_date, context.end_date)

g.hist = hist_1.append(hist_2)

(2) 每个交易日都需执行的函数

def handle_data(context):

hist = g.hist[:dateutil.parser.parse(context.dt)][-g.p2:]

ma5 = hist['close'][-g.p1:].mean()

ma60 = hist['close'].mean()

# 实现双均线策略:

# 如果短均线高于长均线,且股票不在持仓中,则买入

# 反之,且股票在持仓中,则卖出

if ma5 > ma60 and g.security not in context.positions.keys():

order_value(g.security, context.cash)

elif ma5 < ma60 and g.security in context.positions.keys():

order_target(g.security, 0)

(3) 下单函数

github 中上传的代码共包含四个下单函数:

order: 购买一定的股票数量order_value购买一定的股票金额order_target购买到一定数量的股票order_target_value购买到一定金额的股票

而这四个下单函数均基于:

def _order(today_data, security, amount):

if today_data.empty: return

# 获取股票价格

price = today_data['open']

# 判断是否持有该股票

try:

test = context.positions[security]

except KeyError:

# 如果卖出操作,直接退出函数

if amount <= 0: return

# 如果买入操作,创建position

context.positions[security] = pd.Series(dtype=float)

context.positions[security]['amount'] = 0

# 买入/卖出操作时,必须以100的倍数购买,除非全部卖出

if (amount % 100 != 0) and (amount != -context.positions[security].amount):

amount = int(amount/100) * 100

# 更新持仓

context.positions[security].amount = context.positions[security].get('amount') + amount

if context.positions[security].amount == 0: # 如果持仓股数为0,删除

del context.positions[security]

# 更新现金

context.cash -= amount * price