标注说明

ff表示预测值,yy表示实际值

评价指标

- MAE(Mean Absolute Error) 平均绝对误差

MAE=1n∑i=1n|fi−yi|MAE=1n∑i=1n|fi−yi| - MSE(Mean Square Error) 平均平方差/均方误差是回归任务最常用的性能度量。

MSE=1n∑i=1n(fi−yi)2MSE=1n∑i=1n(fi−yi)2 RMSE(Root Mean Square Error) 方均根差

RMSE=MSE−−−−−√RMSE=MSE

缺点:因为它使用的是平均误差,而平均误差对异常点较敏感,如果回归器对某个点的回归值很不合理,那么它的误差则比较大,从而会对RMSE的值有较大影响,即平均值是非鲁棒的。MAPE

全称是Mean Absolute Percentage Error(WikiPedia), 也叫mean absolute percentage deviation (MAPD),在统计领域是一个预测准确性的衡量指标。MAPE=100n∑t=1n|yi−fiyi|MAPE=100n∑t=1n|yi−fiyi|R平方

y¯y¯表示观测数据的平均值

残差平方和SSres=∑(yi−fi)2SSres=∑(yi−fi)2

总平均值

SStot=∑(yi−y¯)2SStot=∑(yi−y¯)2

R平方

r2=1−SSresSStot=1−∑(yi−fi)2∑(yi−y¯)2r2=1−SSresSStot=1−∑(yi−fi)2∑(yi−y¯)2

R平方是多元回归中的回归平方和占总平方和的比例,它是度量多元回归方程中拟合程度的一个统计量,反映了在因变量yy的变差中被估计的回归方程所解释的比例。

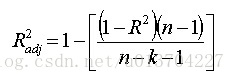

R平方越接近1,表明回归平方和占总平方和的比例越大,回归线与各观测点越接近,用xx的变化来解释yy值变差的部分就越多,回归的拟合程度就越好。校正R平方

http://www.statisticshowto.com/adjusted-r2/where: N is the number of points in your data sample.

K is the number of independent regressors, i.e. the number of variables in your model, excluding the constantRMSPE

RMSPE=1n∑i=1n(yi−y^iyi)2−−−−−−−−−−−−−−−⎷RMSPE=1n∑i=1n(yi−y^iyi)2

where yiyi denotes the sales of a single store on a single day and y^iy^i denotes the corresponding prediction.

https://www.kaggle.com/cast42/xgboost-in-python-with-rmspe-v2/code

- RMSLE(Root Mean Squared Logarithmic Error) Kaggle 上用的一个指标https://www.kaggle.com/wiki/RootMeanSquaredLogarithmicError

def rmsle(predicted,real):

sum=0.0

for x in range(len(predicted)):

p = np.log(predicted[x]+1)

r = np.log(real[x]+1)

sum = sum + (p - r)**2

return (sum/len(predicted))**0.5- 1

- 2

- 3

- 4

- 5

- 6

- 7

# https://www.kaggle.com/jpopham91/rmlse-vectorized

# vectorized error calc

def rmsle(y, y0):

assert len(y) == len(y0)

return np.sqrt(np.mean(np.power(np.log1p(y)-np.log1p(y0), 2)))