原创文章第93篇,专注“个人成长与财富自由、世界运作的逻辑, AI量化投资”。

今天要说说强化学习。

强化学习个人认为,是最契合金融投资的范式。它其实不是一个具体的算法,而是一种范式。

与监督学习不同,监督学习是“一次性”的,有明确的标签。而类比人类的学习,我们不会拿1万张猫的图片让孩子学习什么是猫,一个小朋友也许只见过几只猫,他几乎可以认出各种图片的,抽象的,卡通的猫。人脑的学习是激励-反馈机制。你做一个动作,得到一个正反馈就可以强化这个动作,如果得到负反馈,则弱化这个动作。

我们学骑自行车,并不会用物理学的公式,去计算,人体和地面的角度,手臂要如何发力,而是骑就是了,自行车和地面给你反馈,你随之调整。

简言之,智能体通过与环境交互,得到即时反馈,来调整自己的动作,直到学会某个技能。——这样的学习范式的通过的。所以有了alpha go, alpha master和alpha zero这样的围棋大师,然后它们的技能迁移的打战略游戏上,也是一等一的好手,都拜强化学习所赐。

昨天我们讲的DNN的模式,我们是让模型学习过去的因子“预测”当天的收盘价的“涨跌”。但现实交易过程中,我们就不会因为判断今天会涨就买入,而明天会跌就卖出吧。

投资是一个系列的决策,寻找是一段时间内的收益率,而不是某一天或某几天的涨与跌。这种多轮博弈,而且带有成本的多轮博弈,使用强化学习再适合不过了。

01 强化学习

导入一般常规配置:

import os

import math

import random

import numpy as np

import pandas as pd

from pylab import plt, mpl

plt.style.use('seaborn')

mpl.rcParams['savefig.dpi'] = 300

mpl.rcParams['font.family'] = 'serif'

np.set_printoptions(precision=4, suppress=True)

os.environ['PYTHONHASHSEED'] = '0'

实现一个观察空间类,这是一个N维向量,n的维度等于我们因子的个数。

class observation_space:

def __init__(self, n):

self.shape = (n,)

动作空间,这里动作空间是2(买,卖)

class action_space:

def __init__(self, n):

self.n = n

def seed(self, seed):

pass

def sample(self):

return random.randint(0, self.n - 1)

模似交易环境:

交易环境除了准备交易数据之外,最重要的就是step函数,我们这里的reward仍然与昨天的DNN类似,智能体猜中一次,则奖励加1分。

准确率低于47.5%时退出,或者一个episode结束时退出。

相当于我们做一个交易游戏,一个智能体进来“猜”,猜中加1分,计算准确率,低于47.5%直接出局。

class Finance:

url = 'http://hilpisch.com/aiif_eikon_eod_data.csv'

def __init__(self, symbol, features):

self.symbol = symbol

self.features = features

self.observation_space = observation_space(4)

self.osn = self.observation_space.shape[0]

self.action_space = action_space(2)

self.min_accuracy = 0.475

self._get_data()

self._prepare_data()

def _get_data(self):

self.raw = pd.read_csv(self.url, index_col=0,

parse_dates=True).dropna()

def _prepare_data(self):

self.data = pd.DataFrame(self.raw[self.symbol])

self.data['r'] = np.log(self.data / self.data.shift(1))

self.data.dropna(inplace=True)

self.data = (self.data - self.data.mean()) / self.data.std()

self.data['d'] = np.where(self.data['r'] > 0, 1, 0)

def _get_state(self):

return self.data[self.features].iloc[

self.bar - self.osn:self.bar].values

def seed(self, seed=None):

pass

def reset(self):

self.treward = 0

self.accuracy = 0

self.bar = self.osn

state = self.data[self.features].iloc[

self.bar - self.osn:self.bar]

return state.values

def step(self, action):

correct = action == self.data['d'].iloc[self.bar]

reward = 1 if correct else 0

self.treward += reward

self.bar += 1

self.accuracy = self.treward / (self.bar - self.osn)

if self.bar >= len(self.data):

done = True

elif reward == 1:

done = False

elif (self.accuracy < self.min_accuracy and

self.bar > self.osn + 10):

done = True

else:

done = False

state = self._get_state()

info = {}

return state, reward, done, info

智能体的实现DRL:

def set_seeds(seed=100):

random.seed(seed)

np.random.seed(seed)

env.seed(seed)

set_seeds(100)

from collections import deque

from keras.optimizers import Adam, RMSprop

from keras.layers import Dense, Dropout

from keras.models import Sequential

from keras.optimizers import Adam, RMSprop

from sklearn.metrics import accuracy_score

from tensorflow.python.framework.ops import disable_eager_execution

disable_eager_execution()

class DQLAgent:

def __init__(self, gamma=0.95, hu=24, opt=Adam,

lr=0.001, finish=False):

self.finish = finish

self.epsilon = 1.0

self.epsilon_min = 0.01

self.epsilon_decay = 0.995

self.gamma = gamma

self.batch_size = 32

self.max_treward = 0

self.averages = list()

self.memory = deque(maxlen=2000)

self.osn = env.observation_space.shape[0]

self.model = self._build_model(hu, opt, lr)

def _build_model(self, hu, opt, lr):

model = Sequential()

model.add(Dense(hu, input_dim=self.osn,

activation='relu'))

model.add(Dense(hu, activation='relu'))

model.add(Dense(env.action_space.n, activation='linear'))

model.compile(loss='mse', optimizer=opt(lr=lr))

return model

def act(self, state):

if random.random() <= self.epsilon:

return env.action_space.sample()

action = self.model.predict(state)[0]

return np.argmax(action)

def replay(self):

batch = random.sample(self.memory, self.batch_size)

for state, action, reward, next_state, done in batch:

if not done:

reward += self.gamma * np.amax(

self.model.predict(next_state)[0])

target = self.model.predict(state)

target[0, action] = reward

self.model.fit(state, target, epochs=1,

verbose=False)

if self.epsilon > self.epsilon_min:

self.epsilon *= self.epsilon_decay

def learn(self, episodes):

trewards = []

for e in range(1, episodes + 1):

state = env.reset()

state = np.reshape(state, [1, self.osn])

for _ in range(5000):

action = self.act(state)

next_state, reward, done, info = env.step(action)

next_state = np.reshape(next_state,

[1, self.osn])

self.memory.append([state, action, reward,

next_state, done])

state = next_state

if done:

treward = _ + 1

trewards.append(treward)

av = sum(trewards[-25:]) / 25

self.averages.append(av)

self.max_treward = max(self.max_treward, treward)

templ = 'episode: {:4d}/{} | treward: {:4d} | '

templ += 'av: {:6.1f} | max: {:4d}'

print(templ.format(e, episodes, treward, av,

self.max_treward), end='\r')

break

if av > 195 and self.finish:

print()

break

if len(self.memory) > self.batch_size:

self.replay()

def test(self, episodes):

trewards = []

for e in range(1, episodes + 1):

state = env.reset()

for _ in range(5001):

state = np.reshape(state, [1, self.osn])

action = np.argmax(self.model.predict(state)[0])

next_state, reward, done, info = env.step(action)

state = next_state

if done:

treward = _ + 1

trewards.append(treward)

print('episode: {:4d}/{} | treward: {:4d}'

.format(e, episodes, treward), end='\r')

break

return trewards

重点关注learn函数:

每个episode跑5000次,遇到失败会退出。DRL有重放机制,这个我们系统讲强化学习算法的时候再说。

训练这个模型花了22分钟。

02 DRL应用于投资实战

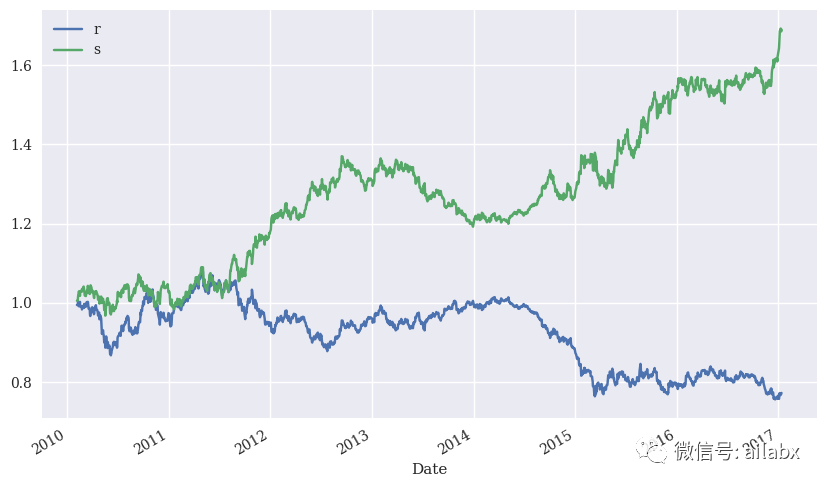

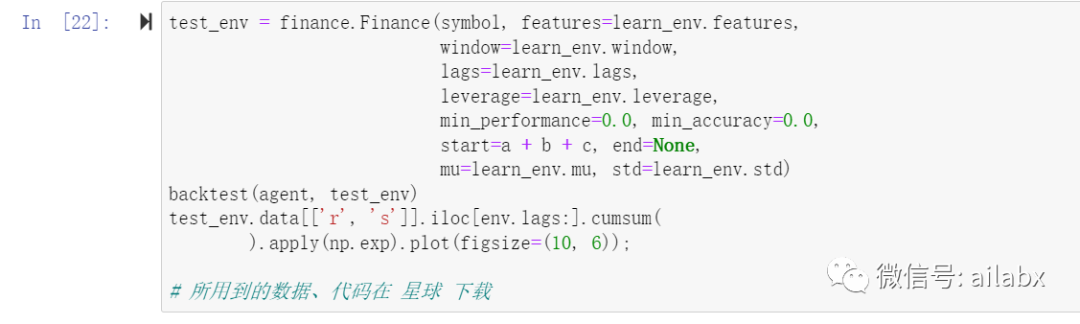

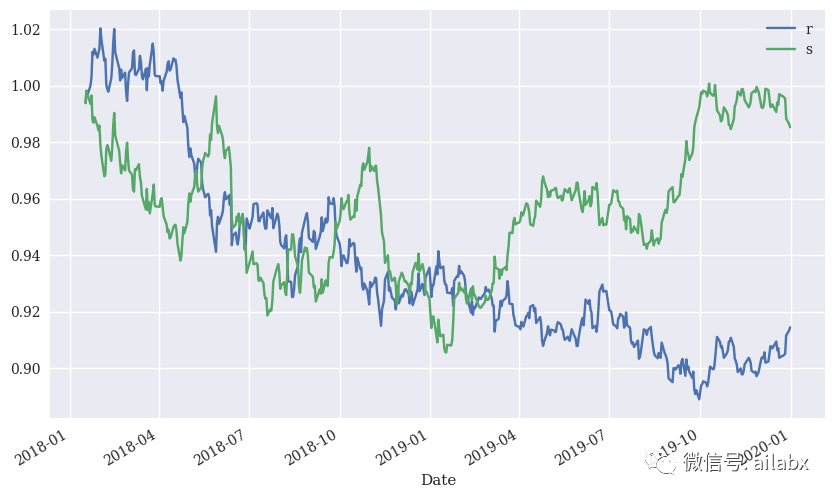

样本内的表现还是不错的,我们再来看样本外的表现情况:

还可以,注意这里未考虑手续费。

小结:

本文重在演示强化学习如何作用于金融时间序列数据,这个方向一定是可行,而且应该深入探讨的。