目标和背景

采用逻辑回归方法,使用过去 5 天的收益率 X 来预测未来一天的涨跌 Y,

并依据涨跌概率大小来构建多空投资组合。

解决方案和程序

- 拟合模型:将其中 450 天数据作为训练样本,拟合一个逻辑回归模型,得

到参数估计。用最后 50 天数据作为预测样本,用于检验模型效果。 - 计算信息系数:检验样本中股票涨跌的预测和实际涨跌的相关系数大约为

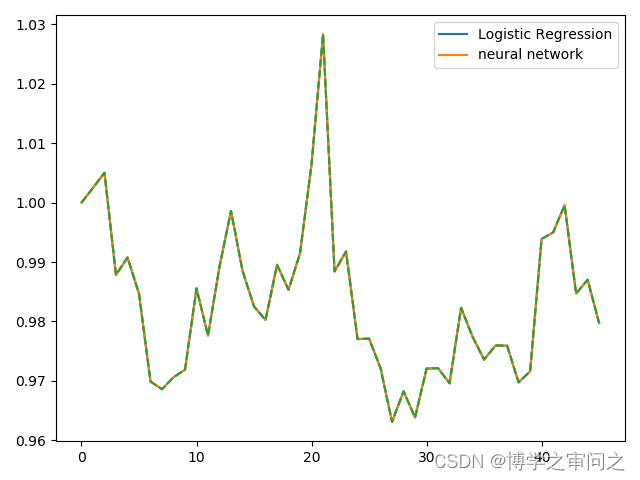

0.077,即信息系数,用来度量因子或因子组合的好坏。 - 构建多空投资组合:等比例持有预测上涨概率最大的 10 支股票,做空上

涨概率最小的 10 支股票,画出组合收益图。

参考代码:

import numpy as np

import numpy.linalg as la

import pandas as pd

import os

import matplotlib.pyplot as plt

index_path = r’data\SZ399300.TXT’

index300 = pd.read_table(index_path,

encoding = ‘cp936’,header = None)

idx = index300[:-1]

idx.columns = [‘date’,‘o’,‘h’,‘l’,‘c’,‘v’,‘to’]

idx.index = idx[‘date’]

stock_path = r’data\hs300’

names = os.listdir(stock_path)

close = []

for name in names:

spath = stock_path + ‘\’ + name

df0 = pd.read_table(spath,

encoding = ‘cp936’,header = None)

df1 = df0[:-1]

df1.columns = [‘date’,‘o’,‘h’,‘l’,‘c’,‘v’,‘to’]

df1.index = df1[‘date’]

df2 = df1.reindex(idx.index,method = ‘ffill’)

df3 = df2.fillna(method = ‘bfill’)

close.append(df3[‘c’].values)

data = np.asarray(close).T

retx = (data[1:,:]-data[:-1,:])/data[:-1,:]

n = 500

n1 = 50

p = 5

train = retx[-n:-n1,:]

ret = train[p:,:].ravel()

X1 = train[4:-1,:].ravel()[:,np.newaxis]

X2 = train[3:-2,:].ravel()[:,np.newaxis]

X3 = train[2:-3,:].ravel()[:,np.newaxis]

X4 = train[1:-4,:].ravel()[:,np.newaxis]

X5 = train[:-5,:].ravel()[:,np.newaxis]

y_train = (ret>0).astype(int)

X_train = np.hstack((X5,X4,X3,X2,X1))

test = retx[-n1:,:]

ret2 = test[p:,:].ravel()

X1 = test[4:-1,:].ravel()[:,np.newaxis]

X2 = test[3:-2,:].ravel()[:,np.newaxis]

X3 = test[2:-3,:].ravel()[:,np.newaxis]

X4 = test[1:-4,:].ravel()[:,np.newaxis]

X5 = test[:-5,:].ravel()[:,np.newaxis]

y_test = (ret2>0).astype(int)

X_test = np.hstack((X5,X4,X3,X2,X1))

from sklearn import linear_model

from sklearn.metrics import classification_report

clf = linear_model.LogisticRegression(C=1e2,fit_intercept=True)

clf.fit(X_train,y_train)

y_pred0 = clf.predict(X_train)

print(classification_report(y_train, y_pred0))

np.corrcoef([y_train,y_pred0])

y_pred = clf.predict(X_test)

from sklearn.metrics import classification_report

print(classification_report(y_test, y_pred))

np.corrcoef([y_test,y_pred]) # Information Coefficient, IC

holding_matrix = np.zeros((n1-p,300))

for j in range(n1-p):

#prob = clf.predict_proba(test[j:j+5,:].T)[:,1]

prob = clf.predict_proba(test[j:j+p,:].T)[:,1]

long_position = prob.argsort()[-10:]

short_position = prob.argsort()[:10]

holding_matrix[j,long_position] = 0.05

holding_matrix[j,short_position] = -0.05

tmp_ret = np.sum(holding_matrix*test[p:],axis = 1)

portfolio_ret = np.append(0,tmp_ret)

plt.plot(np.cumprod(1+portfolio_ret))

plt.legend([‘Performance of LR’],loc=‘upper left’)

plt.savefig(r’fig\stockret-lr’)

plt.plot(np.cumprod(1+portfolio_ret))

plt.plot(np.cumprod(1+portfolio_ret),‘–’)

plt.legend([‘Logistic Regression’,‘neural network’])

plt.savefig(r’fig\stockret-lrnn’)

plt.show()

运行结果: