以下内容笔记出自‘跟着迪哥学python数据分析与机器学习实战’,外加个人整理添加,仅供个人复习使用。

基于信用卡交易记录数据建立分类模型预测哪些交易是正常的,哪些交易是异常的。

流程:

- 加载数据,观察问题;

- 针对问题给出解决方案;

- 数据集切分;

- 逻辑回归模型;

导入数据

import pandas as pd

import matplotlib.pyplot as plt

import numpy as np

%matplotlib inline

file=r'creditcard.csv'

data=pd.read_csv(file)

print(data.shape)

data.head(6)

目标是分类模型,首先查看标签分布:

#查看标签分布

count_classes=pd.value_counts(data['Class'],sort=True).sort_index()

#pd.value_counts()函数要比转换为dataframe在sort.values()简洁

count_classes.plot(kind='bar') #pandas自带作图函数

plt.xlabel('Class')

plt.ylabel('Frequency')

数据标准化

观察数据特征,列Amount值数量级较大,其余列均0-1,对其进行标准化。

from sklearn.preprocessing import StandardScaler

data['normAmount']=StandardScaler().fit_transform(data['Amount'].values.reshape(-1,1))

data=data.drop(['Time','Amount'],axis=1)

data.head(2)

数据下采样方案

data['Class'].value_counts()

0 284315

1 492

Name: Class, dtype: int64

由于数据标签很不平衡,建立的模型有偏,进行下采样。

X=data.iloc[:,data.columns!='Class']

y=data.iloc[:,data.columns=='Class']

#得到所有标签为1(异常)样本的索引

num_fraud=len(data[data.Class==1])

fraud_index=np.array(data[data.Class==1].index)

#得到标签为0(正常)样本的索引

normal_index=data[data.Class==0].index

#在正常样本中随机采样出指定个数的样本,并取其索引

random_nor_index=np.random.choice(normal_index,num_fraud,replace=True)

random_nor_index=np.array(random_nor_index)

#合并所有正常和异常样本的索引,并提取数据

under_sample_index=np.concatenate([fraud_index,random_nor_index])

under_sample_data=data.iloc[under_sample_index,:]

X_undersample=under_sample_data.iloc[:,under_sample_data.columns!='Class']

y_undersample=under_sample_data.iloc[:,under_sample_data.columns=='Class']

#下采样样本比例

print('正常样本比例:',len(under_sample_data[under_sample_data.Class==0])/len(under_sample_data))

print('异常样本比例:',len(under_sample_data[under_sample_data.Class==1])/len(under_sample_data))

print('下采样总样本量:',len(under_sample_data))

正常样本比例: 0.5

异常样本比例: 0.5

下采样总样本量: 984

建立模型

#Recall=TP(TP+FN)

from sklearn.model_selection import train_test_split

from sklearn.linear_model import LogisticRegression

from sklearn.model_selection import KFold,cross_val_score #交叉验证

from sklearn.metrics import confusion_matrix,recall_score,classification_report

from sklearn.model_selection import cross_val_predict

分割数据集

由于模型测试时使用的测试集是原始数据切分出来的测试集,而不是下采样数据切分的数据集,因此要对原始数据和下采样数据都进行切分

X_train,X_test,y_train,y_test=train_test_split(X,y,test_size=0.3,random_state=0)

print('原始训练集:',X_train.shape)

print('原始测试集:',X_test.shape)

print('原始样本:',data.shape)

X_train_under,X_test_under,y_train_under,y_test_under=\

train_test_split(X_undersample,y_undersample,

test_size=0.3,random_state=0)

print('下采样训练集:',X_train_under.shape)

print('下采样测试集:',X_test_under.shape)

print('下采样样本:',under_sample_data.shape)

原始训练集: (199364, 29)

原始测试集: (85443, 29)

原始样本: (284807, 30)

下采样训练集: (688, 29)

下采样测试集: (296, 29)

下采样样本: (984, 30)

使用下采样数据建模

定义交叉验证函数

交叉验证是为了找到更合适参数的求稳操作,是对下采样训练集进行分割

正则化参数的选择:

- LogisticRegession默认带了正则项,可选择l1或l2,默认l2。调参时,主要目的是解决过拟合,一般选择l2即可。若l2正则化还是过拟合,或特征非常多,希望一些不重要的特征系数归零,让模型系数稀疏化时,可以l1正则。

import numpy as np

from sklearn.model_selection import KFold

'''

交叉验证分割数据过程

'''

a=data.loc[:,['V1','V2']][0:6]

b=data.loc[:,'Class'][0:6]

print(a.shape,b.shape)

kfold=KFold(3,shuffle=True)

index=kfold.split(X=a,y=b)

for train,test in index:

print(a.iloc[train],'\n',a.iloc[test])

使用l2正则惩罚项,并选取不同参数进行建模

import warnings

warnings.filterwarnings('ignore')

'''利用cross_val_score函数'''

c_param_range=[0.01,0.1,1,10,100]

for c in c_param_range:

lr=LogisticRegression(C=c,penalty='l2',random_state=0)

scores=cross_val_score(lr,X_train_under,y_train_under,cv=5,

scoring='accuracy')

#scoring参数:accuracy,roc_auc

mean_score=np.mean(scores)

print((c,mean_score))

(0.01, 0.9317359568390987)

(0.1, 0.9288268274621814)

(1, 0.9273669734475828)

(10, 0.921548714693748)

(100, 0.9200888606791494)

在sklearn工具包中,C参数的意义正好是倒过来的,C=0.01表示正则化力度比较大,而C=100表示力度较小。(一定要参考API文档)

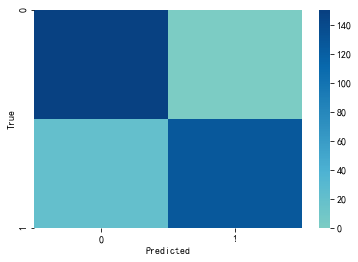

下采样数据-混淆矩阵

lr=LogisticRegression(C=0.01,penalty='l2')

lr.fit(X_train_under,y_train_under)

y_pred=lr.predict(X_test_under)

#混淆矩阵

cm=confusion_matrix(y_test_under,y_pred)

cm

#混淆矩阵第一个参数是行标,第二个参数是列标

array([[148, 1],

[ 20, 127]], dtype=int64)

确定行列标的方式

#确定混淆矩阵的行列标

print(y_test_under.Class.value_counts())

pd.DataFrame(y_pred).iloc[:,0].value_counts()

0 149

1 147

Name: Class, dtype: int64

0 168

1 128

Name: 0, dtype: int64

作图:

import seaborn as sns

plt.figure(figsize=(6,4))

plt.rcParams['font.sans-serif']='SimHei'

sns.heatmap(cm,cmap='GnBu',vmin=0,vmax=150,

annot=False,center=True,fmt='.0f')

plt.xlabel('Predicted')

plt.ylabel('True')

plt.show()

#召回率

recall=cm[1,1]/(cm[1,0]+cm[1,1])

recall

0.8639455782312925

阈值对结果的影响

#用最好的参数建模

lr=LogisticRegression(C=0.01,penalty='l2')

#下采样数据训练模型

lr.fit(X_train_under,y_train_under)

#预测值

y_pred_prob=lr.predict_proba(X_test_under)

#指定不同阈值

thresholds=[0.1,0.2,0.3,0.4,0.5,0.6,0.7,0.8,0.9]

plt.figure(figsize=(10,10))

j=1

for i in thresholds:

y_test_pre_high_recall=y_pred_prob[:,1]>i #得出的是True和False数据

#plt.subplot(3,3,j)

j+=1

cm=confusion_matrix(y_test_under,y_test_pre_high_recall)

print('阈值为',i,'时的召回率',cm[1,1]/(cm[1,0]+cm[1,1]))

#sns.heatmap(cm,cmap='GnBu',annot=True)

#plt.xlabel('Predicted')

#plt.ylabel('True')

print(cm)

原始数据建模结果

lr=LogisticRegression(C=0.01,penalty='l2')

lr.fit(X_train,y_train)

y_pred=lr.predict(X_test)

cm2=confusion_matrix(y_test,y_pred)

print('召回率',cm2[1,1]/(cm2[1,0]+cm2[1,1]))

sns.heatmap(cm2,cmap='GnBu')

plt.xlabel('Predicted')

plt.ylabel('True')

plt.show()

过采样策略

同样可以采用过采样策略进行建模

import pandas as pd

from imblearn.over_sampling import SMOTE

from sklearn.metrics import confusion_matrix

from sklearn.model_selection import train_test_split

features=data.iloc[:,data.columns!='Class']

labels=data['Class']

print(features.shape)

print(labels.shape)

(284807, 29)

(284807,)

features_train,features_test,labels_train,labels_test=train_test_split(features,labels,

test_size=0.3,

random_state=0)

利用SMOTE算法进行样本生成,正例和负例样本数量一致

oversampler=SMOTE(random_state=0)

os_features,os_labels=oversampler.fit_sample(features_train,labels_train)

print(len(os_labels[os_labels==0]))

print(len(os_labels[os_labels==1]))

199019

199019

建立模型

import warnings

warnings.filterwarnings('ignore')

'''利用cross_val_score函数'''

c_param_range=[0.01,0.1,1,10,100]

for c in c_param_range:

lr=LogisticRegression(C=c,penalty='l2',random_state=0)

scores=cross_val_score(lr,os_features,os_labels,cv=5,

scoring='accuracy')

#scoring参数:accuracy,roc_auc

mean_score=np.mean(scores)

print((c,mean_score))

(0.01, 0.9442515545639256)

(0.1, 0.9450153010987146)

(1, 0.945188651552278)

(10, 0.9452162870604811)

(100, 0.94522633639644)

选择最好参数建模

lr=LogisticRegression(C=1,penalty='l2')

lr.fit(os_features,os_labels)

y_pred=lr.predict(features_test)

cm=confusion_matrix(labels_test,y_pred)

print(cm)

print('召回率',cm[1,1]/(cm[1,0]+cm[1,1]))

print('准确率',lr.score(features_test,labels_test))

sns.heatmap(cm,cmap='GnBu')