历史股价分析-python

今天,我们来讲解一个利用numpy 进行历史股价分析的实例

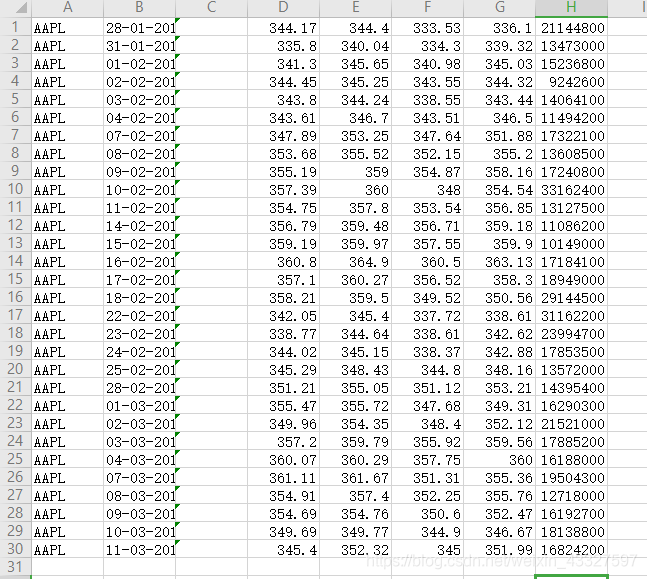

这里用到了一个data.csv的文件,分别有成交日期,开市价,成交最高值,成交最低值,收市价

下面,我们就来对这个股票信息文件进行统计

首先我们先读取数据

###利用NumPy进行历史股价分析

import sys

#读入文件

c,v=np.loadtxt('data.csv', delimiter=',', usecols=(6,7), unpack=True)这里就把文件的第七列数据和第八列数据赋值给c和v

下面进行相关统计量分分析

#计算成交量加权平均价格

vwap = np.average(c, weights=v)print( "VWAP =", vwap)

#算术平均值函数

print( "mean =", np.mean(c))

#时间加权平均价格

t = np.arange(len(c))

print( "twap =", np.average(c, weights=t))

#寻找成交价格最大值和最小值

h,l=np.loadtxt('data.csv', delimiter=',', usecols=(4,5), unpack=True)

print( "highest =", np.max(h))

print( "lowest =", np.min(l))

print( (np.max(h) + np.min(l)) /2)

print( "Spread high price", np.ptp(h))#求取值范围,极差,最大值减最低值

print( "Spread low price", np.ptp(l))统计分析

求中位数和方差

#统计分析

c=np.loadtxt('data.csv', delimiter=',', usecols=(6,), unpack=True)

print( "median =", np.median(c))#求中位数,收盘价

sorted = np.msort(c)

print( "sorted =", sorted)

N = len(c)

print( "middle =", sorted[(N - 1)/2])

print( "average middle =", (sorted[N /2] + sorted[(N - 1) / 2]) / 2)

print( "variance =", np.var(c)))#方差

print( "variance from definition =", np.mean((c - c.mean())**2))#方差计算公式股票收益率分析

#股票收益率

c=np.loadtxt('data.csv', delimiter=',', usecols=(6,), unpack=True) #收盘价

returns = np.diff( c ) / c[ : -1]#股票收益率

print( "Standard deviation =", np.std(returns))

logreturns = np.diff( np.log(c) ) #对数收益率

posretindices = np.where(returns > 0)#收易率大于0

print( "Indices with positive returns", posretindices)

annual_volatility = np.std(logreturns)/np.mean(logreturns)

annual_volatility = annual_volatility / np.sqrt(1./252.)

print( "Annual volatility", annual_volatility) #年度波动率

print( "Monthly volatility", annual_volatility * np.sqrt(1./12.))#月度波动率日期分析

#日期分析

from datetime import datetime

# Monday 0# Tuesday 1# Wednesday 2

# Thursday 3# Friday 4# Saturday 5# Sunday 6

def datestr2num(s):

return datetime.strptime(s, "%d-%m-%Y").date().weekday() #日期格式转换

dates, close=np.loadtxt('data.csv', delimiter=',', usecols=(1,6),

converters={1: datestr2num}, unpack=True)

print( "Dates =", dates) #将日期转换成0-6

averages = np.zeros(5)

for i in range(5):

indices = np.where(dates == i)

prices = np.take(close, indices)

avg = np.mean(prices)

print( "Day", i, "prices", prices, "Average", avg) #求出各个工作日的收盘价,和平均收盘价

averages[i] = avg

top = np.max(averages)

print( "Highest average", top)#最高均值

print( "Top day of the week", np.argmax(averages)) #一周中的·第几天

bottom = np.min(averages)

print( "Lowest average", bottom)#最低均值

print( "Bottom day of the week", np.argmin(averages))周汇总

#周汇总

def datestr2num(s):

return datetime.strptime(s, "%d-%m-%Y").date().weekday()

dates, open, high, low, close=np.loadtxt('data.csv', delimiter=',', usecols=(1, 3, 4, 5, 6), converters={1: datestr2num}, unpack=True)

close = close[:16]

dates = dates[:16]

# get first Monday

first_monday = np.ravel(np.where(dates == 0))[0]

print( "The first Monday index is", first_monday)

# get last Friday

last_friday = np.ravel(np.where(dates == 4))[-1]

print( "The last Friday index is", last_friday)

weeks_indices = np.arange(first_monday, last_friday + 1)

print( "Weeks indices initial", weeks_indices)

weeks_indices = np.split(weeks_indices, 3)

print( "Weeks indices after split", weeks_indices)

def summarize(a, o, h, l, c):

monday_open = o[a[0]]

week_high = np.max( np.take(h, a) )

week_low = np.min( np.take(l, a) )

friday_close = c[a[-1]]

return("APPL", monday_open, week_high, week_low, friday_close)

weeksummary = np.apply_along_axis(summarize, 1, weeks_indices, open, high, low, close)

print( "Week summary", weeksummary) #周汇总数据,成交最高价,成交最低价

np.savetxt("weeksummary.csv", weeksummary, delimiter=",", fmt="%s") 真实波动幅度均值

#真实波动幅度均值

h, l, c = np.loadtxt('data.csv', delimiter=',', usecols=(4, 5, 6), unpack=True)

N =20

h = h[-N:]

l = l[-N:]

print( "len(h)", len(h), "len(l)", len(l))

print( "Close", c)previousclose = c[-N -1: -1]

print( "len(previousclose)", len(previousclose))

print( "Previous close", previousclose)

truerange = np.maximum(h - l, h - previousclose, previousclose - l)

print( "True range", truerange) atr = np.zeros(N) atr[0] = np.mean(truerange)

for i in range(1, N):

atr[i] = (N - 1) * atr[i - 1] + truerange[i]

atr[i] /= N

print( "ATR", atr)指数移动平均线

x = np.arange(5)

print( "Exp", np.exp(x))

print( "Linspace", np.linspace(-1, 0, 5))

N = 5 weights = np.exp(np.linspace(-1., 0., N))

weights /= weights.sum()

print( "Weights", weights)

c = np.loadtxt('data.csv', delimiter=',', usecols=(6,), unpack=True)

ema = np.convolve(weights, c)[N-1:-N+1]

t = np.arange(N - 1, len(c))

plot(t, c[N-1:], lw=1.0)

plot(t, ema, lw=2.0)

show()布林带

#布林带

N = 5

weights = np.ones(N) / N

print( "Weights", weights)

c = np.loadtxt('data.csv', delimiter=',', usecols=(6,), unpack=True)

sma = np.convolve(weights, c)[N-1:-N+1]

deviation = []C = len(c)

for i in range(N - 1, C): if i + N < C:

dev = c[i: i + N] else:

dev = c[-N:]

averages = np.zeros(N)

averages.fill(sma[i - N - 1])

dev = dev - averages

dev = dev ** 2

dev = np.sqrt(np.mean(dev))

deviation.append(dev)

deviation = 2 * np.array(deviation)

print( len(deviation), len(sma))upperBB = sma + deviationlowerBB = sma - deviation c_slice = c[N-1:]

between_bands = np.where((c_slice < upperBB) & (c_slice > lowerBB))

print( lowerBB[between_bands])

print( c[between_bands])

print( upperBB[between_bands])

between_bands = len(np.ravel(between_bands))

print( "Ratio between bands", float(between_bands)/len(c_slice))

t = np.arange(N - 1, C)

plot(t, c_slice, lw=1.0)

plot(t, sma, lw=2.0)

plot(t, upperBB, lw=3.0)

plot(t, lowerBB, lw=4.0)show()线性模型

#线性模型

N = int(sys.argv[1])

c = np.loadtxt('data.csv', delimiter=',', usecols=(6,), unpack=True)

b = c[-N:]b = b[::-1]

print( "b", b) A = np.zeros((N, N), float)

print( "Zeros N by N", A)

for i in range(N):

A[i, ] = c[-N - 1 - i: - 1 - i]

print( "A", A)(x, residuals, rank, s) = np.linalg.lstsq(A, b)

print( x, residuals, rank, s) print( np.dot(b, x))

#趋势线

def fit_line(t, y):

A = np.vstack([t, np.ones_like(t)]).T

return np.linalg.lstsq(A, y)[0]

h, l, c = np.loadtxt('data.csv', delimiter=',', usecols=(4, 5, 6), unpack=True)

pivots = (h + l + c) / 3print( "Pivots", pivots)

t = np.arange(len(c))

sa, sb = fit_line(t, pivots - (h - l))

ra, rb = fit_line(t, pivots + (h - l))

support = sa * t + sb

resistance = ra * t + rb

condition = (c > support) & (c < resistance)

print( "Condition", condition)

between_bands = np.where(condition)

print( support[between_bands])

print( c[between_bands])

print( resistance[between_bands])

between_bands = len(np.ravel(between_bands))

print( "Number points between bands", between_bands)

print( "Ratio between bands", float(between_bands)/len(c) )

print( "Tomorrows support", sa * (t[-1] + 1) + sb)

print( "Tomorrows resistance", ra * (t[-1] + 1) + rb)

a1 = c[c > support]a2 = c[c < resistance]

print( "Number of points between bands 2nd approach" ,len(np.intersect1d(a1, a2)))

plot(t, c)

plot(t, support)

plot(t, resistance)show()data.csv我上传了,可以下载练习