kaggle是一个很好的数据分析挖掘项目平台。可以从中感受到数据分析挖掘的实际应用价值,锻炼技能。它还是一个社交平台。

项目介绍:

在数据分析挖掘的过程中,最重要的一步就是提出重要的问题。

这一步做不好,接下来数据再好,分析在精妙,也没有意义(这也是统计的三要素:问题、数据、方法)。

银行在现代经济生活中扮演至关重要的地位,它希望借贷出去更多款项,但同时它又必须确保借贷人有偿还能力。这就涉及到金融风险预测评估的问题。根据历史,预测未来。根据历史数据,来预测未来会不会发生信用违约的情况,这是一个很重要的数据分析挖掘应用方向。以数据为依据,辅导决策!

数据介绍:

数据来源:give me some credit-kaggle

| Variable Name | Description | Type |

| SeriousDlqin2yrs | Person experienced 90 days past due delinquency or worse 是否有超过90天或更长时间逾期未还的不良行为 | Y/N |

| RevolvingUtilizationOfUnsecuredLines不安全额度循环利用 | Total balance on credit cards and personal lines of credit except real estate and no installment debt like car loans divided by the sum of credit limits.信用卡总余额和个人信用额度(除了房地产和分期付款给债务,比如汽车贷款)除以总信用限制。 | percentage |

| age | Age of borrower in years借贷者的年龄(以年计) | integer |

| NumberOfTime30-59DaysPastDueNotWorse | Number of times borrower has been 30-59 days past due but no worse in the last 2 years. | integer |

| DebtRatio | Monthly debt payments, alimony,living costs divided by monthy gross income月债务支出、赡养费、生活费除以总收入(毛收入) | percentage |

| MonthlyIncome | Monthly income | real |

| NumberOfOpenCreditLinesAndLoans | Number of Open loans (installment like car loan or mortgage) and Lines of credit (e.g. credit cards)公开贷款(如汽车和抵押的分期)和信用上线(比如信用卡)数量 | integer |

| NumberOfTimes90DaysLate | Number of times borrower has been 90 days or more past due(应付款、应付日期).90天或以上贷款者逾期未还的次数。 | integer |

| NumberRealEstateLoansOrLines | Number of mortgage and real estate loans including home equity lines of credit抵押和房地产数量(包括房屋净值信用额度) | integer |

| NumberOfTime60-89DaysPastDueNotWorse | Number of times borrower has been 60-89 days past due but no worse in the last 2 years. | integer |

| NumberOfDependents | Number of dependents in family excluding themselves (spouse, children etc.)家庭中的依赖者(比如说配偶子女,但不包括他自己) | integer |

数据初探:

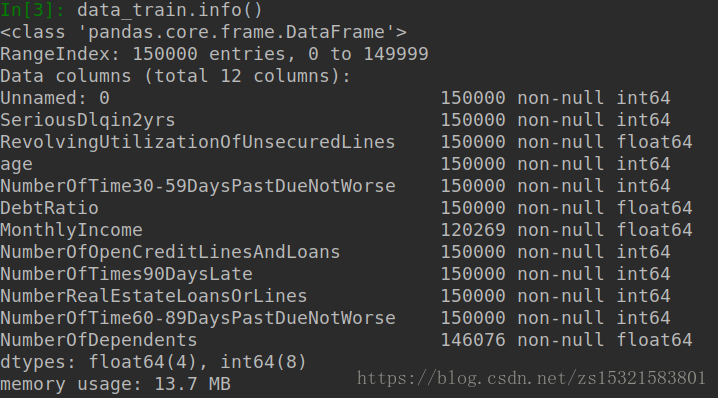

1.弄清楚数据条数(完整性)和类型

import pandas as pd

data_train = pd.read_csv('cs-training.csv')

了解到月收入和亲属人数2个特征中有缺省项。

2.了解各个特征的统计信息:

如果是KAGGLE中的数据,那么它还提供各个特征数据的频数分布直方图:

(以上截图出自pycharm,但是它的显示效果没有jupyter notebook好,后者会将结果以表格的形式显示出来!)

| Unnamed: 0 | SeriousDlqin2yrs | RevolvingUtilizationOfUnsecuredLines | age | NumberOfTime30-59DaysPastDueNotWorse | DebtRatio | MonthlyIncome | NumberOfOpenCreditLinesAndLoans | NumberOfTimes90DaysLate | NumberRealEstateLoansOrLines | NumberOfTime60-89DaysPastDueNotWorse | NumberOfDependents | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| count | 150000.000000 | 150000.000000 | 150000.000000 | 150000.000000 | 150000.000000 | 150000.000000 | 1.202690e+05 | 150000.000000 | 150000.000000 | 150000.000000 | 150000.000000 | 146076.000000 |

| mean | 75000.500000 | 0.066840 | 6.048438 | 52.295207 | 0.421033 | 353.005076 | 6.670221e+03 | 8.452760 | 0.265973 | 1.018240 | 0.240387 | 0.757222 |

| std | 43301.414527 | 0.249746 | 249.755371 | 14.771866 | 4.192781 | 2037.818523 | 1.438467e+04 | 5.145951 | 4.169304 | 1.129771 | 4.155179 | 1.115086 |

| min | 1.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000e+00 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 |

| 25% | 37500.750000 | 0.000000 | 0.029867 | 41.000000 | 0.000000 | 0.175074 | 3.400000e+03 | 5.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 |

| 50% | 75000.500000 | 0.000000 | 0.154181 | 52.000000 | 0.000000 | 0.366508 | 5.400000e+03 | 8.000000 | 0.000000 | 1.000000 | 0.000000 | 0.000000 |

| 75% | 112500.250000 | 0.000000 | 0.559046 | 63.000000 | 0.000000 | 0.868254 | 8.249000e+03 | 11.000000 | 0.000000 | 2.000000 | 0.000000 | 1.000000 |

| max | 150000.000000 | 1.000000 | 50708.000000 | 109.000000 | 98.000000 | 329664.000000 | 3.008750e+06 | 58.000000 | 98.000000 | 54.000000 | 98.000000 | 20.000000 |

从SeriousDlqin2yrs特征的统计信息中可以看出,这个数据集是一个极度不平衡的数据。

3.各项特征与结果的关联统计

探究连续型变量对某个分类结果的影响,方法之一是先将连续型变量用cut()离散成分段变量,然后统计各分段内的某一事件发声概率。

# 数据清洗

# 删除第一列,将.csv文件导入DataFrame中后会有自动索引

df = df.drop(df.columns[0], axis=1)

# 联系实际和统计信息,发现异常数据age<18的一项

# 查看age<18的项

# df[df.age < 18]

# 去掉age<18的项

df = df[df.age > 18]

# 通过了解数据背景,知道特征为连续型变量

# 特征若是分类变量,可以将每个特征不良和正常的数据分别做成频率分布表,

# 显示在一张图表中进行对比,可以对每个特征对结果的影响进行一个直观的了解。

# 使用cut函数,将连续变量转换成分类变量

def binning(col, cut_points, labels=None, isright=True):

val_min = col.min()

val_max = col.max()

break_points = [val_min] + cut_points + [val_max]

if not labels:

labels = range(len(cut_points) + 1)

else:

labels = [str(i + 1) + ':' + labels[i] for i in range(len(cut_points) + 1)]

colbin = pd.cut(col, bins=break_points, labels=labels, include_lowest=True, right=isright)

return colbin

# 将RevolvingUtilizationOfUnsecuredLines离散化

# 尽量不要在原始数据集中更改数据

df_tmp = df[['SeriousDlqin2yrs', 'RevolvingUtilizationOfUnsecuredLines']]

cut_points = [0.25, 0.5, 0.75, 1, 2]

labels = ['below0.25', '0.25-0.5', '0.5-0.75', '0.75-1.0', '1.0-2.0', 'above2']

df_tmp['Utilization_Bin'] = binning(df_tmp['RevolvingUtilizationOfUnsecuredLines'], cut_points, labels)

# 制作频率分布透视表

# 总人数

# total_size = df_tmp.shape[0]

# pd.pivot_table()是制作透视表工具。可以有多级索引,也可以有多级列标(如果默认column=None,那就是所有除了

# 索引外的列都是列标和计算值,列的聚合函数可以有多个。

# per_table = pd.pivot_table(df_tmp, index='Utilization_Bin', aggfunc = {'RevolvingUtilizationOfUnsecuredLines': [len, \

# lambda x:len(x)/total_size*100], 'SeriousDlqin2yrs': np.sum}, values=['RevolvingUtilizationOfUnsecuredLines','Serious\

# Dlqin2yrs'])

# per_table = pd.pivot_table(df_tmp, index=['Utilization_Bin'], aggfunc={"RevolvingUtilizationOfUnsecuredLines":[len, \

# lambda x:len(x)/total_size*100],"SeriousDlqin2yrs":[np.sum] },values=['RevolvingUtilizationOfUnsecuredLines','Seriou\

# sDlqin2yrs'])

# 给透视表增加违约率列

# 多级索引数据框的索引格式pd[a_level,b_level,..]

# per_table['SeriousDlqin2yrs', 'percent'] = per_table['SeriousDlqin2yrs', 'sum'] / per_table['RevolvingUtilizationO\

# fUnsecuredLines', 'len']*100

# 给透视表重命名

# per_table = per_table.rename(columns={'<lambda>': 'percent', 'len': 'number', 'sum': 'number'})

# 把number 放在前面,percent放在后面更合理,用reindex调整顺序

# per_table = per_table.reindex((per_table.columns[1], per_table.columns[0], per_table.columns[2], per_table.col\

# umns[3]), axis=1)

# 将上述生成频率分布表的过程写成函数,以便对每个变量进行类似处理

def get_frequency(df, col_x, col_y, cut_points, labels, isright=True):

df_tmp = df[[col_x, col_y]]

df_tmp['columns_Bin'] = binning(df_tmp[col_x], cut_points, labels, isright=isright)

total_size = df_tmp.shape[0]

per_table = pd.pivot_table(df_tmp, index='columns_Bin', aggfunc={col_x:[len, lambda x:len(x)/total_size], col_y:

np.sum}, values=[col_x, col_y])

if per_table.columns[0][0] != col_x:

# 假如col_x不在第一列,说明是在第2/3列,就把他们往前挪

per_table = per_table.reindex((per_table.columns[1], per_table.columns[2], per_table.columns[0]), axis=1)

per_table[col_y, 'percent'] = per_table[col_y, 'sum'] / per_table[col_x, 'len']*100

per_table = per_table.rename(columns={'<lambda>': 'percent', 'len': 'number', 'sum': 'number'})

per_table = per_table.reindex((per_table.columns[1], per_table.columns[0], per_table.columns[2], per_table.

columns[3]), axis=1)

return per_table

上图中的行索引是将RevolvingUtilizationOfUnsecuredLines列的连续百分比值变成分段的离散变量;第一个number是分段人数统计,第一个percent是分段人数占总人数的比例;第二个number是分段内的违约人数,第二个percent是分段违约人数占总人数的比例。

从上表中可以看出变量RevolvingUtilizationOfUnsecuredLines对违约率的影响,呈不对称的钟形分布。

对其他各个特征变量与违约率的关系:

# age

cut_points = [25, 35, 45, 55, 65]

labels = ['below25', '26-35', '36-45', '46-55', '56-65', 'above65']

freq_age = get_frequency(df, 'age', 'SeriousDlqin2yrs', cut_points, labels)

# print(freq_age)

#DeptRatio

cut_points = [0.25,0.5,0.75,1,2]

labels = ["below0.25","0.25-0.5","0.5-0.75","0.75-1.0","1.0-2.0","above2"]

feq_ratio=get_frequency(df,'DebtRatio','SeriousDlqin2yrs', cut_points, labels)

#print(feq_ratio)

#NumberOfOpenCreditLinesAndLoans

cut_points=[5,10,15,20,25,30]

labels=['below 5', '6-10', '11-15','16-20','21-25','26-30','above 30']

feq_OpenCredit=get_frequency(df,'NumberOfOpenCreditLinesAndLoans','SeriousDlqin2yrs', cut_points, labels)

#print(feq_OpenCredit)

#NumberRealEstateLoansOrLines

cut_points=[5,10,15,20]

labels=['below 5', '6-10', '11-15','16-20','above 20']

feq_RealEstate=get_frequency(df,'NumberRealEstateLoansOrLines','SeriousDlqin2yrs', cut_points, labels)

#print(feq_RealEstate)

#NumberOfTime30-59DaysPastDueNotWorse

cut_points=[1,2,3,4,5,6,7]

labels=['0','1','2','3','4','5','6','7 and above',]

feq_30days=get_frequency(df,'NumberOfTime30-59DaysPastDueNotWorse','SeriousDlqin2yrs', cut_points, labels,isright=False)

#print(feq_30days)

#MonthlyIncome

cut_points=[5000,10000,15000]

labels=['below 5000', '5000-10000','1000-15000','above 15000']

feq_Income=get_frequency(df,'MonthlyIncome','SeriousDlqin2yrs', cut_points, labels)

#print(feq_Income)

#NumberOfDependents

cut_points = [1,2,3,4,5]

labels = ["0","1","2","3","4","5 and more"]

feq_dependent=get_frequency(df,'NumberOfDependents','SeriousDlqin2yrs', cut_points, labels,isright=False)

print(feq_dependent)

age SeriousDlqin2yrs

number percent number percent

columns_Bin

1:below25 3027.0 0.020180 338 11.166171

2:26-35 18458.0 0.123054 2053 11.122548

3:36-45 29819.0 0.198795 2628 8.813173

4:46-55 36690.0 0.244602 2786 7.593350

5:56-65 33406.0 0.222708 1531 4.583009

6:above65 28599.0 0.190661 690 2.412672

------------------------------

DebtRatio SeriousDlqin2yrs

number percent number percent

columns_Bin

1:below0.25 52361.0 0.349076 3126 5.970092

2:0.25-0.5 41346.0 0.275642 2529 6.116674

3:0.5-0.75 15728.0 0.104854 1484 9.435402

4:0.75-1.0 5427.0 0.036180 596 10.982126

5:1.0-2.0 4092.0 0.027280 539 13.172043

6:above2 31045.0 0.206968 1752 5.643421

------------------------------

NumberOfOpenCreditLinesAndLoans SeriousDlqin2yrs \

number percent number

columns_Bin

1:below 5 46590.0 0.310602 3922

2:6-10 60399.0 0.402663 3345

3:11-15 29184.0 0.194561 1804

4:16-20 9846.0 0.065640 676

5:21-25 2841.0 0.018940 191

6:26-30 785.0 0.005233 62

7:above 30 354.0 0.002360 26

percent

columns_Bin

1:below 5 8.418115

2:6-10 5.538171

3:11-15 6.181469

4:16-20 6.865732

5:21-25 6.722985

6:26-30 7.898089

7:above 30 7.344633

------------------------------

NumberRealEstateLoansOrLines SeriousDlqin2yrs

number percent number percent

columns_Bin

1:below 5 149206.0 0.994713 9884 6.624398

2:6-10 699.0 0.004660 121 17.310443

3:11-15 70.0 0.000467 16 22.857143

4:16-20 14.0 0.000093 3 21.428571

5:above 20 10.0 0.000067 2 20.000000

------------------------------

NumberOfTime30-59DaysPastDueNotWorse SeriousDlqin2yrs \

number percent number

columns_Bin

1:0 126018.0 0.840126 5041

2:1 16032.0 0.106881 2409

3:2 4598.0 0.030654 1219

4:3 1754.0 0.011693 618

5:4 747.0 0.004980 318

6:5 342.0 0.002280 154

7:6 140.0 0.000933 74

8:7 and above 104.0 0.000693 50

percent

columns_Bin

1:0 4.000222

2:1 15.026198

3:2 26.511527

4:3 35.233751

5:4 42.570281

6:5 45.029240

7:6 52.857143

8:7 and above 48.076923

------------------------------

MonthlyIncome SeriousDlqin2yrs

number percent number percent

columns_Bin

1:below 5000 55859.0 0.372396 4813 8.616338

2:5000-10000 46090.0 0.307269 2752 5.970926

3:1000-15000 13035.0 0.086901 547 4.196394

4:above 15000 5284.0 0.035227 245 4.636639

------------------------------

NumberOfDependents SeriousDlqin2yrs

number percent number percent

columns_Bin

1:0 86902.0 0.579351 5095 5.862926

2:1 26316.0 0.175441 1935 7.352941

3:2 19521.0 0.130141 1584 8.114338

4:3 9483.0 0.063220 837 8.826321

5:4 2862.0 0.019080 297 10.377358

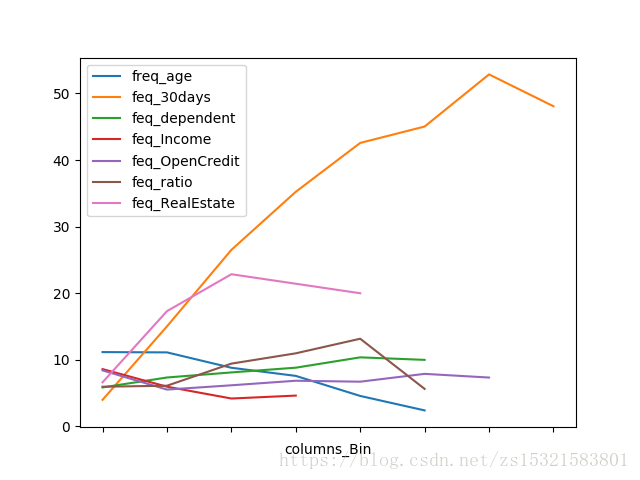

6:5 and more 990.0 0.006600 99 10.000000将上列表格变成更直观的图形:

由上表统计信息可知:

1.随着年龄增加,贷款违约率降低

2.随着借贷率的升高,违约率先升后降。

3.随着30天违约次数的升高,违约率先先急剧升高后降。

4.随着亲人数的增加,违约率缓慢增加。

5.随着收入增加,违约率先缓慢降低然后基本不变。

。。。

模型构建:

比较逻辑回归模型、决策树模型和随机森林模型的AUC值,择优选用。

# coding = utf-8

import pandas as pd

import numpy as np

from sklearn.ensemble import RandomForestClassifier

from sklearn.metrics import roc_auc_score

from sklearn.model_selection import GridSearchCV

from sklearn.model_selection import StratifiedShuffleSplit

from sklearn.preprocessing import Imputer

from sklearn.linear_model.logistic import LogisticRegression

from sklearn import tree

# 忽略警告错误的输出

import warnings

warnings.filterwarnings('ignore')

# 用数据集构造随机森林分类器模型

# 加载数据(训练和测试)

# preprocessing

# split training_data into training_new&test_new to verify model

# use mean_value to replace default_value with the method Imputer

# build a RandomForestModel with training_new

# deal with the unbalanced data problem

# perform parameters'ajustment with GridSearchCV in CrossValidation

# export best model and test it with data_test

# 创建字典函数

# input: keys = [] and values = []

# output: dict{}

def create_dict(keys, vals):

lookup = {}

if len(keys) == len(vals):

for i in range(len(keys)):

key = keys[i]

val = vals[i]

lookup[key] = val

return lookup

# 计算AUC函数

# input: y_true = [] and y_score = []

# output: auc

def compute_auc(y_true, y_score):

auc = roc_auc_score(y_true, y_score)

print('auc', auc)

return auc

def main():

# 1,加载数据(训练和测试)和预处理数据

colnames = ['ID', 'label', 'RUUnsecuredL', 'age', 'NOTime30-59',

'DebtRatio', 'Income', 'NOCredit', 'NOTimes90',

'NORealEstate', 'NOTime60-89', 'NODependents']

# 将数据集中没有意义的数值全部指定为‘NA',比如年龄小于18,

col_nas = ['', 'NA', 'NA', 0, [98, 96], 'NA', 'NA', 'NA', [98, 96], 'NA', [98, 96], 'NA'] col_na_values = create_dict(colnames, col_nas)

dftrain = pd.read_csv('cs-training.csv', names=colnames,

na_values=col_na_values, skiprows=[0])

# print(dftrain)

# pop()返回删除的列,并默认本地删除

train_id = [int(x) for x in dftrain.pop('ID')]

y_train = np.asarray([int(x) for x in dftrain.pop('label')])

x_train = dftrain.values

dftest = pd.read_csv('cs-test.csv', names=colnames,

na_values=col_na_values, skiprows=[0])

test_id = [int(x) for x in dftest.pop('ID')]

y_test = np.asarray(dftest.pop('label'))

x_test = dftest.values

# 2,使用StratifiedShuffleSplit将训练数据分解为trainning_new和test_new(用于验证模型)

sss = StratifiedShuffleSplit(n_splits=1, test_size=0.33333, random_state=0)

for train_index, test_index in sss.split(x_train, y_train):

# print("TRAIN:", train_index, "TEST:", test_index)

x_train_new, x_test_new = x_train[train_index], x_train[test_index]

y_train_new, y_test_new = y_train[train_index], y_train[test_index]

y_train = y_train_new

x_train = x_train_new

# 3,使用Imputer将所有NaN替换为平均值

imp = Imputer(missing_values='NaN', strategy='mean', axis=0)

imp.fit(x_train)

x_train = imp.transform(x_train)

x_test_new = imp.transform(x_test_new)

x_test = imp.transform(x_test)

# 使用training_new数据建立RF模型

rf = RandomForestClassifier()

# 模型比较

# 逻辑回归,二分类模型

lr = LogisticRegression()

# 拟合逻辑回归模型

lr.fit(x_train, y_train)

# 预测训练集中各样本落入各个类别的概率

predicted_probs_train = lr.predict_proba(x_train)

predicted_probs_train = [x[1] for x in predicted_probs_train]

# 计算AUC值

compute_auc(y_train, predicted_probs_train)

# 预测测试集中各样本落入各个类别的概率

predicted_probs_test_new = lr.predict_proba(x_test_new)

predicted_probs_test_new = [x[1] for x in predicted_probs_test_new]

compute_auc(y_test_new, predicted_probs_test_new)

# 树模型中的决策树模型

model = tree.DecisionTreeClassifier()

model.fit(x_train, y_train)

predicted_probs_train = model.predict_proba(x_train)

predicted_probs_train = [x[1] for x in predicted_probs_train]

compute_auc(y_train, predicted_probs_train)

predicted_probs_test_new = model.predict_proba(x_test_new)

predicted_probs_test_new = [x[1] for x in predicted_probs_test_new]

compute_auc(y_test_new, predicted_probs_test_new)

# 随机森林

rf.fit(x_train, y_train)

# 模型AUC值比较

predicted_probs_train = rf.predict_proba(x_train)

predicted_probs_train = [x[1] for x in predicted_probs_train]

compute_auc(y_train, predicted_probs_train)

predicted_probs_test_new = rf.predict_proba(x_test_new)

predicted_probs_test_new = [x[1] for x in predicted_probs_test_new]

compute_auc(y_test_new, predicted_probs_test_new)

# 输出特征重要性评估

print(sorted(zip(map(lambda x: round(x, 4), rf.feature_importances_), dftrain.columns), reverse=True))

# 使用具有crossvalidation的网格搜索执行参数调整

param_grid = {"max_features": [2, 3, 4], "min_samples_leaf": [50]}

grid_search = GridSearchCV(rf, cv=10, scoring='roc_auc', param_grid=param_grid, iid=False)

# 输出最佳模型

# 使用最优参数和训练数据构建模型

grid_search.fit(x_train, y_train)

print('the best parameter:', grid_search.best_params_)

print('the best score:', grid_search.best_score_)

# 使用rf预测train

predicted_probs_train = grid_search.predict_proba(x_train)

predicted_probs_train = [x[1] for x in predicted_probs_train]

compute_auc(y_train, predicted_probs_train)

# 使用rf预测test

predicted_probs_test_new = grid_search.predict_proba(x_test_new)

predicted_probs_test_new = [x[1] for x in predicted_probs_test_new]

compute_auc(y_test_new, predicted_probs_test_new)

# 使用rf预测test data

predicted_probs_test = grid_search.predict_proba(x_test)

predicted_probs_test = ['%.9f' % x[1] for x in predicted_probs_test]

submission = pd.DataFrame({'ID': test_id, 'Probability': predicted_probs_test})

submission.to_csv('rf_submission.csv', index=False)

# 如果直接运行.py文件,则__name__ == '__main__'

# 如果是引入.py文件,则__name__ == 文件名

if __name__ == '__main__':

main()

参考:

基于随机森林算法的贷款违约预测模型研究(Give me some credit)