1 初始环境准备

读取数据与预览

rm(list=ls())

#setwd("./case")

#install.packages("xlsx")

library(openxlsx)

dat<-read.xlsx("credit.xlsx",1)

View(dat)

2数据预览与处理

数据预览,发现最大值999的异常值,偏离平均值

class(dat)

#describe data

summary(dat)

sum(is.na(dat))

异常值处理,使用na填充

#Outlier filling

dat[,1:6]<-sapply(dat[,1:6],function(x) {x[x==999]<-NA;return(x)} )

nrow(dat)

ncol(dat)

summary(dat[,11])

#Understand data deletion invalid variables

dat<-dat[,-11]

将字符型变量character转化为因子变量factor

#Change string variable type to classification variable

dat1<-dat

sapply(dat1,class)

ch=names(which(sapply(dat1,is.character)))#find the character type variance

dat1[,ch]=as.data.frame(lapply(dat1[,ch], as.factor))

观察数据发现家庭人口数和家庭孩子数密切相关,存在多重共线性,于是产生标识变量代替这二个变量

dat1[,4]<-dat1[,4]-dat1[,3]

table(dat1[,4])

dat1[,4]<-factor(dat1[,4],levels=c(1,2),labels=c("其他","已婚"))

colnames(dat1)<-c("age","income","child","marital","dur_live",

"dur_work","housetype","nation","cardtype","loan")

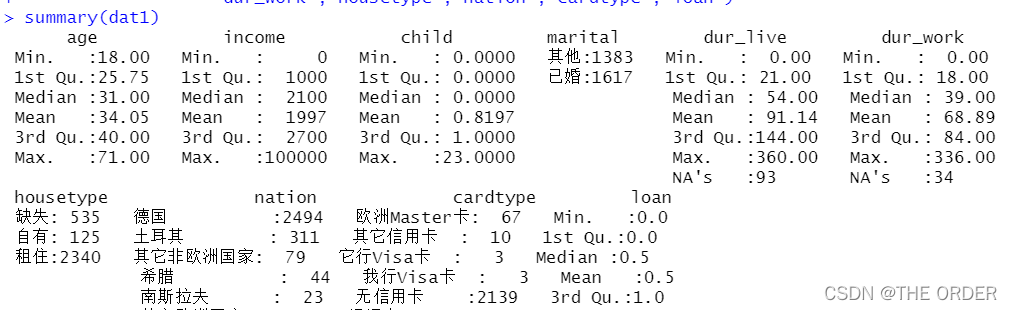

summary(dat1)

3 描述性统计

相关包准备

#install.packages("smbinning")

#install.packages("prettyR")

library(smbinning)

library(prettyR)

library(mvtnorm)

library(kernlab)

盖帽法

异常值可以使用盖帽法处理,使用1%和99%分位数替换异常值

##盖帽法函数 去除异常用99%和1%点分别代替异常值

block<-function(x,lower=T,upper=T){

if(lower){

q1<-quantile(x,0.01)

x[x<=q1]<-q1

}

if(upper){

q99<-quantile(x,0.99)

x[x>q99]<-q99

}

return(x)

}

数据集中1是不违约,0是违约,进行反转设定,使1变为违约,0为不违约

#Odds ratio conversion for later IV calculation

dat1$loan<-as.numeric(!as.logical(dat1$loan))

描述数据分类统计

违约和不违约的人群的区别

#data classification ,discretization of continuous variables

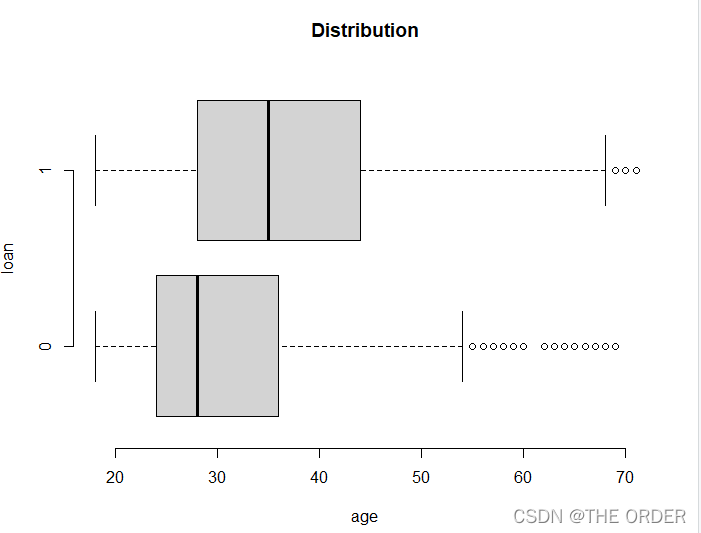

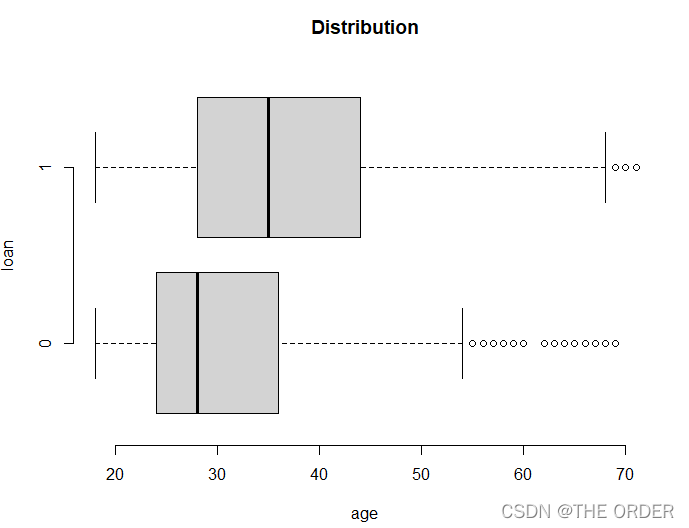

##age

boxplot(age~loan,data=dat1,horizontal=T, frame=F,

col="lightgray",main="Distribution")

age<-smbinning(dat1,"loan","age")

age$ivtable

违约与否的年龄箱线图

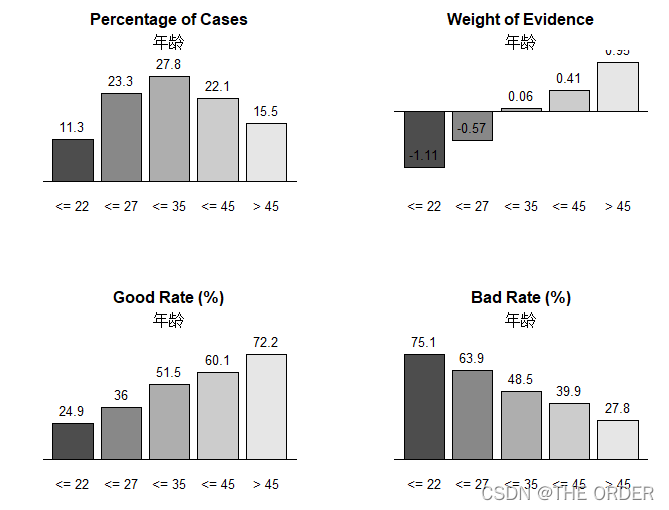

分箱后的IV图

age<-smbinning(dat1,"loan","age")

age$ivtable

对年龄进行分箱后,查看百分比,weight,good,bad rate,后面的描述性统计大致如此,可以秦楚看出不同年龄层次的区别

par(mfrow=c(2,2))

smbinning.plot(age,option="dist",sub="年龄")

smbinning.plot(age,option="WoE",sub="年龄")

smbinning.plot(age,option="goodrate",sub="年龄")

smbinning.plot(age,option="badrate",sub="年龄"

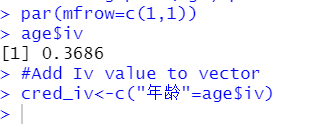

将IV结果添加到一个向量中

par(mfrow=c(1,1))

age$iv

#Add Iv value to vector

cred_iv<-c("年龄"=age$iv)

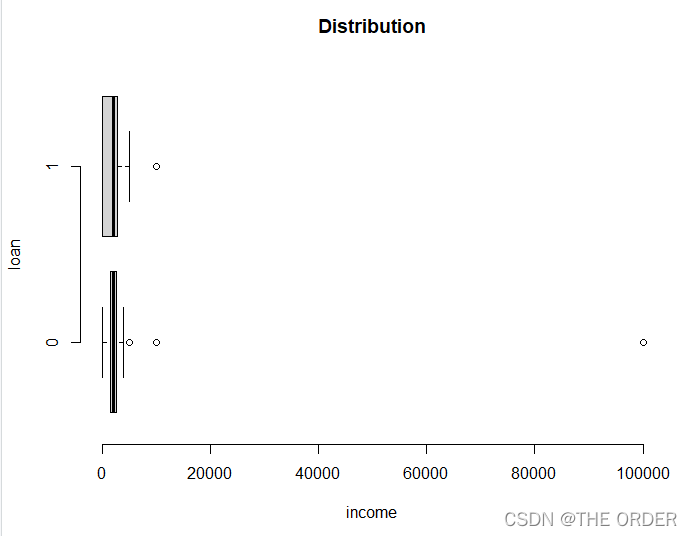

关于收入,明显存在异常值,使用盖帽法

##income

boxplot(income~loan,data=dat1,horizontal=T, frame=F,

col="lightgray",main="Distribution")

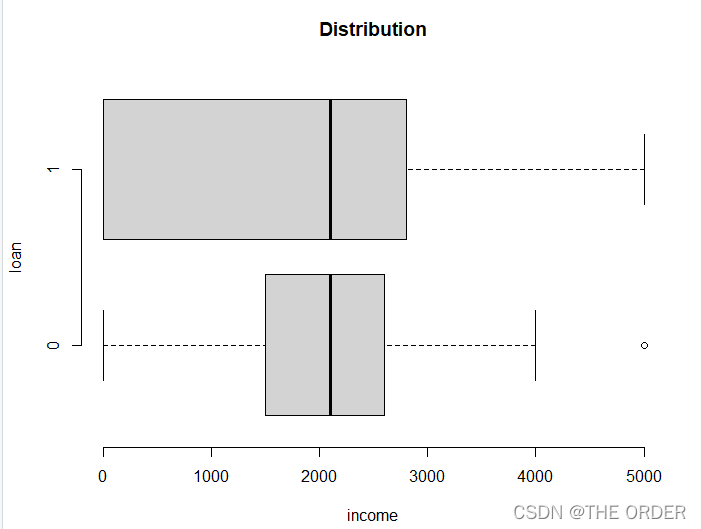

盖帽法填充

dat1$income<-block(dat1$income)

填充后明显变正常了

boxplot(income~loan,data=dat1,horizontal=T, frame=F,

col="lightgray",main="Distribution")

```

IV值测量,同上age

income<-smbinning(dat1,"loan","income")

income$ivtable

smbinning.plot(income,option="WoE",sub="收入")

income$iv

cred_iv<-c(cred_iv,"收入"=income$iv)

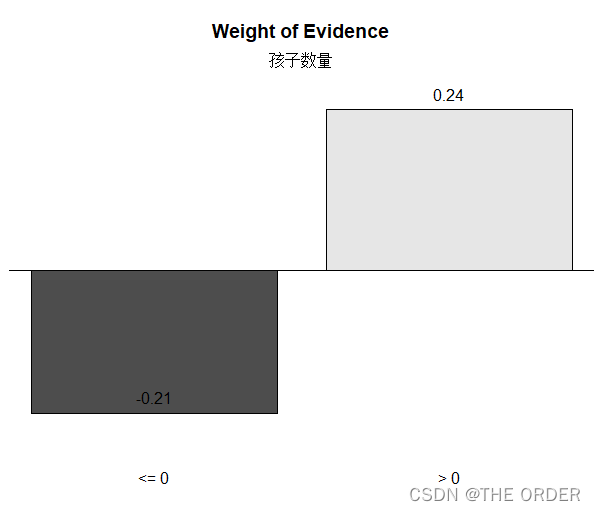

child 统计

##child

boxplot(child~loan,data=dat1,horizontal=T, frame=F,

col="lightgray",main="Distribution")

child<-smbinning(dat1,"loan","child")

child$ivtable

smbinning.plot(child,option="WoE",sub="孩子数量")

child$iv

cred_iv<-c(cred_iv,"孩子数量"=child$iv)

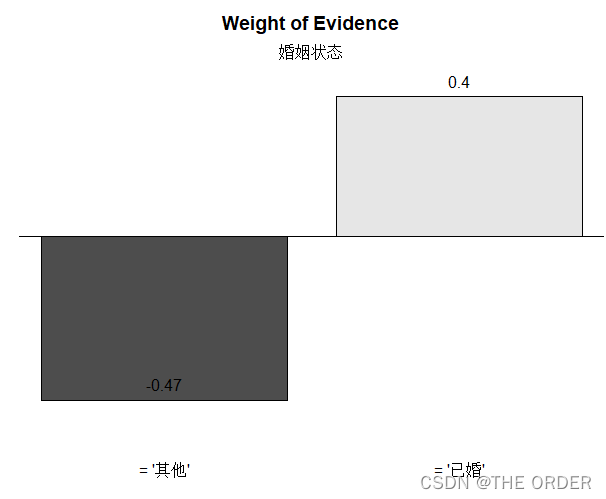

##marital

xtab(~marital+loan,data=dat1,chisq=T)

marital<-smbinning.factor(dat1,"loan","marital")

marital$ivtable

smbinning.plot(marital,option="WoE",sub="婚姻状态")

marital$iv

cred_iv<-c(cred_iv,"婚姻状态"=marital$iv)

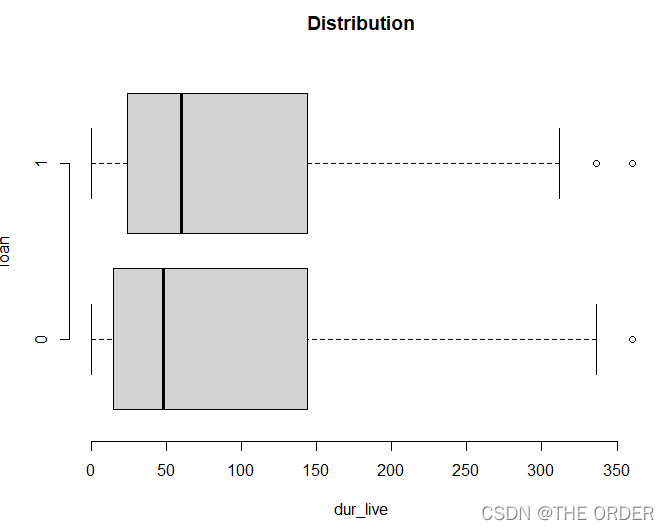

##dur_live

boxplot(dur_live~loan,data=dat1,horizontal=T,

frame=F, col="lightgray",main="Distribution")

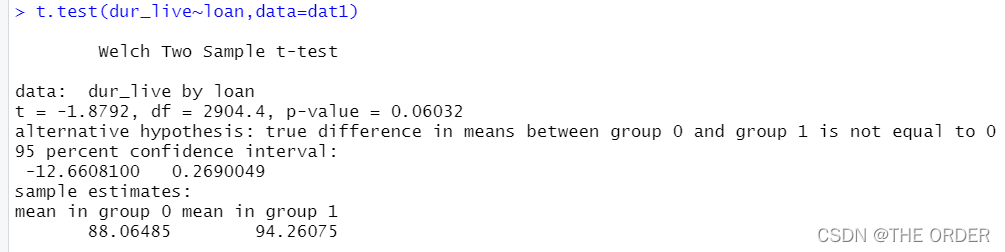

t.test(dur_live~loan,data=dat1)

dur_live<-smbinning(dat1,"loan","dur_live")

dur_live

观察得到dur_live变量对违约分布区别不大,使用t检验,不能拒绝二者同分布

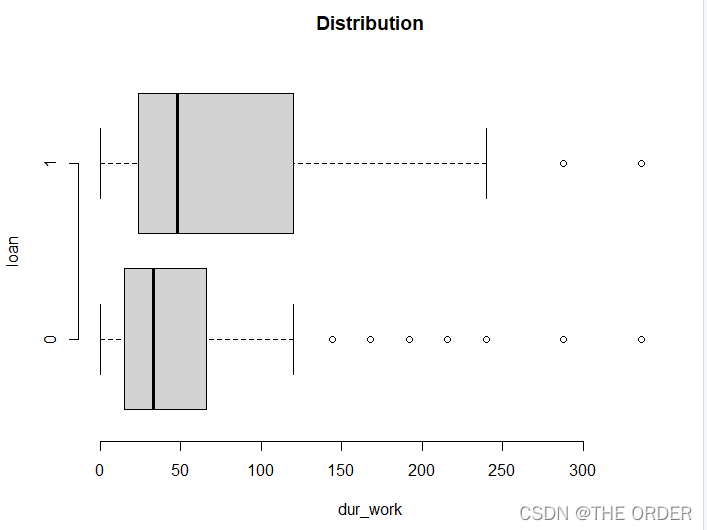

dur_work变量统计

##dur_work

boxplot(dur_work~loan,data=dat1,horizontal=T,

frame=F, col="lightgray",main="Distribution")

t.test(dur_work~loan,data=dat1)

dur_work<-smbinning(dat1,"loan","dur_work")

dur_work$ivtable

smbinning.plot(dur_work,option="WoE",sub="在现工作时间")

dur_work$iv

cred_iv<-c(cred_iv,"在现工作时间"=dur_work$iv)

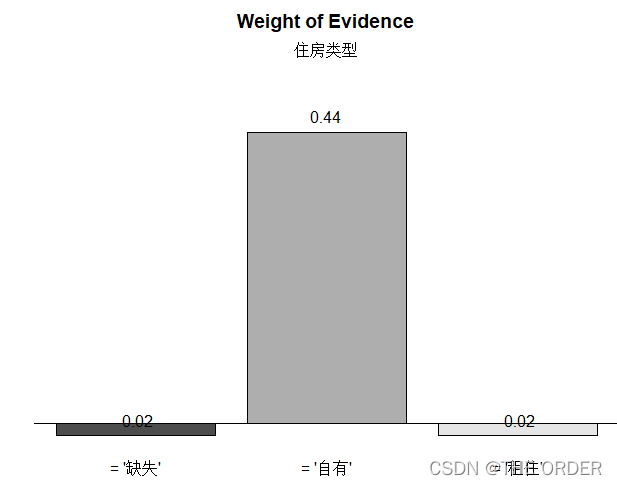

housetype描述统计

##housetype

xtab(~housetype+loan,data=dat1,chisq=T)

housetype<-smbinning.factor(dat1,"loan","housetype")

housetype$ivtable

smbinning.plot(housetype,option="WoE",sub="住房类型")

housetype$iv

cred_iv<-c(cred_iv,"住房种类"=housetype$iv)

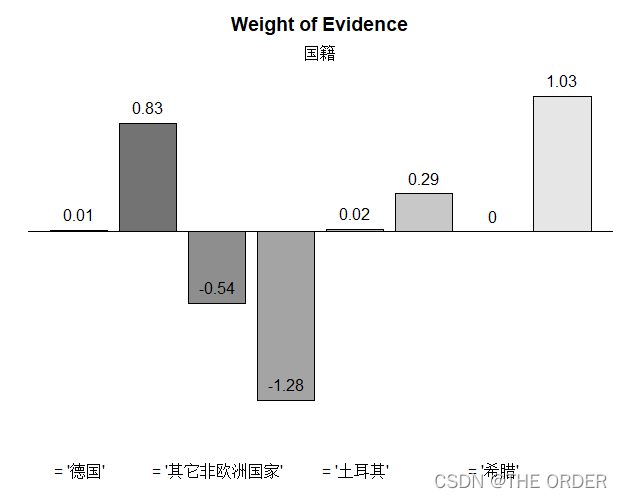

##nation

xtab(~nation+loan,data=dat1,chisq=T)

nation<-smbinning.factor(dat1,"loan","nation")

nation$ivtable

smbinning.plot(nation,option="WoE",sub="国籍")

nation$iv

cred_iv<-c(cred_iv,"国籍"=nation$iv)

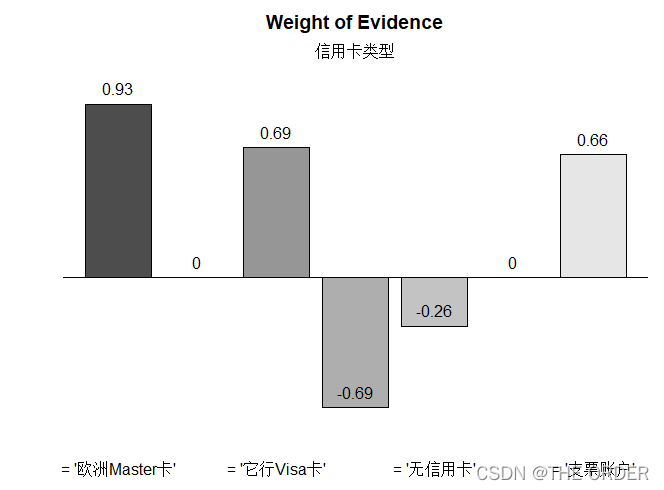

cardtype描述统计

##cardtype

xtab(~cardtype+loan,data=dat1,chisq=T)

cardtype<-smbinning.factor(dat1,"loan","cardtype")

cardtype$ivtable

smbinning.plot(cardtype,option="WoE",sub="信用卡类型")

cardtype$iv

cred_iv<-c(cred_iv,"信用卡类型"=cardtype$iv)

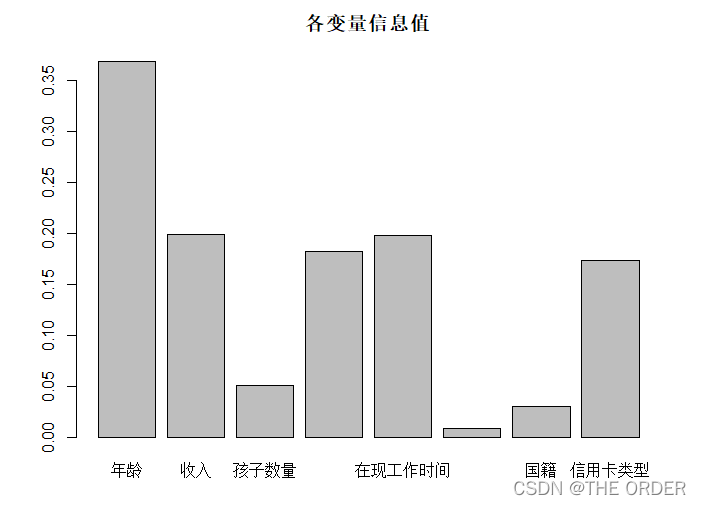

总体变量IV值程度

#Drawing shows the amount of information

barplot(cred_iv,main="各变量信息值")

4 属性分箱

#quantity after adding classification

dat2<-dat1

dat2<-smbinning.gen(dat2,age,"glage")

dat2<-smbinning.gen(dat2,income,"glincome")

dat2<-smbinning.gen(dat2,child,"glchild")

dat2<-smbinning.factor.gen(dat2,marital,"glmarital")

dat2<-smbinning.gen(dat2,dur_work,"gldur_work")

dat2<-smbinning.factor.gen(dat2,housetype,"glhousetype")

dat2<-smbinning.factor.gen(dat2,nation,"glnation")

dat2<-smbinning.factor.gen(dat2,cardtype,"glcardtype")

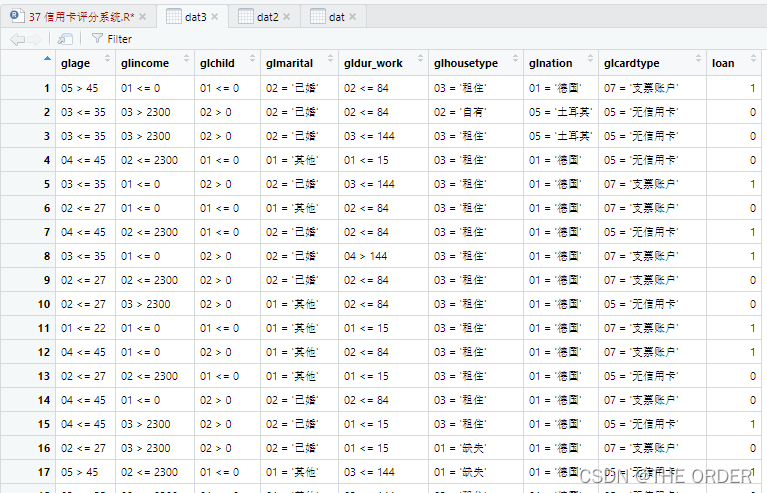

View(dat2)

dat3<-dat2[,c(11:18,10)]

View(dat3)

生成分箱后的数据级,将用户属性转化为区间数据

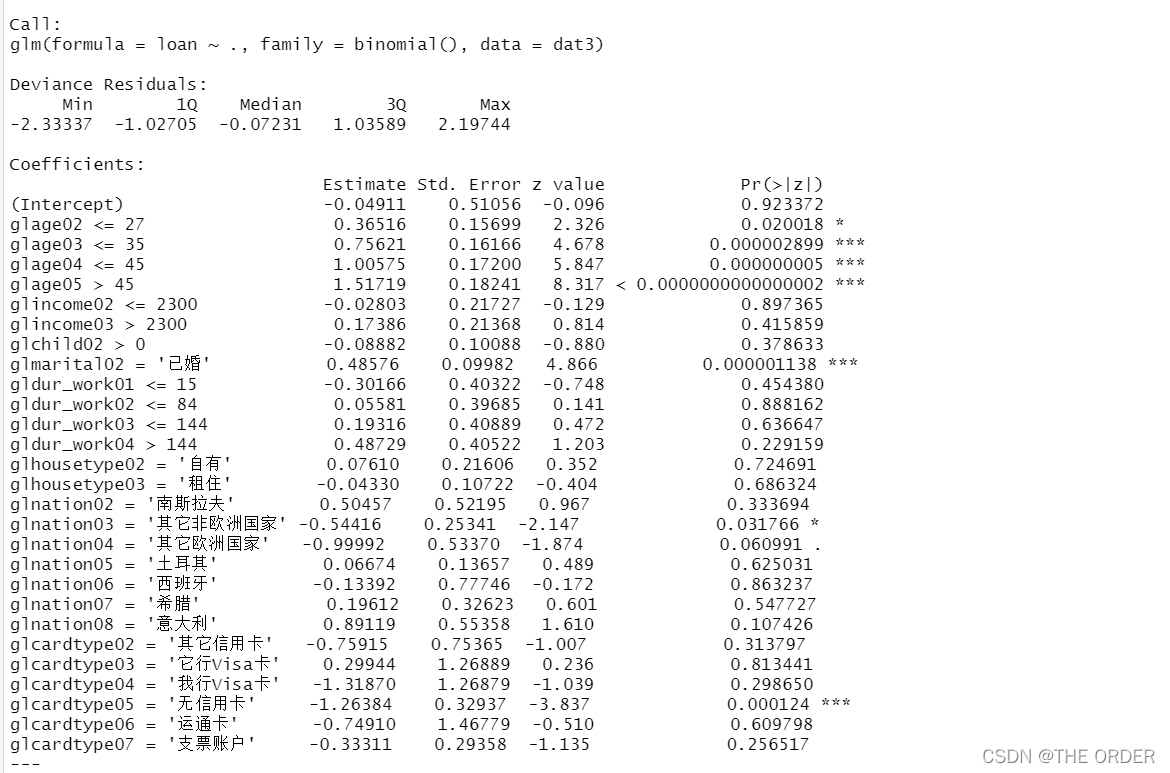

5 logistic建模

具体打分理论参考链接: link.

模型生成

#Creat logistic regression

cred_mod<-glm(loan~. ,data=dat3,family=binomial())

summary(cred_mod)

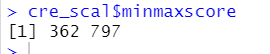

6 打分系统

依照打分公式发现,信用最高评分和最低评分分别为797,362分

#Scoring card system

cre_scal<-smbinning.scaling(cred_mod,pdo=45,score=800,odds=50)

cre_scal$logitscaled

cre_scal$minmaxscore

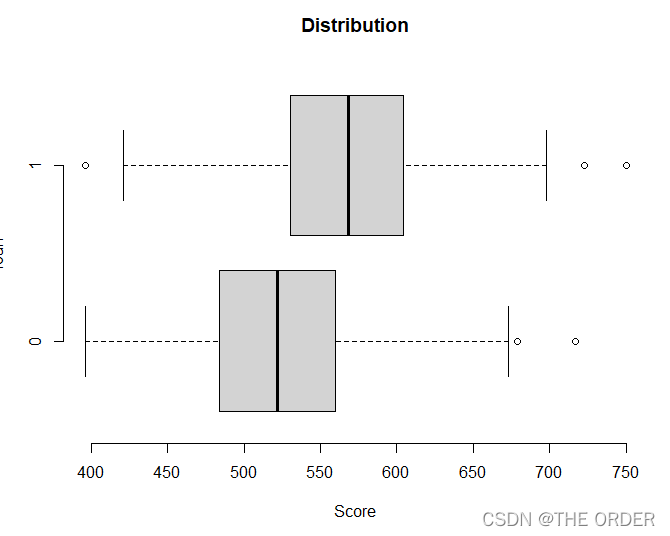

违约过与否的箱线图展示

#Score each item

dat4<-smbinning.scoring.gen(smbscaled=cre_scal, dataset=dat3)

boxplot(Score~loan,data=dat4,horizontal=T, frame=F,

col="lightgray",main="Distribution")

生成打分指标

#Standardized scoring table

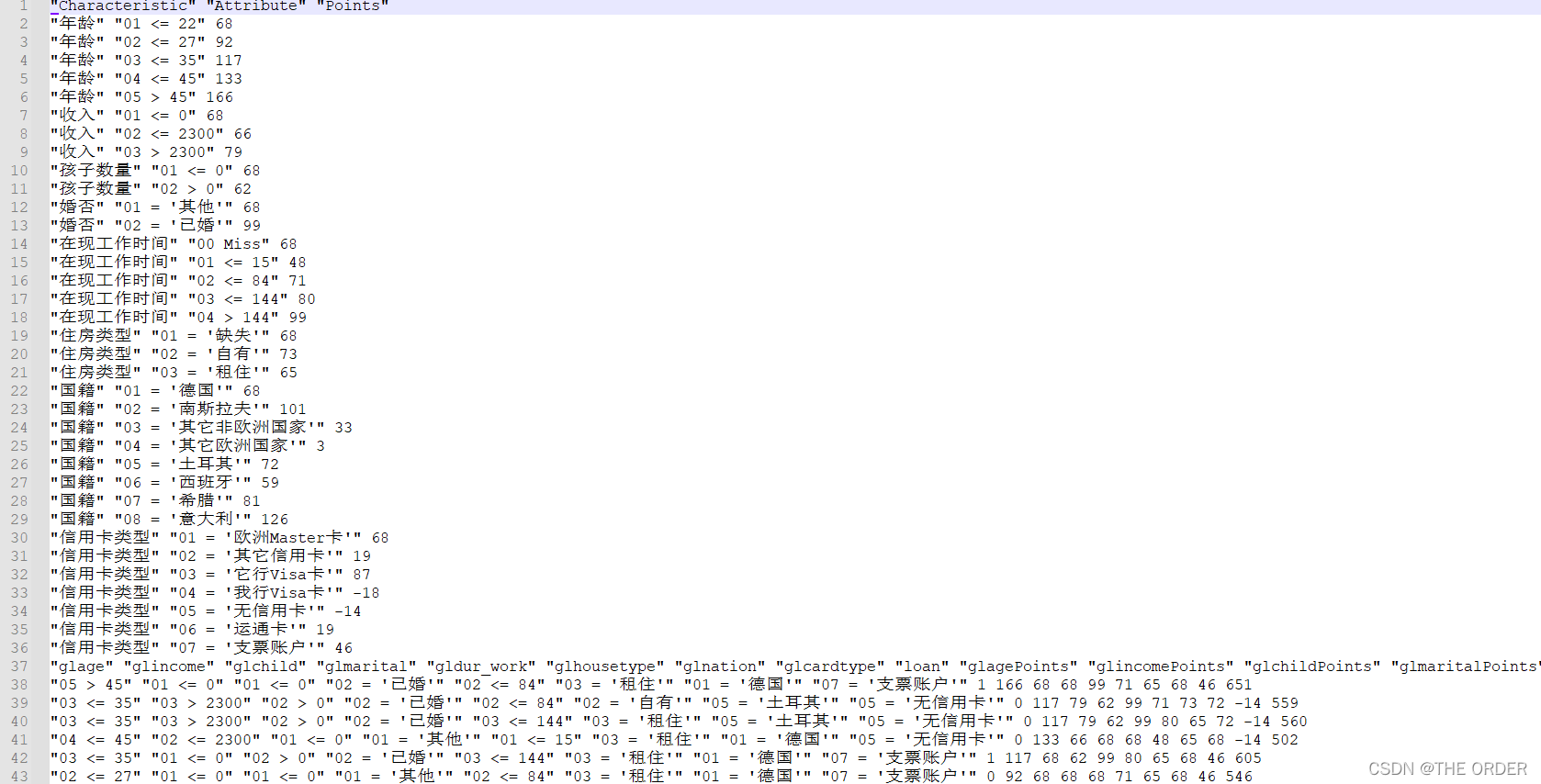

scaledcard<-cre_scal$logitscaled[[1]][-1,c(1,2,6)]

scaledcard[,1]<-c(rep("年龄",5),rep("收入",3),rep("孩子数量",2),

rep("婚否",2),rep("在现工作时间",5),

rep("住房类型",3),rep("国籍",8),rep("信用卡类型",7))

scaledcard

7 写入csv文件

ncol(dat4)

dat5=dat4[,10:18]

#write the results

write.table(scaledcard,"card.csv",row.names = F)

write.table(dat4,"card.csv",row.names = F,append = T)

?write.csv

输出文件给业务人员