numpy常用函数学习2

点乘法

该方法为数学方法,但是在numpy使用的时候略坑。numpy的点乘为a.dot(b)或numpy.dot(a,b),要求a,b的原始数据结构为MxN .* NxL=MxL,不是显示数据,必须经过a.resize()或者a.shape=两种方法转换才能将原始数据改变结构。

代码如下:

>>> import numpy as np

>>> a=np.array([[1,2,3,4],[5,6,7,8]])

>>> a

array([[1, 2, 3, 4],

[5, 6, 7, 8]])

>>> b=np.array([[9],[9]])

>>> b

array([[9],

[9]])

>>> a*b

array([[ 9, 18, 27, 36],

[45, 54, 63, 72]])

>>> a.dot(b)

Traceback (most recent call last):

File "<pyshell#6>", line 1, in <module>

a.dot(b)

ValueError: shapes (2,4) and (2,1) not aligned: 4 (dim 1) != 2 (dim 0)

>>> c=np.array([[9],[10]])

>>> a*c

array([[ 9, 18, 27, 36],

[50, 60, 70, 80]])

>>> d=np.array([[10,20,30,40],[50,60,70,80]])

>>> a.dot(d)

Traceback (most recent call last):

File "<pyshell#10>", line 1, in <module>

a.dot(d)

ValueError: shapes (2,4) and (2,4) not aligned: 4 (dim 1) != 2 (dim 0)

>>> d.reshape(4,2)

array([[10, 20],

[30, 40],

[50, 60],

[70, 80]])

>>> a.dot(d)

Traceback (most recent call last):

File "<pyshell#23>", line 1, in <module>

a.dot(d)

ValueError: shapes (2,4) and (2,4) not aligned: 4 (dim 1) != 2 (dim 0)

>>> d

array([[10, 20, 30, 40],

[50, 60, 70, 80]])

>>> d.resize(4,2)

>>> a.dot(d)

array([[ 500, 600],

[1140, 1400]])

>>> a

array([[1, 2, 3, 4],

[5, 6, 7, 8]])

>>> e=np.array([7,8,9,10])

>>> e.shape=(4,1)

>>> a.dot(e)

array([[ 90],

[226]])

线型预测

通过最小二乘法对已有数据拟合出函数,并预测未知数据。

最小二乘法:在假定函数结构(这里假设我们知道结果是y=ax+b)的情况下,通过已知结果(x,y)求取未知变量(a,b)。

具体求取原理参考:https://baijiahao.baidu.com/s?id=1613474944612061421&wfr=spider&for=pc

预测例子:

import datetime as dt

import numpy as np

import pandas as pd

import matplotlib.pyplot as mp

import matplotlib.dates as md

def dmy2ymd(dmy):

dmy = str(dmy, encoding='utf-8')

date = dt.datetime.strptime(dmy, '%d-%m-%Y').date()

ymd = date.strftime('%Y-%m-%d')

return ymd

dates, closing_prices = np.loadtxt(

'../../data/aapl.csv', delimiter=',',

usecols=(1, 6), unpack=True,

dtype='M8[D], f8', converters={1: dmy2ymd})

N = 5

pred_prices = np.zeros(

closing_prices.size - 2 * N + 1)

for i in range(pred_prices.size):

a = np.zeros((N, N))

for j in range(N):

a[j, ] = closing_prices[i + j:i + j + N]

b = closing_prices[i + N:i + N * 2]

#[1]挤后面的为残差

x = np.linalg.lstsq(a, b)[0]

pred_prices[i] = b.dot(x)

mp.figure('Linear Prediction',

facecolor='lightgray')

mp.title('Linear Prediction', fontsize=20)

mp.xlabel('Date', fontsize=14)

mp.ylabel('Price', fontsize=14)

ax = mp.gca()

# 设置水平坐标每个星期一为主刻度

ax.xaxis.set_major_locator(md.WeekdayLocator(

byweekday=md.MO))

# 设置水平坐标每一天为次刻度

ax.xaxis.set_minor_locator(md.DayLocator())

# 设置水平坐标主刻度标签格式

ax.xaxis.set_major_formatter(md.DateFormatter(

'%d %b %Y'))

mp.tick_params(labelsize=10)

mp.grid(linestyle=':')

dates = dates.astype(md.datetime.datetime)

mp.plot(dates, closing_prices, 'o-', c='lightgray',

label='Closing Price')

dates = np.append(dates,

dates[-1] + pd.tseries.offsets.BDay())

mp.plot(dates[2 * N:], pred_prices, 'o-',

c='orangered', linewidth=3,

label='Predicted Price')

mp.legend()

mp.gcf().autofmt_xdate()

mp.show()

线性拟合

原理同上:通过最小二乘法对已有数据拟合出函数,并预测未知数据。

y`代表预测值

y-y`为误差

kx + b = y y`

kx1 + b = y1 y1` (y1-y1`)^2

kx2 + b = y2 y2` (y2-y2`)^2

...

kxn + b = yn yn` (yn-yn`)^2

----------------------------------------------------------

E=f(,k,b)

找到合适的k和b,使E取得最小,由此,k和b所确定的直线为拟合直线。

/ x1 1 \ / k \ / y1` \

| x2 1 | X | b | 接近 | y2` |

| ... | \ / | ... |

\ xn 1/ \ yn`/

a x b

最小二乘法的方法:

= np.linalg.lstsq(a, b)[0]

y = kx + b

kx1 + b = y1' - y1

kx2 + b = y2' - y2

...

kxn + b = yn' - yn

[y1 - (kx1 + b)]^2 +

[y2 - (kx2 + b)]^2 + ... +

[yn - (kxn + b)]^2 = loss = f(k, b)

k, b? -> loss ->min

趋势线示例:

# -*- coding: utf-8 -*-

from __future__ import unicode_literals

import datetime as dt

import numpy as np

import matplotlib.pyplot as mp

import matplotlib.dates as md

def dmy2ymd(dmy):

dmy = str(dmy, encoding='utf-8')

date = dt.datetime.strptime(dmy, '%d-%m-%Y').date()

ymd = date.strftime('%Y-%m-%d')

return ymd

dates, opening_prices, highest_prices, \

lowest_prices, closing_prices = np.loadtxt(

r'C:\Users\Cs\Desktop\数据分析\DS+ML\DS\data\aapl.csv',

delimiter=',', usecols=(1, 3, 4, 5, 6),

unpack=True, dtype='M8[D], f8, f8, f8, f8',

converters={1: dmy2ymd})

trend_points = (highest_prices+lowest_prices+closing_prices)/3

days = dates.astype(int)

# =np.column_stack:将一位矩阵以纵向组合

"""

>>> a=[1,2,3];b=[11,22,33];np.column_stack((a,b))

array([[ 1, 11],

[ 2, 22],

[ 3, 33]])

"""

# 同理还有row_stack(),方法与其刚好相反

# np.ones_like() 生成一个与参数矩阵结构相同但值为1的矩阵

a = np.column_stack((days, np.ones_like(days)))

# 生成a,b的组合,暂时不知道多个变量情况下的拟合的公示,查手册

x = np.linalg.lstsq(a, trend_points)[0]

#print(np.linalg.lstsq(a, trend_points))

# :(array([ 1.81649663e-01, -2.37829793e+03]), array([1267.18780684]), 2, array([8.22882234e+04, 4.62700411e-03]))

#得到的y`的值矩阵

trend_line = days*x[0]+x[1]

mp.figure('Candlestick', facecolor='lightgray')

mp.title('Candlestick', fontsize=20)

mp.xlabel('Date', fontsize=14)

mp.ylabel('Price', fontsize=14)

ax = mp.gca()

# 设置水平坐标每个星期一为主刻度

ax.xaxis.set_major_locator(md.WeekdayLocator(

byweekday=md.MO))

# 设置水平坐标每一天为次刻度

ax.xaxis.set_minor_locator(md.DayLocator())

# 设置水平坐标主刻度标签格式

ax.xaxis.set_major_formatter(md.DateFormatter(

'%d %b %Y'))

mp.tick_params(labelsize=10)

mp.grid(linestyle=':')

dates = dates.astype(md.datetime.datetime)

# 阳线掩码

rise = closing_prices - opening_prices >= 0.01

# 阴线掩码

fall = opening_prices - closing_prices >= 0.01

# 填充色

fc = np.zeros(dates.size, dtype='3f4')

fc[rise], fc[fall] = (1, 1, 1), (0, 0.5, 0)

# 边缘色

ec = np.zeros(dates.size, dtype='3f4')

ec[rise], ec[fall] = (1, 0, 0), (0, 0.5, 0)

mp.bar(dates, highest_prices - lowest_prices, 0,

lowest_prices, color=fc, edgecolor=ec)

mp.bar(dates, closing_prices - opening_prices, 0.8,

opening_prices, color=fc, edgecolor=ec)

mp.plot(dates, trend_line)

# 自动调整水平坐标轴的日期标签

mp.gcf().autofmt_xdate()

mp.show()

裁剪、压缩和累乘

ndarray.clip(min=下限, max=上限)

将调用数组中小于和大于下限和上限的元素替换为下限和上限,返回裁剪后的数组,调用数组保持不变。

ndarray.compress(条件)

返回由调用数组中满足条件的元素组成的新数组。

ndarray.prod()

返回调用数组中所有元素的乘积——累乘。

ndarray.cumprod()

返回调用数组中所有元素执行累乘的过程数组。

import numpy as np

a = np.array([10, 20, 30, 40, 50])

print(a)

b = a.clip(min=15, max=45)

print(b)

c = a.compress((15 <= a) & (a <= 45))

print(c)

d = a.prod()

print(d)

e = a.cumprod()

print(e)

def jiecheng(n):

return n if n == 1 else n * jiecheng(n - 1)

n = 5

print(jiecheng(n))

jc = 1

for i in range(2, n + 1):

jc *= i

print(jc)

print(np.arange(2, n + 1).prod())

结果:

[10 20 30 40 50]

[15 20 30 40 45]

[20 30 40]

12000000

[ 10 200 6000 240000 12000000]

120

120

120

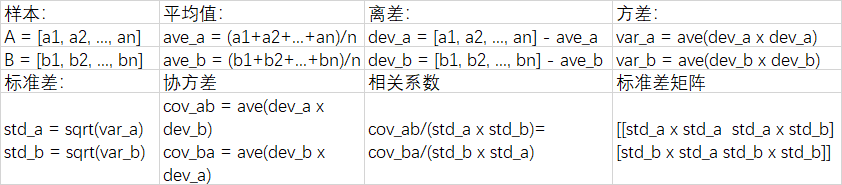

相关性

相关性:

相关系数=相关系数

cov_ab/(std_a x std_b)=cov_ba/(std_b x std_a)

协方差矩阵:

标准差矩阵:

相关性矩阵=协方差矩阵/标准差矩阵:(等号右边是一个矩阵)

| var_a/(std_a x std_a) cov_ab/(std_a x std_b) |

相关性= | cov_ba/(std_b x std_a) var_b/(std_b x std_b) |

numpy.cov(a, b)->相关矩阵的分子矩阵(协方差矩阵)

numpy.corrcoef(a, b)->相关性矩阵

手动和自动计算的例:

import datetime as dt

import numpy as np

import matplotlib.pyplot as mp

import matplotlib.dates as md

def dmy2ymd(dmy):

dmy = str(dmy, encoding='utf-8')

date = dt.datetime.strptime(

dmy, '%d-%m-%Y').date()

ymd = date.strftime('%Y-%m-%d')

return ymd

dates, bhp_closing_prices = np.loadtxt(

'../../data/bhp.csv', delimiter=',',

usecols=(1, 6), unpack=True,

dtype='M8[D], f8', converters={1: dmy2ymd})

vale_closing_prices = np.loadtxt(

'../../data/vale.csv', delimiter=',',

usecols=(6), unpack=True)

bhp_returns = np.diff(

bhp_closing_prices) / bhp_closing_prices[:-1]

vale_returns = np.diff(

vale_closing_prices) / vale_closing_prices[:-1]

ave_a = bhp_returns.mean()

dev_a = bhp_returns - ave_a

var_a = (dev_a * dev_a).sum() / (dev_a.size - 1)

std_a = np.sqrt(var_a)

ave_b = vale_returns.mean()

dev_b = vale_returns - ave_b

var_b = (dev_b * dev_b).sum() / (dev_b.size - 1)

std_b = np.sqrt(var_b)

cov_ab = (dev_a * dev_b).sum() / (dev_a.size - 1)

cov_ba = (dev_b * dev_a).sum() / (dev_b.size - 1)

#相关系数

corr = np.array([

[var_a / (std_a * std_a), cov_ab / (std_a * std_b)],

[cov_ba / (std_b * std_a), var_b / (std_b * std_b)]])

print(corr)

#相关性矩阵的分子矩阵:协方差矩阵

covs = np.cov(bhp_returns, vale_returns)

#相关性矩阵的分母矩阵:标准差矩阵

stds = np.array([

[std_a * std_a, std_a * std_b],

[std_b * std_a, std_b * std_b]])

corr = covs / stds

print(corr)

corr = np.corrcoef(bhp_returns, vale_returns)

print(corr)

mp.figure('Correlation Of Returns',

facecolor='lightgray')

mp.title('Correlation Of Returns', fontsize=20)

mp.xlabel('Date', fontsize=14)

mp.ylabel('Returns', fontsize=14)

ax = mp.gca()

ax.xaxis.set_major_locator(md.WeekdayLocator(

byweekday=md.MO))

ax.xaxis.set_minor_locator(md.DayLocator())

ax.xaxis.set_major_formatter(md.DateFormatter(

'%d %b %Y'))

mp.tick_params(labelsize=10)

mp.grid(linestyle=':')

dates = dates.astype(md.datetime.datetime)

mp.plot(dates[:-1], bhp_returns, c='orangered',

label='BHP')

mp.plot(dates[:-1], vale_returns, c='dodgerblue',

label='VALE')

mp.legend()

mp.gcf().autofmt_xdate()

mp.show()

结果:

[[1. 0.67841747]

[0.67841747 1. ]]

[[1. 0.67841747]

[0.67841747 1. ]]

[[1. 0.67841747]

[0.67841747 1. ]]

结果解读:

在相关性矩阵中,主对角线上的元素是1,代表每个随机变量关于其自身一定是最强的正相关,辅助角上的元素为去除了分散性以后的净相关性指标–相关系数。相关系数介于[-1,1],正负代表了相关性的方向,绝对值表示了相关性的强弱。

多项式拟合

y = p0x^n + p1x^n-1 + p2x^n-2 + … + pn = f(x)

y1’ = f(x1) -> y1

y2’ = f(x2) -> y2

…

yn’ = f(xn) -> yn

(y1-y1’)^2 + (y2-y2’)^2 + … + (yn-yn’)^2

= loss (p0, …, pn)

p0, …, pn = ? -> loss -> min

X = [x1, x2, …, xn] - 自变量

Y = [y1, y2, …, yn] - 实际函数值

Y’= [y1’,y2’,…,yn’] - 拟合函数值

P = [p0, p1, …, pn] - 多项式函数中的系数

Q = [q0, q1, …, qn-1] - 多项式函数导函数的系数

np.polyfit(X, Y, 最高次幂)->P

np.polyval(P, X)->Y’

np.polyder§->Q

y = 4x^3 + 3x^2 + 2x + 1, P=[4,3,2,1]

dy/dx = 12x^2 + 6x + 2, Q=[12, 6, 2]

4x^3 + 3x^2 + 2x + 1 = 0的根:np.roots§(f(x)=0的解)

np.polysub(P1, P2)->两个多项式函数的差函数的系数

y = 4x^3 + 3x^2 + 2x + 1, P1=[4,3,2,1]

y = 5x^4 + x, P2=[5, 0, 0, 1, 0]

y = -5x^4 + 4x^3 + 3x^2 + x + 1

np.polysub(P1, P2)->[-5, 4, 4, 1, 1]

np.polyfit(X, Y, 最高次幂)->P得到一个函数,赋予变量才可以得到值

np.roots§(f(x)=0的解)

np.polysub(P1, P2)->两个多项式函数的差函数的系数

np.polyval(p, days) 对曲线求值

【polyfit】多项式曲线拟合

【polyval】多项式曲线求值

np.polyder§对p函数求导、

# -*- coding: utf-8 -*-

from __future__ import unicode_literals

import datetime as dt

import numpy as np

import matplotlib.pyplot as mp

import matplotlib.dates as md

def dmy2ymd(dmy):

dmy = str(dmy, encoding='utf-8')

date = dt.datetime.strptime(

dmy, '%d-%m-%Y').date()

ymd = date.strftime('%Y-%m-%d')

return ymd

dates, bhp_closing_prices = np.loadtxt(

r'C:\Users\Cs\Desktop\数据分析\DS+ML\DS\data\bhp.csv', delimiter=',',

usecols=(1, 6), unpack=True,

dtype='M8[D], f8', converters={1: dmy2ymd})

vale_closing_prices = np.loadtxt(

r'C:\Users\Cs\Desktop\数据分析\DS+ML\DS\data\vale.csv', delimiter=',',

usecols=(6), unpack=True)

diff_closing_prices = bhp_closing_prices - vale_closing_prices

#将日期转换为int格式,方便计算

days = dates.astype(int)

print(dates)

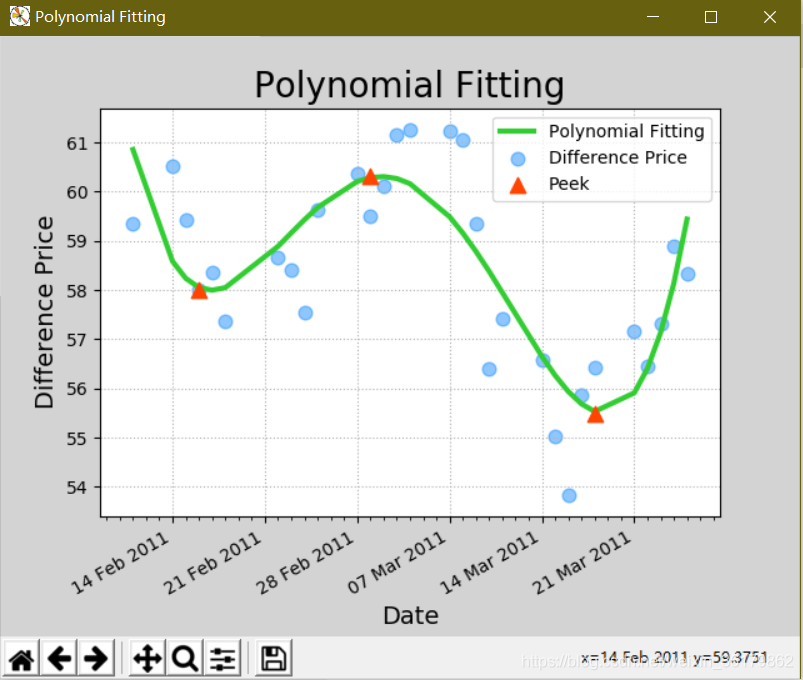

# 拟合4次曲线

p = np.polyfit(days, diff_closing_prices, 4)

# 生成曲线定点的值

poly_closing_prices = np.polyval(p, days)

# 求导

q = np.polyder(p)

#解导数等于0的值

roots_x = np.roots(q)

#求导数等于0的时候函数值(y值)

roots_y = np.polyval(p, roots_x)

mp.figure('Polynomial Fitting', facecolor='lightgray')

mp.title('Polynomial Fitting', fontsize=20)

mp.xlabel('Date', fontsize=14)

mp.ylabel('Difference Price', fontsize=14)

ax = mp.gca()

ax.xaxis.set_major_locator(md.WeekdayLocator(

byweekday=md.MO))

ax.xaxis.set_minor_locator(md.DayLocator())

ax.xaxis.set_major_formatter(md.DateFormatter(

'%d %b %Y'))

mp.tick_params(labelsize=10)

mp.grid(linestyle=':')

dates = dates.astype(md.datetime.datetime)

mp.plot(dates, poly_closing_prices, c='limegreen',

linewidth=3, label='Polynomial Fitting')

mp.scatter(dates, diff_closing_prices, c='dodgerblue',

alpha=0.5, s=60, label='Difference Price')

#将求得的解转换为日期格式

roots_x = roots_x.astype(int).astype(

'M8[D]').astype(md.datetime.datetime)

mp.scatter(roots_x, roots_y, marker='^', s=80,

c='orangered', label='Peek', zorder=4)

mp.legend()

mp.gcf().autofmt_xdate()

mp.show()

提取符号数组

将数组的正负提取出来单独作为一个数组:

两种方法:

- np.sign(源数组)->符号数组

+ -> 1

- -> -1

0 -> 0 - np.piecewise(源数组, 条件序列, 取值序列)->目标数组

针对源数组中的每一个元素,检测其是否符合条件序列中的每一个条件,符合哪个条件就用取值系列中与之对应的值,表示该元素,放到目标数组中返回。

条件序列: [a < 0, a == 0, a > 0]

取值序列: [-1, 0, 1]

# -*- coding: utf-8 -*-

from __future__ import unicode_literals

import numpy as np

a = np.array([70, 80, 60, 30, 40])

print(a)

b = a - 60

print(b)

c = np.sign(b)

print(c)

d = np.piecewise(a, [a < 60, a == 60, a > 60],[-1, 0, 1])

print(d)

例子2(没啥意义,和例子一差不多):

# -*- coding: utf-8 -*-

from __future__ import unicode_literals

import datetime as dt

import numpy as np

import matplotlib.pyplot as mp

import matplotlib.dates as md

def dmy2ymd(dmy):

dmy = str(dmy, encoding='utf-8')

date = dt.datetime.strptime(

dmy, '%d-%m-%Y').date()

ymd = date.strftime('%Y-%m-%d')

return ymd

dates, closing_prices, volumes = np.loadtxt(

r'C:\Users\Cs\Desktop\数据分析\DS+ML\DS\data\bhp.csv', delimiter=',',

usecols=(1, 6, 7), unpack=True,

dtype='M8[D], f8, f8', converters={1: dmy2ymd})

diff_closing_prices = np.diff(closing_prices)

#sign_closing_prices = np.sign(diff_closing_prices)

sign_closing_prices = np.piecewise(

diff_closing_prices, [

diff_closing_prices < 0,

diff_closing_prices == 0,

diff_closing_prices > 0], [-1, 0, 1])

print(volumes)

obvs = volumes[1:] * sign_closing_prices

print(obvs)

mp.figure('On-Balance Volume', facecolor='lightgray')

mp.title('On-Balance Volume', fontsize=20)

mp.xlabel('Date', fontsize=14)

mp.ylabel('OBV', fontsize=14)

ax = mp.gca()

ax.xaxis.set_major_locator(md.WeekdayLocator(

byweekday=md.MO))

ax.xaxis.set_minor_locator(md.DayLocator())

ax.xaxis.set_major_formatter(md.DateFormatter(

'%d %b %Y'))

mp.tick_params(labelsize=10)

mp.grid(axis='y', linestyle=':')

dates = dates[1:].astype(md.datetime.datetime)

mp.bar(dates, obvs, 1.0, color='dodgerblue',

edgecolor='white', label='OBV')

mp.legend()

mp.gcf().autofmt_xdate()

mp.show()

杂项

numpy.diff(a, n=1,axis=-1)

沿着指定轴计算第N维的离散差值

参数:

a:输入矩阵

n:可选,代表要执行几次差值

axis:默认是最后一个

示例:

>>> a=np.arange(2,14)

>>> a.shape=(3,4)

>>> a

array([[ 2, 3, 4, 5],

[ 6, 7, 8, 9],

[10, 11, 12, 13]])

>>> np.diff(a)

array([[1, 1, 1],

[1, 1, 1],

[1, 1, 1]])