一、单因子选股策略--小市值策略

二、多因子选股策略--市值+ROE(净资产收益率)选股策略

一、单因子选股策略--小市值策略

因子选股策略

因子:选择股票的某种标准

增长率、市值、市盈率、ROE(净资产收益率)............

选股策略:

对于某个因子,选取表现最好(因子最大或最小)的N支股票持仓

每隔一段时间调仓一次,如果一段时间没有涨可以卖了换

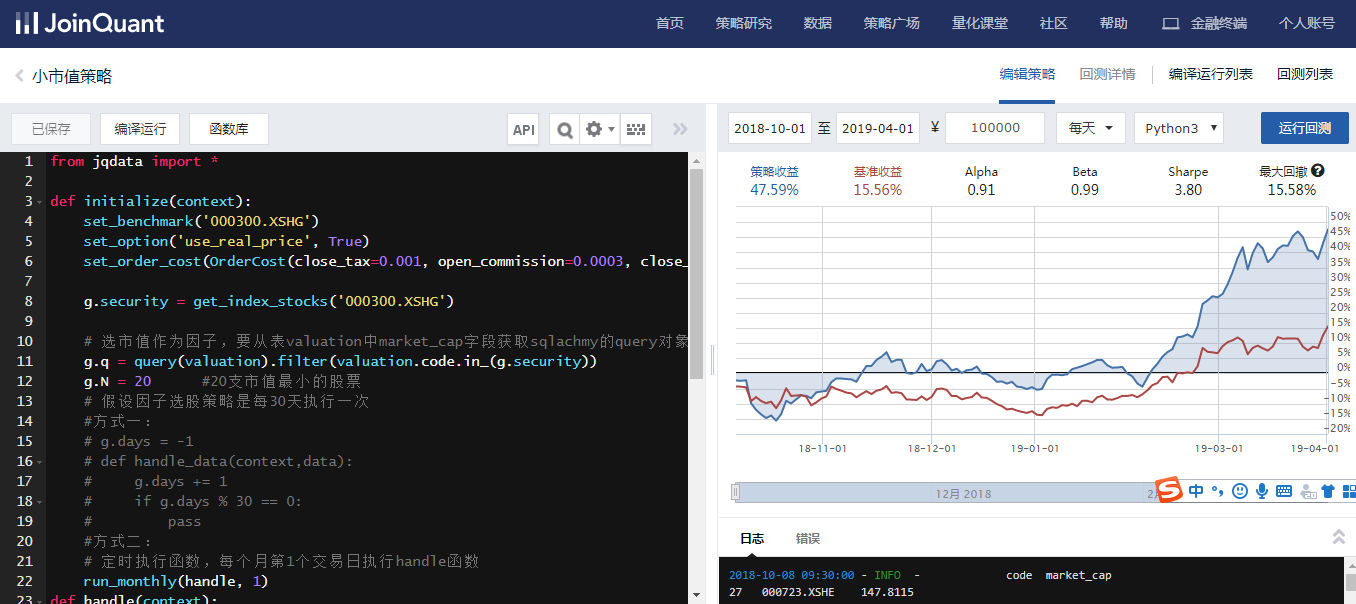

小市值策略:选取股票池中市值最小的N只股票持仓

例如:选择20支市值最小的股票持有,一个月调一次仓:

from jqdata import * def initialize(context): set_benchmark('000300.XSHG') set_option('use_real_price', True) set_order_cost(OrderCost(close_tax=0.001, open_commission=0.0003, close_commission=0.0003, min_commission=5), type='stock') g.security = get_index_stocks('000300.XSHG') # 选市值作为因子,要从表valuation中market_cap字段获取sqlachmy的query对象 g.q = query(valuation).filter(valuation.code.in_(g.security)) g.N = 20 #20支市值最小的股票 # 假设因子选股策略是每30天执行一次 #方式一: # g.days = -1 # def handle_data(context,data): # g.days += 1 # if g.days % 30 == 0: # pass #方式二: # 定时执行函数,每个月第1个交易日执行handle函数 run_monthly(handle, 1) def handle(context): df = get_fundamentals(g.q)[['code','market_cap']] df = df.sort_values('market_cap').iloc[:g.N,:] #选出20支 print(df) to_hold = df['code'].values for stock in context.portfolio.positions: if stock not in to_hold: order_target(stock, 0) to_buy = [stock for stock in to_hold if stock not in context.portfolio.positions] if len(to_buy) > 0: cash_per_stock = context.portfolio.available_cash / len(to_buy) for stock in to_buy: order_value(stock, cash_per_stock)

二、多因子选股策略--市值+ROE(净资产收益率)选股策略

多因子选股策略

如何同时综合多个因子来选股?

评分模型:

每个股票针对每个因子进行评分,将评分相加

选出总评分最大的N只股票持仓

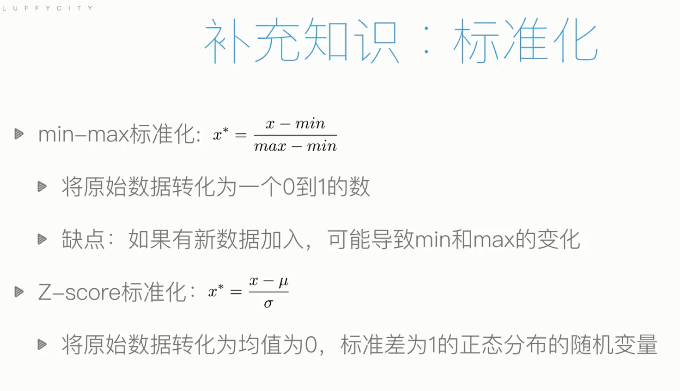

如何计算股票在某个因子下的评分:归一化(标准化),下面是两种标准化的方式

比如选择两个因子:市值和ROE(净资产收益率)作为选股评价标准

from jqdata import * def initialize(context): set_benchmark('000300.XSHG') set_option('use_real_price', True) set_order_cost(OrderCost(close_tax=0.001, open_commission=0.0003, close_commission=0.0003, min_commission=5), type='stock') g.security = get_index_stocks('000300.XSHG') # 选市值作为因子,要从表valuation中market_cap字段获取sqlachmy的query对象 g.q = query(valuation, indicator).filter(valuation.code.in_(g.security)) g.N = 20 #20支股票 run_monthly(handle, 1) def handle(context): df = get_fundamentals(g.q)[['code','market_cap','roe']] df['market_cap'] = (df['market_cap']-df['market_cap'].min())/(df['market_cap'].max()-df['market_cap'].min()) df['roe'] = (df['roe']-df['roe'].min())/(df['roe'].max()-df['roe'].min()) # 双因子评分:市盈率越大越好,市值越小越好 df['score'] = df['roe'] - df['market_cap'] # 对评分排序,选最大的20支股票 df = df.sort_values('score').iloc[-g.N:,:] to_hold = df['code'].values for stock in context.portfolio.positions: if stock not in to_hold: order_target(stock, 0) to_buy = [stock for stock in to_hold if stock not in context.portfolio.positions] if len(to_buy) > 0: cash_per_stock = context.portfolio.available_cash / len(to_buy) for stock in to_buy: order_value(stock, cash_per_stock)