版权声明:本文为博主原创文章,未经博主允许不得转载。 https://blog.csdn.net/brucewong0516/article/details/84768464

首先我们直接看官方的文档:

DataFrame.resample(rule, how=None, axis=0, fill_method=None, closed=None,

label=None, convention='start', kind=None, loffset=None,

limit=None, base=0, on=None, level=None)

- 聚合的时间参数rule

- 参数如下:

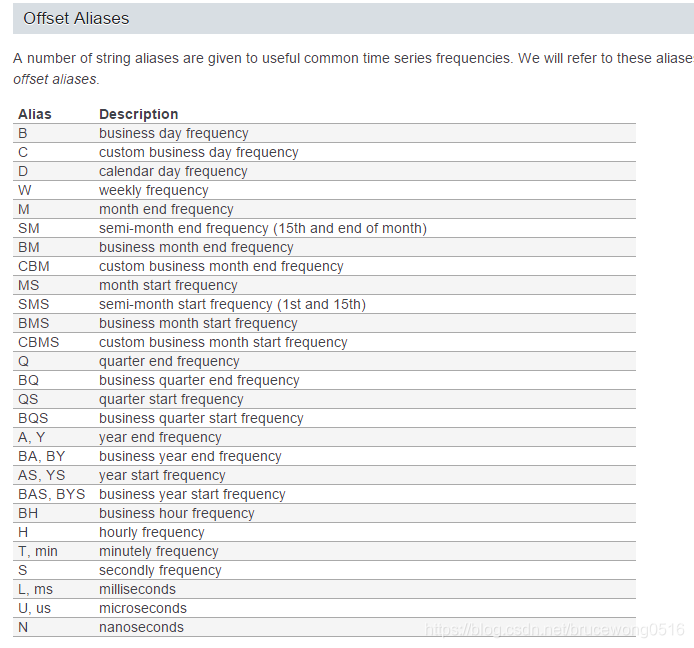

rule : 表示目标转换的偏移字符串或对象,一般是时间参数,比如“M”,“A”,“Q”,“BM”,“BA”,“BQ”和“W”;

axis : int, optional, default 0

closed : {‘right’, ‘left’};间隔的哪一侧是关闭的,对于除“M”,“A”,“Q”,“BM”,“BA”,“BQ”和“W”之外的所有频率偏移,默认值为“左”,其默认值均为“右”

label : {‘right’, ‘left’};用于标记bins,间隔的哪一侧是关闭的,对于除“M”,“A”,“Q”,“BM”,“BA”,“BQ”和“W”之外的所有频率偏移,默认值为“左”,其默认值均为“右”

convention : {‘start’, ‘end’, ‘s’, ‘e’}:For PeriodIndex only, controls whether to use the start or end of rule

kind: {‘timestamp’, ‘period’}, optional;Pass ‘timestamp’ to convert the resulting index to a DateTimeIndex or ‘period’ to convert it to a PeriodIndex. By default the input representation is retained.

loffset : 调整重新采样的时间标签

on : 对于DataFrame,要使用的列而不是索引进行重新采样。列必须与日期时间相似的数据。

实例

1.1 创建时间索引,并查看按时间合并后进行求和计算

#首先创建一个包含9个一分钟时间戳的系列

index = pd.date_range('1/1/2000', periods=9, freq='T') # 生成频率为每分钟的数据

series = pd.Series(range(9), index=index)

series

Out[31]:

2000-01-01 00:00:00 0

2000-01-01 00:01:00 1

2000-01-01 00:02:00 2

2000-01-01 00:03:00 3

2000-01-01 00:04:00 4

2000-01-01 00:05:00 5

2000-01-01 00:06:00 6

2000-01-01 00:07:00 7

2000-01-01 00:08:00 8

Freq: T, dtype: int64

series.resample('3T')

# 3T就是rule,合并的方向默认是axis = 0;

Out[34]: DatetimeIndexResampler [freq=<3 * Minutes>, axis=0, closed=left, label=left, convention=start, base=0]

series.resample('3T').sum()

Out[35]:

2000-01-01 00:00:00 3

2000-01-01 00:03:00 12

2000-01-01 00:06:00 21

Freq: 3T, dtype: int64

1.2 close和left的左右

# 间隔的哪一侧是关闭的,对于除“M”,“A”,“Q”,“BM”,“BA”,“BQ”和“W”之外的所有频率偏移,默认值为“左”,其默认值均为“右”

series.resample('W')

Out[37]: DatetimeIndexResampler [freq=<Week: weekday=6>, axis=0, closed=right, label=right, convention=start, base=0]

series.resample('T')

Out[38]: DatetimeIndexResampler [freq=<Minute>, axis=0, closed=left, label=left, convention=start, base=0]

# 如果是T分钟频率,合并后的K线是从合并的时间开始计算,如果是2T,就从开始的第一根往后数2根;

series.resample('T').sum()

Out[40]:

2000-01-01 00:00:00 0

2000-01-01 00:01:00 1

2000-01-01 00:02:00 2

2000-01-01 00:03:00 3

2000-01-01 00:04:00 4

2000-01-01 00:05:00 5

2000-01-01 00:06:00 6

2000-01-01 00:07:00 7

2000-01-01 00:08:00 8

Freq: T, dtype: int64

# 对比可以看出是左侧关闭的

series.resample('2T').sum()

Out[42]:

2000-01-01 00:00:00 1

2000-01-01 00:02:00 5

2000-01-01 00:04:00 9

2000-01-01 00:06:00 13

2000-01-01 00:08:00 8

Freq: 2T, dtype: int64

# 如果是W周频率,那么整个合并的结果归集到最后一天

series = pd.Series(range(9), index=index)

series.resample('W').sum()

Out[53]:

2000-01-02 0

2000-01-09 3

2000-01-16 12

2000-01-23 13

2000-01-30 8

Freq: W-SUN, dtype: int64

series

Out[54]:

2000-01-01 0

2000-01-04 1

2000-01-07 2

2000-01-10 3

2000-01-13 4

2000-01-16 5

2000-01-19 6

2000-01-22 7

2000-01-25 8

Freq: 3D, dtype: int64

1.3 自定义label的方向,也就是数据归集的位置

index = pd.date_range('1/1/2000', periods=9, freq='T') # 生成频率为每分钟的数据

series = pd.Series(range(9), index=index)

series.resample('3T', label='right').sum()

Out[57]:

2000-01-01 00:03:00 3

2000-01-01 00:06:00 12

2000-01-01 00:09:00 21

Freq: 3T, dtype: int64

1.4 自定义close的方向

index = pd.date_range('1/1/2000', periods=9, freq='T') # 生成频率为每分钟的数据

series = pd.Series(range(9), index=index)

series

Out[63]:

2000-01-01 00:00:00 0

2000-01-01 00:01:00 1

2000-01-01 00:02:00 2

2000-01-01 00:03:00 3

2000-01-01 00:04:00 4

2000-01-01 00:05:00 5

2000-01-01 00:06:00 6

2000-01-01 00:07:00 7

2000-01-01 00:08:00 8

Freq: T, dtype: int64

# 被合并的数据的最右不显示,关闭箱间隔的右侧

series.resample('3T', closed='right').sum()

Out[64]:

1999-12-31 23:57:00 0

2000-01-01 00:00:00 6

2000-01-01 00:03:00 15

2000-01-01 00:06:00 15

Freq: 3T, dtype: int64

1.5 上采用成30s的数据,加上asfreq()

series.resample('30S').asfreq()

Out[66]:

2000-01-01 00:00:00 0.0

2000-01-01 00:00:30 NaN

2000-01-01 00:01:00 1.0

2000-01-01 00:01:30 NaN

2000-01-01 00:02:00 2.0

2000-01-01 00:02:30 NaN

2000-01-01 00:03:00 3.0

2000-01-01 00:03:30 NaN

2000-01-01 00:04:00 4.0

2000-01-01 00:04:30 NaN

2000-01-01 00:05:00 5.0

2000-01-01 00:05:30 NaN

2000-01-01 00:06:00 6.0

2000-01-01 00:06:30 NaN

2000-01-01 00:07:00 7.0

2000-01-01 00:07:30 NaN

2000-01-01 00:08:00 8.0

Freq: 30S, dtype: float64

1.6 将系列上采样到30秒的箱中,并使用pad方法填充NaN值

series.resample('30S').pad()[0:5]

Out[67]:

2000-01-01 00:00:00 0

2000-01-01 00:00:30 0

2000-01-01 00:01:00 1

2000-01-01 00:01:30 1

2000-01-01 00:02:00 2

Freq: 30S, dtype: int64

1.7 将系列上上采样30秒的箱中,并使用bfill方法填充NaN值

series.resample('30S').bfill()[0:5]

Out[68]:

2000-01-01 00:00:00 0

2000-01-01 00:00:30 1

2000-01-01 00:01:00 1

2000-01-01 00:01:30 2

2000-01-01 00:02:00 2

Freq: 30S, dtype: int64

1.8 通过apply传递自定义功能

def custom_resampler(array_like):

return np.sum(array_like)+5

import numpy as np

series.resample('3T').apply(custom_resampler)

Out[74]:

2000-01-01 00:00:00 8

2000-01-01 00:03:00 17

2000-01-01 00:06:00 26

Freq: 3T, dtype: int64

1.9 对于具有PeriodIndex的Series,关键字约定可用于控制是否使用规则的开头或结尾。

s = pd.Series([1, 2], index=pd.period_range('2012-01-01',

freq='A',

periods=2))

# 上采样需要asfreq( )

s.resample('M', convention='start').asfreq().head()

Out[76]:

2012-01 1.0

2012-02 NaN

2012-03 NaN

2012-04 NaN

2012-05 NaN

Freq: M, dtype: float64

s.resample('M', convention='end').asfreq()

Out[78]:

2012-12 1.0

2013-01 NaN

2013-02 NaN

2013-03 NaN

2013-04 NaN

2013-05 NaN

2013-06 NaN

2013-07 NaN

2013-08 NaN

2013-09 NaN

2013-10 NaN

2013-11 NaN

2013-12 2.0

Freq: M, dtype: float64

1.10 对于DataFrame对象,关键字on可用于指定列而不是重新取样的索引

df = pd.DataFrame(data=9*[range(4)], columns=['a', 'b', 'c', 'd'])

df['time'] = pd.date_range('1/1/2000', periods=9, freq='T')

df.resample('3T', on='time').sum()

Out[81]:

a b c d

time

2000-01-01 00:00:00 0 3 6 9

2000-01-01 00:03:00 0 3 6 9

2000-01-01 00:06:00 0 3 6 9

1.11 how,未来不会用的功能

index = pd.date_range('1/1/2000', periods=9, freq='T') # 生成频率为每分钟的数据

series = pd.Series(range(9), index=index)

series.resample('2T',how='last')

Out[83]:

2000-01-01 00:00:00 1

2000-01-01 00:02:00 3

2000-01-01 00:04:00 5

2000-01-01 00:06:00 7

2000-01-01 00:08:00 8

Freq: 2T, dtype: int64

series.resample('2T',how='mean')

Out[84]:

2000-01-01 00:00:00 0.5

2000-01-01 00:02:00 2.5

2000-01-01 00:04:00 4.5

2000-01-01 00:06:00 6.5

2000-01-01 00:08:00 8.0

Freq: 2T, dtype: float64