.1.从投资组合的方差公式说起

发现一篇详细的博客介绍了详细的推导过程: http://www.cnblogs.com/simbon/p/7979638.html

所以可以理解为,投资组合的总方差等于组合方案中的所有两两组合的投资比例乘他们各自之间的协方差。

之后会常用的rho可以理解为每个投资选择之间的correlation,实际中可以类比为两家股票之间的关系。

2.对rho的进一步探讨:(假设投资方案只包含两个投资A和B)

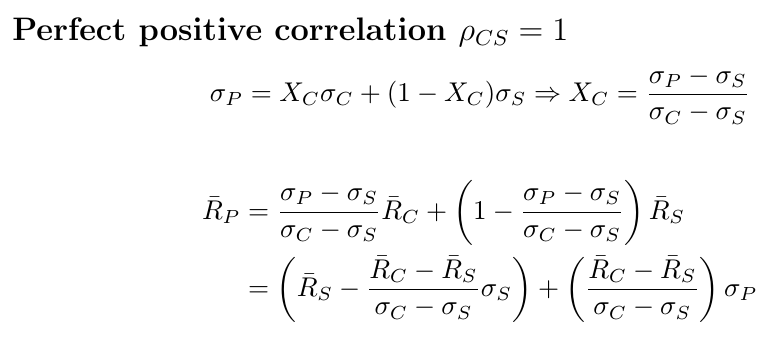

2.1当rho=+1时,A和B的关系称为Perfect positive correlation,可以理解为,AB会同步的增减

已知:

把rho=1带入平均收益和标准差, 然后使用标准差表示投资比例X:

化简平均收益表达式,可以发现

对应的图像:( Relationship between expected return and standard deviation when r = +1)

2.2 当rho为-1时:

从图中可以发现有一个点的标准差为0,也就是没有危险,100%可以获得对应Y轴的收益:

2.3 除了上述两种特殊情况外,更为常见的应该是两个asset returns 没有correlation>

The relationship between expected return and standard deviation for various correlation coefficients.

S-A-C 完全正相关

S-B-C完全负相关

S-O-C相较于前两者更接近0,不严格相关

2.4 完全不相关rho=0:

此时的预期收益和风险图:

2.5 更中间的情况(2.3的量化)

2.6 允许做空(short sales )的情况 (rho = 0.5)

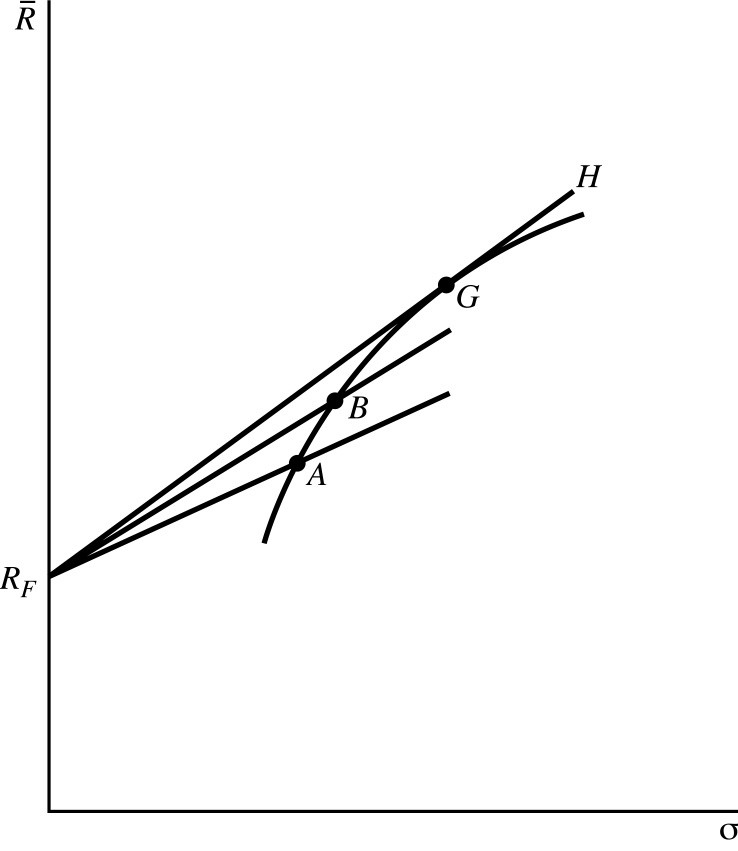

3. 有了之前的预期回报于风险的关系之后,我们得到了一个可以满足只想冒可量化任何风险的投资人的投资方案,来实现可控风险借贷投资:

(这里的riskless rate指的是无风险利率,是指将资金投资于某一项没有任何风险的投资对象而能得到的利息率。这是一种理想的投资收益。 在资本市场上,美国国库券(国债Treasury bond)的利率通常被公认为市场上的无风险利率,这是因为美国政府的公信力被市场认可不会出现违约的行为。)

在2的只有两个asset的设定下,假定其中一个是无风险利率,那么如何将其与有风险投资组合起来,才能实现整体投资组合的最佳收益

这也被称为Efficient frontier. (with riskless lending and borrowing)

"The efficient frontier is the entire length of the ray extending through RF - B, with different points along the ray RF- B representing different amounts of borrowing and/or lending in combination with the optimum portfolio - B - of risky assets."

Expected return and risk when the risk-free rate is mixed with portfolio A.

Combinations of the riskless asset and various risky portfolios.

所以投资人应该在Rf - G阶段从riskless asset贷款,在G-H阶段存钱(买入)

这就对应了1981年诺别尔奖获得者Tobin的Separation theorem: All investors will hold combinations of the cash account and portfolio G

The efficient frontier with lending but not borrowing at the riskless rate.

The efficient frontier with riskless lending and borrowing at different rates.(更为普世的状态,借钱的利息比存钱的利息高)

4.