Selling Covered Call Strategy (Covered_call)

The strategy of selling covered call options is one of the most basic income strategies. The main operation of this strategy is to sell the corresponding call option contract while holding the underlying asset, in order to obtain rent from the underlying asset held. a way. If the price of the underlying asset rises above the exercise price, then the call option sold will be exercised, then the investor can sell the underlying asset held in his hand, and the investor will receive the initial option premium equal to the amount of the underlying asset at the beginning of the period. The upside gain between exercise options. If the price of the underlying asset is equal to the exercise price of the call option, the investor will receive the option premium. If the price of the underlying asset falls, the premium received from the call option sold at the beginning of the period can make up for the loss of the fall in the price of the underlying asset to a certain extent.

Generally speaking, the strategy of selling covered call options often sells out-of-the-money options, so that the underlying asset has more room for growth. In other words, the potential income of this strategy comes from the premium income from selling call options and the amount of the underlying asset. There are two parts of income: income from rising asset prices.

1.1 Strategy Overview

Trend: Bullish or Neutral

Volatility: N/A

Asset leg: Buy the underlying asset and sell the put option

Maximum risk: There is an upper limit

Maximum profit: There is an upper limit

Strategy Type: Income Strategy

1.2 Strategy risks and benefits

The strategy of selling covered call options can be mainly divided into selling out-of-the-money covered calls and in-the-money covered call options. For the out-of-the-money covered call strategy, it can provide higher potential returns, but the degree of risk protection is limited. Therefore, investors can build a more aggressive offensive position by selling out-of-the-money call options. At this time, the investor is bullish on the price of the underlying asset. If the investor is neutral or slightly bearish on the price of the underlying asset, , then selling in-the-money call options for a covered strategy is more appropriate. If investors are bearish on the price of the underlying asset, then the investor should sell the underlying asset.

1.3 Instructions to sell covered call options

When establishing a selling covered call strategy, it is not fixed whether the underlying asset is bought first or the call option is sold first. Generally speaking, the only way is to make both sides of the covered call strategy sell at the desired price. That is, buying the underlying asset and selling the call option at the same time. If an investor buys the underlying asset first or sells a call option first, the investor's position is at risk.

Investors who sell covered call strategies want to combine high potential gains with adequate downside protection as much as possible. Selling out-of-the-money call options to cover can provide higher potential returns, but provides less downside protection, while selling in-the-money call options to cover can provide more downside protection, but only provides less downside protection. potential earnings. In order to obtain higher potential returns and higher downside protection at the same time, investors can diversify the strategy, that is, sell a portion of the in-the-money call options for coverage and sell a portion of the out-of-the-money call options for coverage. Convert.

1.4 Follow-up actions

After the strategy of selling covered call options is constructed, the position needs to be closely monitored. If the price of the underlying asset drops too much, adjustments need to be made in a timely manner, or when the price of the underlying asset changes slightly and the call option is approaching expiration, adjustments are also required. Corresponding follow-up actions.

If the underlying asset is higher than the exercise price when the option expires, and the investor sells the underlying asset to exercise the option, or the price of the underlying asset is lower than the exercise price when the option expires, the call option will expire worthless. For those who do not take As with any measure, more proactive behavior is necessary. Generally speaking, it can be divided into three types: protective measures taken when the price of the underlying asset falls, offensive measures taken when the price of the underlying asset rises, and actions taken to avoid assignment when the time value of in-the-money call options disappears.

If the price of the underlying asset drops sharply and no measures are taken, then selling covered call options will face a large loss, because this strategy is a strategy with limited income, so investors should try to limit losses, otherwise they will lose once It will offset several profits. The simplest operation is to close the underlying asset. Another better method is to buy back the call option originally sold, and then sell another call option with a different strike price or expiration date to replace it. This operation is called a downward move, because the new call option The exercise price of the option is lower. Although this strategy can provide better protection against further declines in the price of the underlying asset, it also limits the profit margin for an increase in the price of the underlying asset because the exercise price of the new option is lower than that of the old option. In other words, the only possible reason for the poor performance of the downward move operation is that the price of the underlying asset has rebounded significantly.

Of course, when the price of the underlying asset falls, investors can move part of their positions downwards, which can balance the protection against market declines with the retention of profits from market increases, that is, part of the positions can be moved downwards. Move down to the warehouse.

When the price of the underlying asset rises, investors can wait for the assignment of the underlying asset to exercise the option, or they can close the position in advance or move the call option upward. The operation of moving the position upward is to buy back the originally sold call option and sell a call option with a higher exercise price. Generally speaking, moving a position upward will incur additional expenses, which is different from moving a position downward to generate income. At the same time, although moving a position upward increases the potential for investors to make profits, once the price of the underlying asset changes direction, When, the risk of the position will be exposed. Therefore, when the price of the underlying asset rises, don't forget to construct the risk control goal of selling covered call options, and think about whether to put profits at risk.

When the price of the underlying asset rises and investors do not want their position to be assigned to sell, they can sell a part of the underlying asset and use this part of the income to buy back the previously sold call options. In this way, the investor avoids the entire position being assigned. Assigned risks.

As the expiration date of the option approaches, the time value of the call option sold will gradually disappear. Then the investor can buy back the previously sold call option and sell an option with the same exercise price and a longer expiration time. Call options.

1.5 Python practice

Underlying asset: ChinaAMC SSE 50 ETF

Options: 50ETF Call Options

Backtesting time: June 1, 2022 - July 20, 2022

Idea: Hold the underlying assets, sell call options, swap positions at the end of the month, and calculate the out-of-the-money first-third and at-the-money option contract strategy net values respectively.

Part of the code:

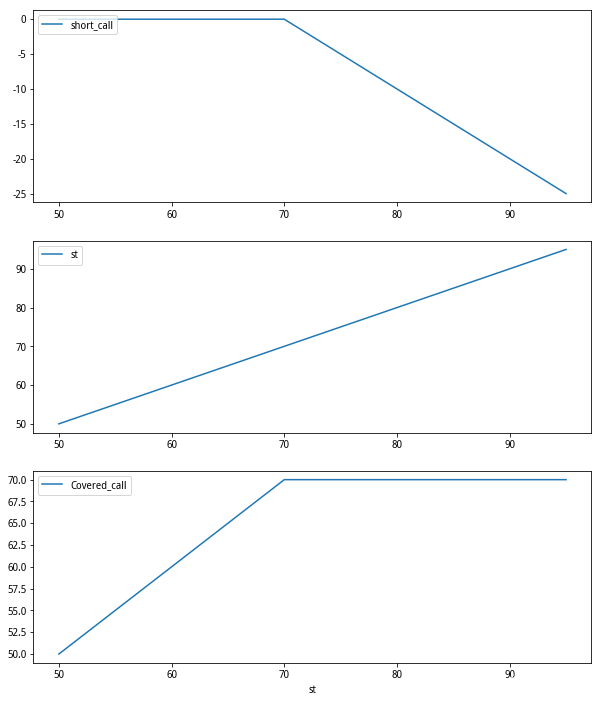

class Covered_call(object):

def __init__(self,st,k):

self.st=st

self.k=k

def option_value(self):

return -np.maximum(self.st-self.k,0)

def plot_return(self):

value=self.option_value()

plt.figure(figsize=(10,12))

plt.subplot(311)

plt.plot(st,value,label='short_call')

plt.legend(loc='upper left')

plt.subplot(312)

plt.plot(st,st,label='st')

plt.legend(loc='upper left')

plt.subplot(313)

plt.plot(st,value+st,label='Covered_call')

plt.xlabel('st')

plt.legend(loc='upper left')

plt.show()

st=np.arange(50,100,5)

k=70

Covered_call(st,k).plot_return()Covered_call_return:

Strategy Equity Curve:

Strategy income indicators: