Using "unevenness of heat and cold" to describe the current automotive chip track could not be more appropriate.

This week, Nvidia announced that its revenue for the second fiscal quarter (May-July) reached a record US$13.5 billion, significantly exceeding the previous consensus estimate of slightly more than US$11 billion, and the year-on-year growth rate reached 101%. .

Among them, most of the revenue growth came from the data center sector. Due to the continuous benefit from the hot AIGC track, revenue increased by 171% year-on-year to $10.3 billion.

However, the company's fiscal second-quarter automotive revenue ($253 million) fell 15% sequentially from the previous quarter and rose just 15% from the year-earlier period. The automotive business is also the part with the lowest growth rate among the four major business segments (data center, games, professional services, and automobiles).

In this regard, Nvidia said that compared with the same period last year, the growth was due to the mass production and delivery of autonomous driving platforms of several new energy vehicle manufacturers. The quarter-on-quarter decline reflects lower overall auto demand, especially in China.

Data show that in the first fiscal quarter of this year (February-April), Nvidia's automotive business revenue was US$296 million, a quarter-on-quarter increase of 1% and a year-on-year increase of 114%. Considering that there is a certain delay window between chip delivery and vehicle sales, it may also explain some problems.

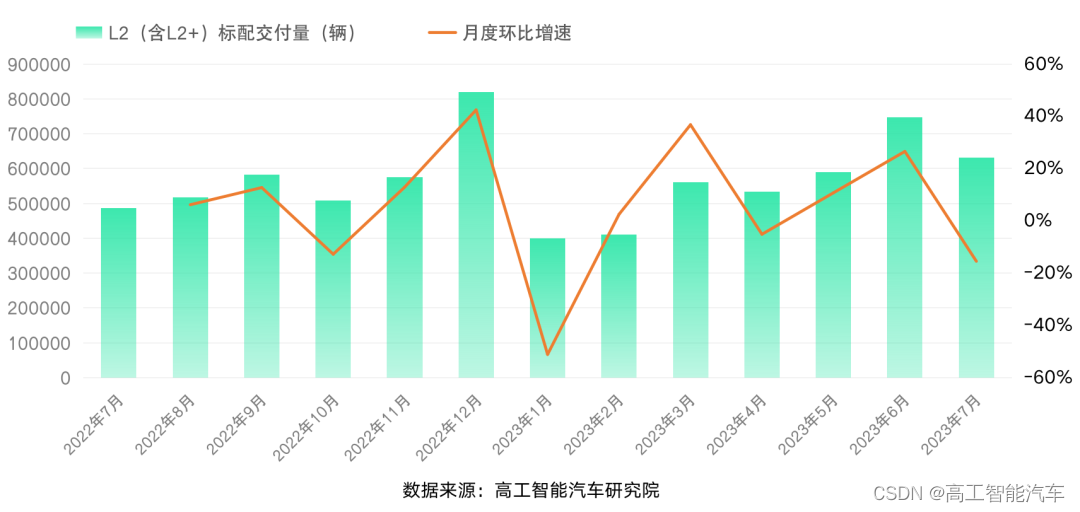

As one of the main contributing markets of Nvidia’s Xavier/Orin platform, the monitoring data of Gaogong Intelligent Vehicle Research Institute shows that from January to June 2023, new cars equipped with Nvidia’s intelligent driving computing platform (excluding cockpit) will be delivered as standard. 161,600 vehicles, a year-on-year increase of 288.46%.

At the same time, considering that the second half of 2022 is the rapid introduction period of the pre-installation of the Orin platform, Gaogong Intelligent Vehicle Research Institute predicts that the growth rate of Nvidia's automotive business may enter a fluctuation cycle in the second half of the year.

The data shows that in the Chinese market, the average monthly delivery of the Orin platform in the second half of 2022 will be around 20,000 vehicles (according to the statistical caliber of bicycles, some models are equipped with multiple Orins), and around 25,000 vehicles from January to June this year. In the second half of the year, it will rise to 40,000 vehicles per month, but the year-on-year growth rate will also decline sharply.

In the past few years, Nvidia has not given too many "words" to the automotive business in every quarterly report and annual report disclosure, except for the ever-increasing fixed-point scale figure (as of the end of the first quarter of this year, it was 14 billion US dollars, an annual increase of 30 One hundred million U.S. dollars).

In fact, Nvidia also issued a negative warning on the automotive business in April this year. "Because Chinese customers are adjusting production plans due to lower-than-expected end-market demand. We expect this situation to continue until the end of this year."

As one of Nvidia's possible largest customers in the future, the BYD Dynasty and Ocean series models are expected to enter the scale-up cycle starting in 2024. However, Tengshi’s new model, which is the first to get on the Orin, will not be able to bring substantial scale in the short term.

For example, for Tenshi N7, the Orin version is optional. The 2023 sales target of the Denza brand is only 150,000 vehicles, which is not even as high as the annual sales of a single model of the Dynasty and Ocean series.

In addition, considering that the price of Denza N7 has reached the range of 300,000 yuan, for the Dynasty and Ocean series with lower positioning, the configuration rate of the follow-up Orin platform is still unknown.

In fact, as the upstream core link of smart cars, chip manufacturers' expectations for the market are predictable. From the data point of view, taking the Chinese passenger car market as an example, the growth rate of L2 and above intelligent driving is still in an unstable cycle.

As one of the major suppliers of global automotive-grade MCUs and SoCs, in the second quarter of this year, the profit margin of Renesas Electronics’ automotive business dropped by 1.2 percentage points from the previous quarter. "Client cash flow is tight and many companies are struggling to keep inventories under control."

Every family has hard-to-read scriptures, and another listed company for automotive chips has a similar situation.

"Customers are very cautious in the first half of 2023, resulting in lower than normal growth rates, but we have seen a pick-up in the second half of the year, with deliveries expected to grow 16% year-on-year in the second half of the year, much higher than in the first half." This is Mobileye The prediction at the company's semi-annual report conference recently.

According to public data, in the first half of this year, Mobileye achieved revenue of US$912 million, an increase of only 6.79% year-on-year, far lower than the 35% in 2022. In terms of net profit, there was still a loss of US$107 million, an increase of 59.70% over the same period last year.

Mobileye is under different pressure than Nvidia, though.

The company pointed out that as some joint venture brands in the Chinese market and China's local new energy car companies continue to seek breakthroughs in advanced intelligent driving technology, "we are facing increasing competitive pressure."

At present, in the Chinese market, several companies such as Nvidia, Horizon, TI, and Black Sesame Smart occupy most of the mass-produced and fixed-point model markets of NOA (including integrated parking and parking).

The good news is that Mobileye's partners are still developing platform solutions based on the EyeQ6 series. For example, Jingwei Hengrun is still actively following up Mobileye's EyeQ6/EyeQ Ultra solution.

But the bad news is that several partners, including ZF and Aptiv, are choosing the Horizon platform to develop solutions that meet the needs of customers in the Chinese market. In addition, Jingwei Hengrun and Zhixing Technology have already begun to deliver domain control solutions based on the TI TDA4 platform.

In addition, Mobileye's SuperVison advanced program is not progressing as expected. The company expects to have five new vehicles equipped with the solution put into production by the first quarter of 2024. This figure is far behind Nvidia and Horizon.

At the same time, as the first customer of Mobileye EyeQ5 in China, Jikr is also accelerating the self-development of smart driving solutions, and officially announced that it will be equipped with Nvidia's next-generation vehicle computing platform DRIVE Thor.

Previously, Mobileye acknowledged that some of their competitors have more or better resources than their own. For example, Nvidia and Qualcomm have preemptively released cross-domain super-computing computing solutions for the next-generation vehicle electronic architecture, and each occupy the top share of high-end smart driving and smart cockpits.

In the Chinese market, in the popular market below 150,000 yuan, Chinese local chip suppliers have begun to seize market share, and car companies have put more emphasis on the cost-effectiveness and openness of solutions, as well as localized Tier1 ecosystem resources.

At the same time, in the high-end market of more than 300,000 yuan, various schemes have also launched fierce competition.

Just at the beginning of this month, on August 3, Ideal L9 Pro was launched at a price of 429,800 yuan, equipped with the Horizon Journey 5 chip, creating a precedent for Chinese high-performance intelligent driving computing solution providers to enter the market above 400,000 yuan for the first time.

In addition, Huawei is also developing intelligent software and hardware businesses.

In addition to Huawei's car manufacturing, Huawei has recently reached a strategic cooperation with Chang'an Deep Blue. The two parties will cooperate in the field of automotive intelligence, including carrying Huawei's intelligent driving system ADS.

Of course, in addition to this, a number of local in-vehicle computing solution suppliers, including Black Sesame Smart, Aixin Yuanzhi, Xinli Smart, and Yixing Smart, will also gradually enter the pre-installation delivery cycle. For example, Black Sesame Smart predicts that shipments this year will reach about 100,000 pieces, four times the shipments in 2022.

At the same time, new entrants continue to emerge.

For example, judging from the current public recruitment information, the layout of Momenta's self-developed chips has been confirmed. For example, the NPU architecture design position is responsible for evaluating third-party IP and self-developed IP.