Optimal ratios calculated hedging

Cross-hedging refers to the underlying assets and quilt Paul inconsistencies assets in futures contracts, such as a company equipped with the SSE 180 Index ETF fund, but not the Shanghai Futures contracts 180 index on the market, the company can only choose the Shanghai and Shenzhen 300 index futures, Shanghai 50 CSI 500 index futures or index futures for hedging.

Optimal hedging ratio is also called the minimum variance hedging ratio, denoted h *, indicates how many futures contracts hedged asset price changes in a security unit needs to hedge. Construction of linear equations + [alpha] = H [Delta] S * × [Delta] F + [epsilon], where [Delta] S and [Delta] F respectively in the hedging period, changes apply security asset prices for futures and hedging price changes. Many times ΔS and ΔF with their daily return data instead. The linear regression calculation can be obtained H * = ρσ S / [sigma] F. = [Delta] S / [Delta] F, a process similar to find β coefficient of CAPM.

Assume that a fund company to configure the SSE 180 Index ETF fund, the company can only choose the Shanghai and Shenzhen 300 index futures contract IF1812, IH1812 SSE 50 Index futures contract or the CSI 500 Index futures contracts to hedge IC1812, listing the three contracts daily average is April 23, 2018, the last trading day is December 21, 2018, to select the most suitable contract according to the optimal hedging ratio.

step1: read SSE 180 Index ETF fund net and three futures contract settlement price data:

import numpy as np

import pandas as pd

data=pd.read_excel('C:/lenovo/Desktop/上证180ETF与期货合约.xlsx',index_col=0)

data.head()

Out[1]:

上证180ETF IF1812 IC1812 IH1812

交易日期

2018-04-23 3.218 3669.4 5524.0 2614.2

2018-04-24 3.278 3753.0 5681.8 2687.8

2018-04-25 3.261 3743.6 5677.4 2670.0

2018-04-26 3.216 3672.6 5598.8 2628.2

2018-04-27 3.217 3686.8 5612.6 2626.2

step2: the number generated each day for the return series:

SHre=np.log(data.iloc[:,0]/data.iloc[:,0].shift(1)).dropna()

IFre=np.log(data.iloc[:,1]/data.iloc[:,1].shift(1)).dropna()

ICre=np.log(data.iloc[:,2]/data.iloc[:,2].shift(1)).dropna()

IHre=np.log(data.iloc[:,3]/data.iloc[:,3].shift(1)).dropna()

step3: to three the number of futures contracts yield data as an argument, SSE 180 Index ETF logarithmic regression rate of return of the dependent variable respectively:

import statsmodels.api as sm

IF=sm.add_constant(IFre)

IC=sm.add_constant(ICre)

IH=sm.add_constant(IHre)

model1=sm.OLS(SHre,IF).fit()

model1.summary()

Out[3]:

<class 'statsmodels.iolib.summary.Summary'>

"""

OLS Regression Results

==============================================================================

Dep. Variable: 上证180ETF R-squared: 0.946

Model: OLS Adj. R-squared: 0.946

Method: Least Squares F-statistic: 2854.

Date: Fri, 14 Feb 2020 Prob (F-statistic): 3.31e-105

Time: 17:35:06 Log-Likelihood: 715.08

No. Observations: 165 AIC: -1426.

Df Residuals: 163 BIC: -1420.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0002 0.000 0.628 0.531 -0.000 0.001

IF1812 0.8735 0.016 53.419 0.000 0.841 0.906

==============================================================================

Omnibus: 1.256 Durbin-Watson: 2.687

Prob(Omnibus): 0.534 Jarque-Bera (JB): 0.866

Skew: 0.114 Prob(JB): 0.648

Kurtosis: 3.271 Cond. No. 65.8

==============================================================================

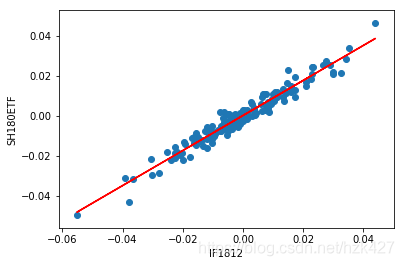

Similarly available other two futures linear regression model results, the coefficient of determination R & lt 2 were 0.72 and 0.929, most hedge ratio of 0.922 and 0.6657, respectively. In terms of R & lt 2 highest as the optimum model is selected, the security contract IF1812 contract as the most appropriate condom, R & lt 2 reached 0.946, most hedge ratio of .8735. Paint can look at fitting effect:

import matplotlib.pyplot as plt

plt.plot(IFre,model1.params[0]+model1.params[1]*IFre,'r-')

plt.scatter(IFre,SHre,marker='o')

plt.xlabel('IF1812')

plt.ylabel('SH180ETF')

Optimal number of futures hedging contracts

Then calculate how much the number of futures contracts hedgers need for hedging operations. Suppose Q S indicates the number of assets insured quilt, Q F. Represents the size of a futures contract, N * represents most futures contracts for hedging parts, then there × Q * N F. × [Delta] F = Q S × [Delta] S, substituting h * = ΔS / ΔF * = H * have Q N S / Q F. .

Connected cases, assuming that the fund company bought in December 28, 2018 in accordance with the closing net 2.768 yuan SSE 180 Index ETF billion, while the CSI 300 futures IF1901 contracts with short positions (daily settlement price of 3003.6 yuan) to set Paul, assuming optimal hedge ratios constant, seeking the best futures of contracts:

def n(h,qs,qf):

return h*qs/qf

n(model1.params[1],100000000,3003.6*300)

Out[6]: 96.9344687900856

So IF1901 contract to sell 97 copies.

Dynamic Break combined hedging

Connected cases, it is assumed that after completion of hedging, with changes in NAV and futures contract prices, the overall effect of hedging portfolio also changed, calculate the three trading portfolio hedging profit and loss information in the following table:

| date | January 11, 2019 | January 14, 2019 | January 15, 2019 |

|---|---|---|---|

| NAV (yuan) | 2.836 | 2.815 | 2.867 |

| Futures contract settlement price | 3095.0 | 3069.4 | 3126.2 |

net0=2.768;N=97;F0=3003.6;Q=100000000

net=pd.Series([2.836,2.815,2.867])

F=pd.Series([3095.0,3069.4,3126.2])

for i in range(3):

r=Q*((net[i]/net0)-1)-300*N*(F[i]-F0)#这时用一般收益率公式更合理

print('第{}个交易日套保组合的累积盈亏为{:.2f}'.format(i+1,r))

第1个交易日套保组合的累积盈亏为-203092.60

第2个交易日套保组合的累积盈亏为-216803.12

第3个交易日套保组合的累积盈亏为8929.60

Visible hedging calculate the optimal ratio not once, in order to obtain the best effect of hedging, consider creating a dynamic model of such hedging DCC-GARCH, Copula like.