"Customers are very cautious in the first half of 2023, resulting in lower than normal growth rates, but we have seen a pick-up in the second half of the year, with deliveries expected to grow 16% year-on-year in the second half of the year, much higher than in the first half." This is Mobileye The prediction at the company's semi-annual report conference recently.

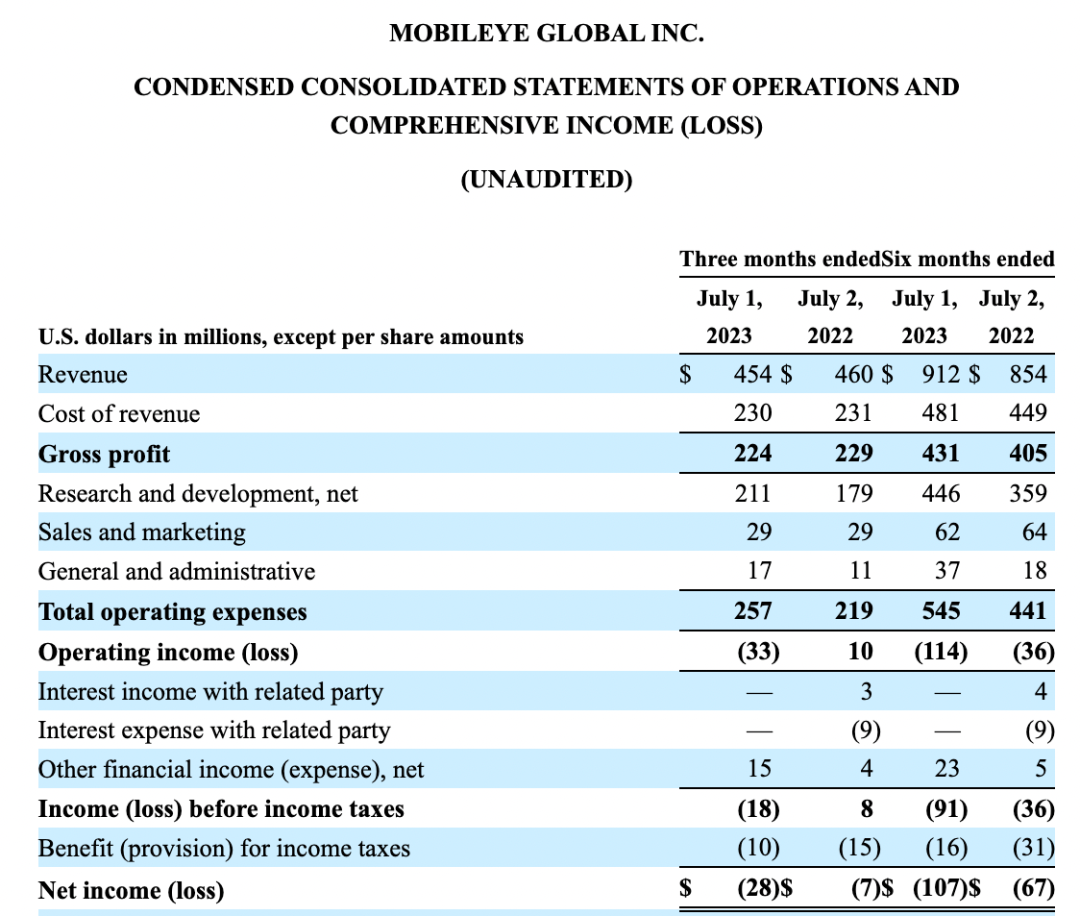

According to public data, in the first half of this year, Mobileye achieved revenue of US$912 million, an increase of only 6.79% year-on-year, far lower than the 35% in 2022. In terms of net profit, there was still a loss of US$107 million, an increase of 59.70% over the same period last year.

The data chart comes from Mobileye's 2023 semi-annual report

Among them, in terms of expenditure, Mobileye is rebuilding the strategic inventory of EyeQ series chips, consuming a lot of cash flow. At present, the company's visible customer fixed-point release expectations are: the third quarter increased by more than 10% compared with the second quarter, and the fourth quarter increased by more than 20% compared with the third quarter.

However, the company also pointed out that as some joint venture brands in the Chinese market and Chinese local new energy car companies continue to seek breakthroughs in advanced intelligent driving technology , "we are facing increasing competitive pressure."

According to the monitoring data of Gaogong Intelligent Automobile Research Institute, from January to June this year, 3.2435 million new passenger cars equipped with L2 (including L2+) equipped with pre-installed standard equipment in the Chinese market (excluding imports and exports) were delivered, a year-on-year increase of 37.65%; The equipped ratio was 34.90%, an increase of about 8 percentage points year-on-year.

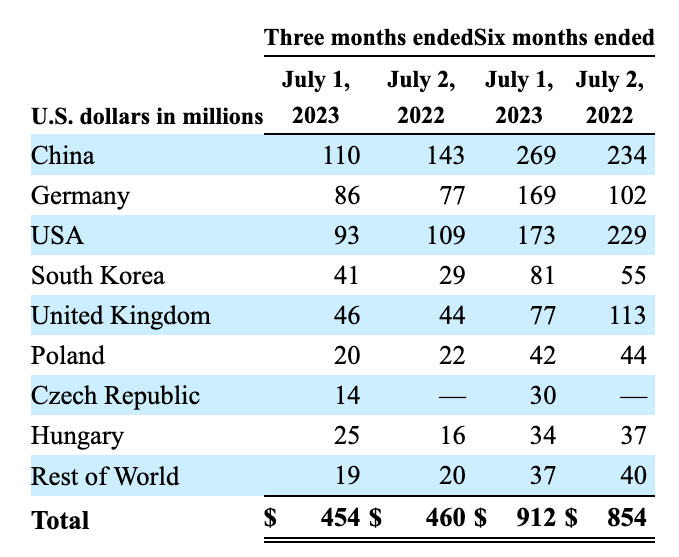

In the same period, Mobileye's revenue from the Chinese market was US$269 million , a year-on-year increase of 14.96%, failing to outperform the market. However, the proportion of revenue in the Chinese market continued to rise to nearly 30%. This means that the "win or lose" of the Chinese market is becoming more and more important to Mobileye.

Of course, the good news is that Mobileye's partners are still developing platform solutions based on the EyeQ6 series. For example, Jingwei Hengrun, which recently announced a strategic investment in Huixi Intelligent, is still actively following up Mobileye's EyeQ6/EyeQ Ultra solution.

But the bad news is that several partners, including ZF and Aptiv, are choosing the Horizon platform to develop solutions that meet the needs of customers in the Chinese market. In addition, Jingwei Hengrun and Zhixing Technology have already begun to deliver domain control solutions based on the TI TDA4 platform.

In contrast, at present, the progress of Mobileye's SuperVison high-level solution is not as expected. The company expects to have five new vehicles equipped with the solution put into production by the first quarter of 2024. This figure is far behind Nvidia and Horizon.

In addition, Mobileye also admitted that the expectations for Jikrypton 001 are too high. According to the monitoring data of Gaogong Intelligent Vehicle Research Institute, from January to June this year, 30,300 units of Jikrypton 001 were actually delivered, a decrease of about 22,300 units compared with the second half of last year.

At the same time, this week, Jikrypton announced the time-limited price rights and interests policy of the 2023 Jikrypton 001. It is determined that you can enjoy a limited-time price reduction of 30,000 to 37,000 yuan, and the price reduction rate is about 10%.

For this price reduction, Ji Krypton's vice president Lin Jinwen publicly stated, "The price cut is not to clear inventory, Ji Chlorine has never been in stock." But obviously, from the perspective of the supplier (Mobileye), the expected sales target has not been achieved.

In addition, in addition to the comprehensive and continuous coverage of Volkswagen, Toyota, and Honda, many of Mobileye's customers are entering the platform switching cycle, which is not good news for the company's future performance expectations.

For example, Nissan. Beginning this year, Dongfeng Nissan will redesign its smart driving system for its models, and Hitachi (on the Renesas platform) is taking over ZF (Mobileye).

In terms of China's independent brands, Geely is switching between Horizon, Black Sesame Smart, and Nvidia platforms. Even Jikrypton, which the founder of Mobileye participated in the investment, will also adopt Nvidia + self-developed solutions.

SAIC, Great Wall, BYD, etc. are also beginning to switch models to Horizon, and these car companies are also one of the shareholders of Horizon. In addition, manufacturers such as Black Sesame Smart and Aixin Yuanzhi will also start mass production and delivery in the second half of this year.

In addition, in June this year, Intel, the parent company of Mobileye, announced that it would sell part of its equity in Mobileye, which is expected to be worth approximately US$1.5 billion, and its shares will drop from 99.3% to approximately 98.7%.

At the end of 2021, Intel suddenly announced Mobileye’s spin-off plan, the reason given was that it “hopes to release more value to Intel’s shareholders.” Against the background of increasing competition in the automotive chip track, Mobileye’s profitability problem remains. To be solved.

Data show that in 2021, 2020 and 2019, Mobileye's annual net operating losses will be US$75 million, US$196 million and US$328 million respectively.

In 2022, Mobileye will achieve an annual revenue of US$1.869 billion, a year-on-year increase of about 35%. In the context of continuing to increase revenue, it will still maintain a loss in 2022, with a net loss of US$82 million for the year, a slight increase from 2021.

Additionally, Mobileye acknowledges that some of their competitors have more or better resources than their competitors. For example, Nvidia and Qualcomm have preemptively released cross-domain super-computing solutions for the next-generation vehicle electronic architecture.

In the Chinese market, local Chinese suppliers have begun to seize market share in the popular market below 150,000 yuan, and car companies have put more emphasis on the cost-effectiveness and openness of solutions, as well as localized Tier1 ecosystem resources. In the high-end market of more than 300,000 yuan, a variety of schemes have launched fierce competition.

Just at the beginning of this month, on August 3, Ideal L9 Pro was launched at a price of 429,800 yuan. It is equipped with the Horizon Journey 5 chip, creating the first entry of Chinese high-performance intelligent driving computing solutions into the market priced above 400,000 yuan.

When talking about the fierce competition in the current market, Mobileye’s senior executives believe that “the performance and cost of the system are the key to determining who will win.” In addition, it revealed that 4D imaging radar will be implemented in 2024 as originally planned. SOP.

Mobileye predicts that its full-year revenue in 2023 will reach US$2.07 billion to US$2.11 billion; however, there will still be operating losses throughout the year, which are estimated to be -US$98 million to -129 million.

In the view of Gaogong Intelligent Vehicle Research Institute, compared with other peers, Mobileye did not have much positive news in the first half of the year, except for the announcement that the L4 test fleet in cooperation with Volkswagen began to run. This means that the company still lacks favorable support to meet full-year revenue expectations.