The AI war between technology giants continues, and the earnings season is an important window to get a glimpse of the success of AI.

Google and Microsoft, two technology giants that compete head-on in many fields, released their financial reports on the same day. This time, compared with the previous quarter, the situation seems to have reversed.

Last quarter, Google not only successfully resisted the attack of Bing and ChatGPT, but its cloud business grew beyond expectations. However, the results of Microsoft's attack on all sides with OpenAI did not bring many surprises.

However, this quarter, although Google once again exceeded expectations and firmly maintained its basic search and advertising market, in the field of cloud computing, Microsoft's outstanding growth has made Google's performance slightly bleak, and directly led to the outside world's doubts about the quality of Google Cloud AI. After the financial report was released, the market value of Google's parent company evaporated by more than one trillion yuan in one day.

So, how does Google truly win in the AI wrestling field?

The growth of advertising business is accelerating, and the dominance of search engines is difficult to shake?

Financial report data shows that Google achieved revenue of US$76.69 billion in the third quarter, higher than analysts' expectations of US$75.54 billion, a year-on-year increase of 11%. It finally ended four consecutive quarters of single-digit growth and returned to the double-digit range. Net profit was US$19.689 billion, which was also higher than market expectations. Due to the low base in the same period last year, the year-on-year growth was as high as 41.55%. Overall, this is a relatively impressive financial report.

Specifically, the overall performance exceeded expectations, mainly driven by the strong recovery of the advertising business. The financial report shows that Google’s advertising revenue in the third quarter reached US$59.65 billion, compared with US$54.48 billion in the same period last year, accounting for nearly 80% of total revenue.

The strong growth of the advertising business is partly related to the continued improvement of the economic environment and the increase in advertising budgets by advertisers. Data show that overall U.S. media advertising spending began to rebound in the second half of the year after experiencing sluggish growth in the first two quarters. In the latest forecast released recently, Magna has raised its advertising growth guidance for the U.S. market in 2023 and 2024, predicting that advertising expenditures will grow by 5.2% in 2023 and will increase advertising expenditures in 2024 from 5% to 5.6%.

Against this background, Meta advertising business, which also belongs to the online digital advertising category, has also recorded rapid growth. Financial report data shows that due to its coverage of multiple sectors with growth dividends such as social media and short videos, Meta’s advertising business grew at a year-on-year rate of 23% in the third quarter, which is more eye-catching than Google.

On the other hand, it is driven by the synergy of search engines and streaming platform YouTube. The financial report shows that the growth of these two major sectors in the third quarter exceeded expectations. Among them, Google search advertising revenue increased by more than 11% year-on-year, and YouTube advertising revenue increased by 12% year-on-year.

Specifically, Google search still accounts for the majority of the company's advertising business revenue structure, contributing 74% of revenue in the third quarter, and its dominance is stable, with a global market share of as high as 90%. While the search engine business has entered a stable period and is facing the challenge of generative AI, the growth rate can outperform the market, which once again proves that Bing+ChatGPT's offensive is still unable to shake the dominance of Google search.

In this regard, Microsoft CEO Satya Nadella also personally admitted that when Microsoft introduced ChatGPT to Bing in February this year, it had hoped to increase its search market share of only 3% at the time. "I started to think that maybe I would "With a 3.5% share", but eight months later, such hopes ultimately came to nothing, and Microsoft's share of the search market has not changed significantly.

The key reason is that on the one hand, users have long-term usage habits, which determines that unless there is obvious improvement in performance and experience, it is difficult to trigger user migration; on the other hand, generative AI is still in the early stages of development, and its The stability and accuracy need to be improved, and it cannot replace search engines.

In addition, the improvement of the streaming media platform YouTube is also indispensable. According to Nielsen data, YouTube ranks first in time share, and its YouTube Shorts, which competes with Tik Tok, officially launched commercialization this year, which has promoted the Segment revenue continues to grow.

However, the overall performance and the unexpected growth of its main business did not convince the capital market. On the day the financial report was released, Google's stock price plummeted, and its market value evaporated by 1.2 trillion yuan in a single day, which was the fifth largest single-day loss in the history of a U.S. listed company. The reason why the capital market is bearish is that the cloud business, which carries Google's second growth curve, has not grown as fast as expected. Especially compared with Microsoft, which released its financial report on the same day, its performance is not impressive.

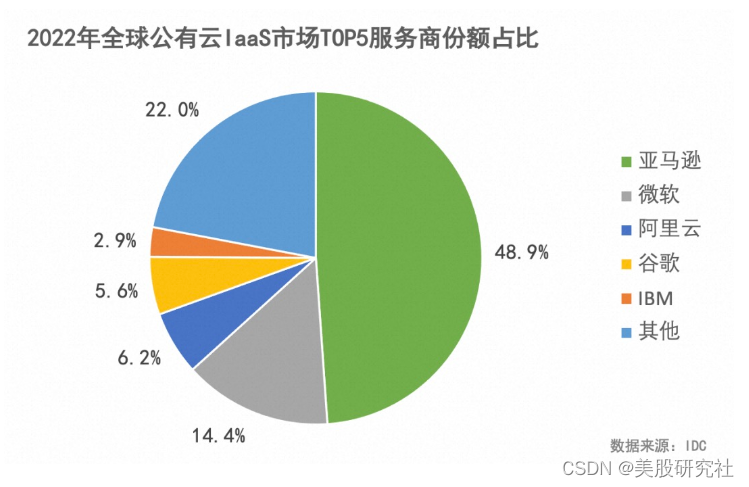

Financial report data shows that in the third quarter, Google Cloud business achieved revenue of US$8.41 billion, lower than market expectations of US$8.6 billion, with a year-on-year growth rate of 22%, lower than market expectations of 25.3%. Moreover, cloud business growth has continued to decline for several quarters. The financial report shows that from the third quarter of 2022 to the second quarter of 2023, the growth rates of the cloud business segment were 38%, 32%, 28%, and 28% respectively. In contrast, Microsoft Azure cloud performed brilliantly in the third quarter, with a year-on-year growth of 29%, sweeping away the weak trend in the previous quarter.

So, in this situation, how can Google regain the certainty of growth?

Cloud business growth is slower than expected. Is Google AI viable?

At this stage, generative AI has injected new growth momentum into cloud computing. Since Google is a technology giant with deep accumulation in the field of AI, the capital market is also full of expectations for its use of AI to accelerate the development of cloud computing business. However, the plunge in Google's stock price after the release of its earnings report seems to indicate that investors have gradually lost patience with companies that fail to realize the ability of AI to make money. However, based on the specific situation, there is no need to panic too much about Google’s AI progress not being as good as expected.

In rough comparison, the rapid growth of Microsoft Azure Cloud shows obvious AI pull, while the weak growth of Google Cloud seems to be due to insufficient AI pull. But when it comes to cloud computing business specifically, there are obvious differences in the customer composition and business conditions of the two, which determines that in the AI era, the growth of the two may not necessarily be completely synchronized.

Looking back, Google Cloud can be said to be a pioneer in the cloud business. The reason why it has not caught up with Amazon and Microsoft is mainly due to its inherent business model that relies too much on traffic monetization and its lack of ToB genes. Moreover, in the cloud computing business While progress was slow, Google even considered withdrawing from the cloud market entirely.

This inherent shortcoming of B-side thinking and the vacillating attitude in strategy led to the fact that although Google later decided to catch up after reflection, in a situation where most of its major customers have chosen Amazon and Microsoft, which are more certain, Google Cloud can obtain are mainly small and medium-sized customers, including many start-up companies.

Therefore, although Microsoft and Google are also exploring the growth space of the cloud business, in specific cases, the focus of the two is obviously different. Microsoft focuses on core large customers who already use many of its own software services, while Google places its hopes on in start-ups. In addition, in the current environment where the economic recovery is still climbing, cloud computing expenditures mainly come from large enterprise customers, while small businesses are reducing expenditures. This naturally determines that Microsoft can realize the cloud computing growth brought about by AI one step ahead of Google. dividend.

However, as the global economy continues to recover and generative AI technology continues to mature, small and medium-sized enterprises are bound to gradually increase cloud computing-related expenditures, and Google Cloud may usher in a period of dividend redemption.

In addition, since Google Cloud changed its leadership in 2019, a series of drastic reforms have not only strengthened the ToB service team, but also allowed Google Cloud to gradually accumulate differentiated advantages in competing for large customers.

At present, Google's main differentiating advantage lies in its open source strategy. The open source strategy can make full use of Google's own accumulated business resources, and also points directly to the future of cloud computing and AI.

Specifically, with the development of cloud computing, after the infrastructure at the IaaS level has become more complete, services at the PaaS layer and SaaS layer have become the key to attracting customers. At this stage, building an ecosystem through collective collaboration and common wisdom has become a top priority. heavy. As Meta once said: "We believe that an open source approach is the right way to develop today's artificial intelligence models, especially in the generative field where technological advancements are advancing rapidly."

As of now, Google has mastered more than 2,000 open source projects, from the TensorFlow machine learning library to the popular Kubernetes cloud native development platform. These are attractive and high-quality resources for the business side. It is worth mentioning that Microsoft, which had previously lacked interest in open source, has also begun to focus on open source. It is understood that Microsoft has reached an in-depth technical cooperation with Hugging Face, an open source model library company, to expand the support scope of ONNX Runtime.

However, in terms of open source, Google obviously has a stronger first-mover advantage and focus, and therefore its attraction to customers continues to increase. For example, Microsoft Cloud's major customer Verizon moved to Google Cloud, which is an example.

In addition, Google’s investment in AI continues to increase. At the beginning of this year, Google announced that it would lay off 12,000 office workers. However, judging from the third quarter data, the number of employees has rebounded from the previous quarter. At this time, it began to increase personnel investment, which is generally believed to be used to improve the research and development capabilities of the AI team. According to another financial report, Google’s capital expenditures in the third quarter were US$8.06 billion, most of which were investments in technology infrastructure, reflecting Google’s continued efforts in artificial intelligence computing.

Overall, Google is still in an upward period that can give the market a lot of confidence and expectations. On the one hand, Google's search dominance is still hard to shake, and its basic advertising business also maintains its dominant position, which is expected to bring continuous cash flow to Google; on the other hand, although the development curve of the cloud business has fluctuated, it will still be combined with the company's own advantages and Judging from the continued increase in investment, the real value may be blooming in the near future.

Author: Jianbai

Source: US Stock Research Institute