KK Group launched the third shock on its IPO road.

Recently, KK Group updated its prospectus and continued to promote the listing process on the Hong Kong Stock Exchange. After the previous two listings were shelved, there was finally a new trend. Judging from the updated content, the prospectus of KK Group disclosed the company's latest performance as of the first quarter of 2023, and handed over a good "report card": in the first quarter of 2023, the company achieved revenue of 1.446 billion yuan, a year-on-year increase of 4.785 billion yuan. %; the group's operating profit was 131 million yuan, and the operating profit rate was 9.1%, which sent a positive signal to the market.

From the perspective of the purpose of raising funds in the prospectus, KK Group is still determined to expand its stores and further increase its market penetration. It is undeniable that store expansion is a necessary action for most retail companies to seize the market, but the operating pressure brought by KK Group's strengthening of store expansion is obvious, and to a certain extent blocked its road to listing. And after the "respite", KK Group continued to promote the store layout, how to tell the growth story well?

KK Group's trendy retail business, success stores, failure stores?

Established in 2015, the KK Group has grown under the rise of Generation Z and new consumption concepts. The dividends of the times have undoubtedly provided a fertile ground for the development of the KK Group, and it has also embarked on a promising track.

Data show that my country's fashion retail market has developed rapidly in recent years, and the market size has increased from 151 billion yuan in 2017 to 253.4 billion yuan in 2021, with a compound annual growth rate of 13.8%. It is expected to reach 540.3 billion yuan in 2026. Such a broad space for industry growth has created many trendy retail companies such as MINISO, Bubble Mart, and KK Group.

Among them, KK Group has occupied a certain market share mainly by building a brand matrix and expanding its offline store network at a high speed. It is understood that KK Group currently owns four major retail brands, KKV, THE COLORIST, X11, and KK Pavilion, and has more than 696 stores in more than 190 cities in 31 provinces of my country and 22 cities in Indonesia. Based on this, in terms of GMV, KK Group will become one of the three major lifestyle consumer goods trend retailers in my country in 2022, and it will gradually catch up with the top companies in the industry and enter the leading ranks.

In addition, the network layout of offline stores also escorts the revenue growth of KK Group. According to the prospectus, from 2020 to 2022, KK Group's revenue will be 1.646 billion yuan, 3.524 billion yuan, and 3.551 billion yuan respectively. However, judging from the data, the supporting effect of scale expansion seems to have gradually weakened in recent years, which is closely related to the industry background. In 2022, under the influence of multiple factors, the total retail sales of consumer goods in my country will decrease by 0.2% year-on-year, and the retail sales of consumer goods other than automobiles will decrease by 0.4% cumulatively. It can be seen that under the downward trend of the industry's prosperity, it is commendable that KK Group can achieve positive revenue growth by virtue of its scale advantage.

But what is more worrying about the development of KK Group is its profitability problem, that is, the large-scale store operation leads to a relatively large operating burden. According to the prospectus, KK Group's sales and distribution expenses are mainly related to store investment. From 2020 to 2022, this expense will account for 24%, 31.1%, and 37% of total revenue respectively; KK Group has accumulated losses of more than 7 billion yuan in the past three years.

From the perspective of the industry, the growth path of other fashion retail companies is actually similar to that of KK Group, but there is no such significant profit pressure. For example, MINISO, as of Q2 of fiscal year 2023, the number of MINISO stores is 5,440, an increase of 395 compared with the same period in 2021, and an increase of 144 from the previous quarter. The continuous expansion of offline scale has not lowered the profit level of the enterprise. In Q2 of fiscal year 2023, MINISO’s adjusted net profit was 370 million yuan, a year-on-year increase of 82.1%; operating profit was 450 million yuan, a year-on-year increase of 75.2%.

On the whole, in the new consumer retail industry, KK Group and MINISO have completely different profit performances. Why?

The root of the problem may still need to return to the store expansion model. In comparison, MINISO mainly relies on third-party franchising to expand its stores, showing the characteristics of "light assets", while KK Group focuses on the direct sales model of large stores, with immersive shopping experience, trendy and creative space layout, and the taste of the Z generation. The selection of products has attracted a large number of young consumers, but at the same time, the more "heavy" business model has made it difficult for KK Group to escape losses. Moreover, the operation of large stores can easily lead to high floor efficiency and high inventory, which also means greater risks for franchisees. Therefore, the franchise model that reduces capital occupation and realizes brand expansion is hindered by KK Group.

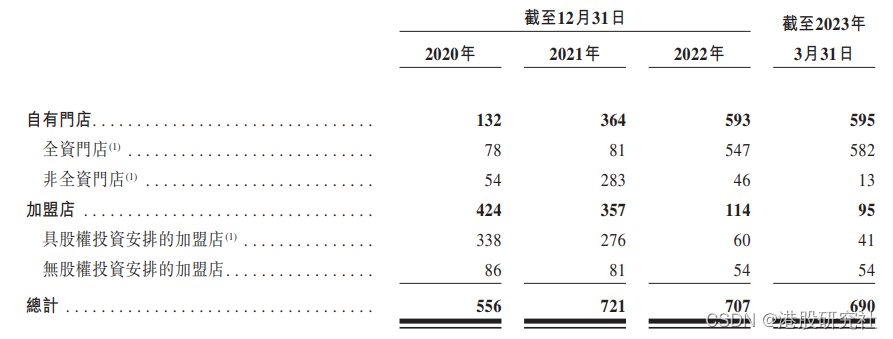

The data shows that from 2020 to March 31, 2023, KK Group has 556, 721, 707, and 690 stores respectively. Among them, the number of self-owned stores is 132, 364, 593, and 595 respectively; the number of franchised stores has decreased significantly, respectively 424, 357, 114, and 95.

In the case of failure in the transformation of the store business model, KK Group may be able to take more direct measures such as raising prices and slowing down the pace of scale expansion to expand profit margins and control costs. But combined with the actual situation, the feasibility is difficult to grasp.

First of all, from the perspective of pricing level, MINISO focuses on low-price and sinking market strategies, and has won a lot of loyal consumers in the early stage, while KK Group, such as KKV, has the temperament of "Internet celebrity" and is deeply involved in the first- and second-tier cities. The cost performance advantage of its brand products is not outstanding. If the price is raised rashly, it may only get further and further away from consumers. In terms of slowing down the pace of store expansion, the relevant results have been verified in the first quarter of 2023. In the first quarter of this year, KK Group only opened 4 new stores and closed 22 stores, thus achieving an adjusted net profit of 86 million Yuan, turning losses into profits.

However, with the continuous expansion of the market and more and more entrants, especially under the momentum of MINISO's slogan of "hundreds of countries and hundreds of billions of stores", the urgency of KK Group's expansion is becoming more and more obvious. The prospectus discloses that KK Group not only plans to open 250-300 new stores in 2023, but also plans to open 250 stores in 2024 and 2025, and most of them are self-owned stores. Future development pressure has already emerged.

Generally speaking, KK Group has always faced the contradiction between the expansion of stores and the increase of operating burden and inherent profit needs. From the perspective of the company itself, this contradiction may be due to its lack of competition barriers, and it can only start with scale Shaping consumer perceptions. Based on this, with a long-term perspective on development, if KK Group wants to achieve real growth, it needs to conduct more in-depth exploration on the issue of "how to build a moat and achieve sustainable development".

To tell a good growth story, building a moat is the key?

For KK Group, it is not easy to tell a good growth story in the future.

It can be seen that behind its insistence on store expansion and large-scale store operation, on the one hand, it is because under the fierce competition situation, there are no high competition barriers in terms of products. Compared with MINISO and other brands that are actively building their own IP, KK The group currently owns mostly "Internet celebrity" products, third-party brand products, etc., lacking product innovation.

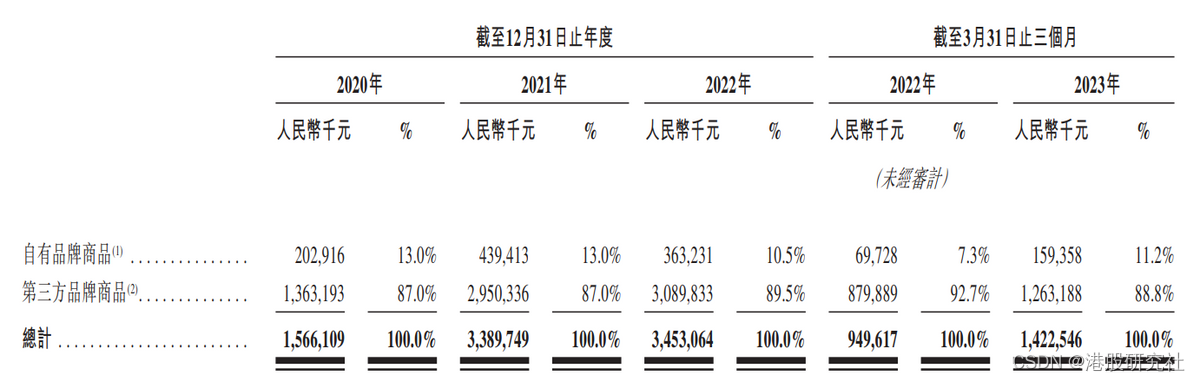

The data shows that as of the first quarter of 2023, nearly 90% of KK Group's revenue comes from third-party branded products, and the revenue from its own brand products has dropped from 13% in 2020 to 11.2%.

However, the gross profit margin of its own brand products is much higher than that of third-party products. According to data, in 2022, the gross profit margin of KK Group's own brand products will be 52.3%, while the gross profit margin of third-party brands will only be 36.8%. It can be seen that the profitability of KK Group is difficult to improve, and it is also closely related to its product structure.

On the other hand, a major drawback of the collection store model is that it is easy to replicate and highly replaceable. In recent years, cutting-edge collection stores such as Healthy Planet, HEAT, Jupiter Yutang, and HAYDON Black Hole have emerged in the market, most of which carry similar labels such as "net celebrity check-in" and "immersive scene". In this case, the lack of product competition barriers, KK Group may face a huge impact.

It is worth mentioning that the fashion retail business is also facing more prominent market changes. The target consumer group, Generation Z, pursues trends, and their interests and hobbies change rapidly. If brands do not keep up with the trend changes, it will be difficult to form competitiveness in the fierce competition to seize consumers' minds.

So, in the face of an unknown future, how does KK Group find its own position and form a moat?

In fact, looking at the trendy retail industry, most of the brands that can win the favor of capital and consumers have their own "hard work". For example, MINISO's transition from a channel brand to a product brand is inseparable from strong supply chain management capabilities. , cost control capabilities, and continuous promotion of IP research and development, joint name and other actions. Bubble Mart has a greater say in IP hematopoietic capabilities. The seven major IPs headed by MOLLY will each achieve revenues exceeding 100 million in 2022, supporting most of the company.

For KK Group, in order to open up the future growth path and solve the current problems, it still needs to reduce its dependence on third-party products, strengthen its own IP creation and logistics supply chain management capabilities, so as to improve the sustainability of profitability.

Judging from the current development plan of the KK Group, in addition to continuing to accelerate store expansion, it also plans to continue to optimize logistics and supply chains, and improve the level of system automation and intelligence. In terms of IP development, although there is no clear plan to disclose, judging from KK Group’s previous initiatives such as jointly building an IP ecological chain with Moyan Gongshe, KK Group’s future product innovation may bring new surprises to the market.

However, as the 28th effect of the fashion retail industry becomes more and more obvious, leading brands have more and more resources, KK Group also needs to accelerate the pace of building a moat, so that it is expected to get rid of the growth dilemma and play a more important role in guiding the consumption trend role.

Author: Helen

Source: Hong Kong Stock Research Institute