Friends who are options, please take a look! Specific brokerages currently cooperating with Nuggets Quantification have been able to support option data and trading interfaces~ If you need to carry out option quantification, please contact me for more details.

In this issue, we will share a strategy with you and introduce how to use options for automated arbitrage .

Futures spot arbitrage refers to a certain futures contract. When there is a price gap between the futures market and the spot market, the price difference between the two markets is used to buy low and sell high to make a profit.

However, the price of first-hand futures is often very expensive . Take SSE 50 stock index futures as an example:

The current one-hand IH2205 is about 2800 points, the contract multiplier is 300 yuan per point, the first-hand market value is equal to 2800*300, up to 840,000 yuan, the exchange margin is 12%, and the first-hand margin is equal to 840,000 yuan*0.12%=100,800 Yuan.

It can be seen that the capital requirements of stock index futures are high, and the utilization rate of funds is low.

In contrast, options are very advantageous. If you are a buyer, you only have rights but no obligations, and you only need to pay a premium, and you don’t need to pay a deposit at all; The calculation of margin is more complicated. According to experience, except for deep real-value options, the general margin is below 1W.

In this way, the threshold for trading with options instead of stock index futures is relatively lower, and the utilization rate of funds is higher .

However, since it is relatively difficult to sell spot ETFs at present, the strategy we share is mainly to hold long positions in the spot market and carry out arbitrage in the form of options synthetic futures short positions.

So, how to use options to synthesize short positions in futures? Answer: Buy a put option and sell a call option at the same time .

The strategy idea is as follows:

1. Traversing all options under the strike price, constructing futures short positions, and calculating the value of the short position portfolio;

2. Calculate the arbitrage space and find the combination with the largest price difference between the futures short position and the spot long position;

3. Trading: long spot (buy 10,000 ETFs), short futures (buy 1 put option, sell 1 call option);

4. When there is a larger difference, actively update the position; when the combination price difference decreases to below 0, or on the expiration date of the option, close the position and leave the market.

Note: The calculation of arbitrage space needs to take transaction fees into account.

Option commission: price×volume * multiplier * backtest_commission_ratio + volume * backtest_commission_unit,

ETF commission: price*volume*backtest_commission_ratio, where price is the transaction price, volume is the transaction volume, multiplier is the option contract multiplier, backtest_commission_ratio is the backtest commission ratio, and backtest_commission_unit is the backtest fixed commission (yuan/unit). The default commission ratio is 0.0001, and the fixed handling fee (yuan/contract) is 1.

Policy parameter settings:

-

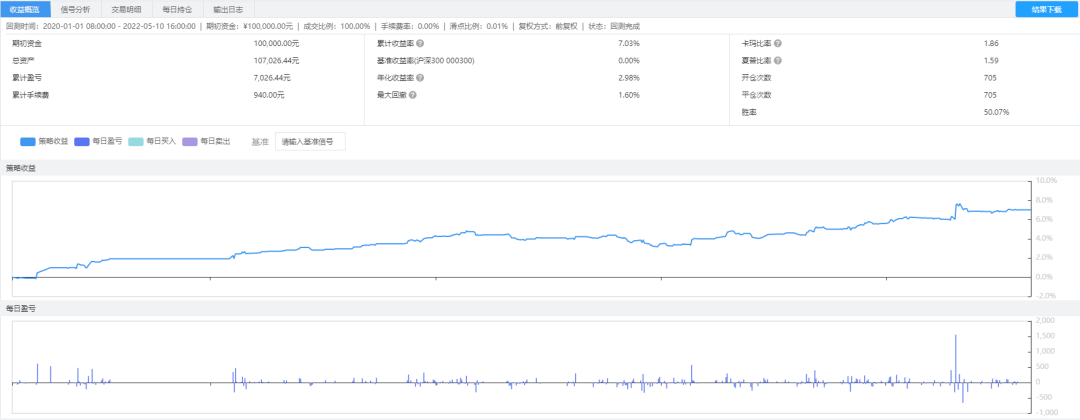

Initial capital: 100,000

-

Backtest varieties: SSE 50ETF (510050) and its option contracts

-

Backtest period: January 1, 2020 - May 10, 2022

The backtest results are as follows:

According to the backtest results, we can see that from the beginning of 2020 to May 10, 2022, the annualized rate of return of the strategy is 2.98%, the maximum retracement is 1.60%, the Sharpe ratio is 1.59, the winning rate is 50.07%, and the number of transactions is 705 . From the perspective of strategy performance, the strategy fluctuates little, and the net worth curve rises steadily.

It should be noted that this strategy uses daily frequency data. In theory, it can capture the price difference in a more timely manner when used on high-frequency data such as minute frequency. At the same time, the setting of commission and handling fee is relatively simple, and interested friends can further Adjust parameters and optimize strategies.

The source code of the strategy has been shared with the Quantitative Nuggets community. If you need it, you can go to the link below to pick it up.

Portal: https://bbs.myquant.cn/thread/3291

Disclaimer: This content is original by Nuggets Quantitative, for learning, communication, and demonstration purposes only, and does not constitute any investment advice!