Is Baidu finally going to drink the "Hong Kong stocks" medicine in 2021?

Recently, a number of media reports stated that Baidu plans to go public in Hong Kong as early as the first half of 2021 and raise at least US$3.5 billion. It is reported that Baidu has hired CITIC Lyon and Goldman Sachs to assist in the Hong Kong listing. This shows that Baidu's return to Hong Kong for listing may have already been finalized.

So, Baidu, which has been undervalued by the U.S. stock market, can solve the worries over the years by drinking the "Hong Kong stocks" medicine? Today, the search era has come to an end, and Baidu, which has "stalled" in the mobile Internet era, can borrow Hong Kong to reverse the trend?

2021, Baidu's "Great Comeback"

The second listing in Hong Kong is Baidu's trump card and a long-cherished wish for many years.

There have always been rumors about Baidu's second listing in Hong Kong. In May 2020, it was reported that Baidu was considering delisting from Nasdaq. Baidu responded as "a rumor", but then Baidu Chairman Robin Li publicly stated that "Baidu is considering a second listing in Hong Kong." In July of the same year, According to media reports, Baidu has launched a listing plan to return to Hong Kong; in October 2020, there are also reports that Baidu plans to complete the listing before the end of the year.

In addition, as early as 2018, Robin Li once said, "I went to the U.S. to list because the policy did not allow it, but when the policy allowed Baidu to come back, I definitely hoped to be able to come back to the domestic stock market as soon as possible."

It can be seen that returning to Hong Kong is Baidu's long-cherished wish. Moreover, after the reflow of concept stocks in 2020, it is certain that the time to return to Hong Kong for a second listing has already arrived.

So, what is the market's view on Baidu's return to Hong Kong? After the second news of Baidu's return to Hong Kong on January 7, US stocks closed on January 7, Eastern Time. Baidu's stock price rose 1.92% to US$207.890, with a total market value of US$70,096.2 million. It can be seen that the market is optimistic about Baidu's return to Hong Kong.

In addition, it is not unreasonable for Baidu to return to Hong Kong for the second listing, as can be seen from the stock price changes of Baidu, Ali and Tencent since they went public. Baidu's stock price chart is showing a declining trend, while Ali and Tencent are obviously climbing. It can be seen that Baidu has not had a good time in the US stock market in recent years and has been underestimated by the Wall Street market.

Screenshot from: Futu Niuniu

In 2020, the return of NetEase and JD.com to Hong Kong has led to a wave of return of Chinese concept stocks. At the beginning of the new year, if Baidu is the first to return to Hong Kong or also set off a wave of return of Chinese concept stocks, there is also news that Ctrip plans to return this year. Hong Kong listed.

Baidu's A side

From BAT to MAT, Baidu has nowhere to tell. In recent years, Baidu has been frequently challenged or even surpassed by Internet "post-waves" such as JD.com, Pinduoduo, Meituan, and Bytedance. Although the capital market still refers to Baidu, Alibaba, and Tencent collectively as BAT, Baidu has fallen behind." fact".

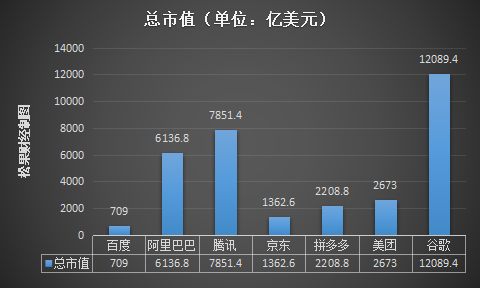

According to Futu Niuniu statistics, as of January 7, 2021, Baidu's total market capitalization is US$70.9 billion, far less than Alibaba, JD.com, Pinduoduo, Tencent, and the same search engine Google.

The search era belonging to Baidu has long ended, and BAT has been replaced by MAT in the mobile Internet era.

So why did Baidu fall behind?

Baidu is under two pressures: on the one hand, revenue growth is slowing; on the other hand, it is the pressure of cost and expense growth. After the company implemented the cost reduction and efficiency increase plan, the overall revenue situation is still in a state of sluggish growth.

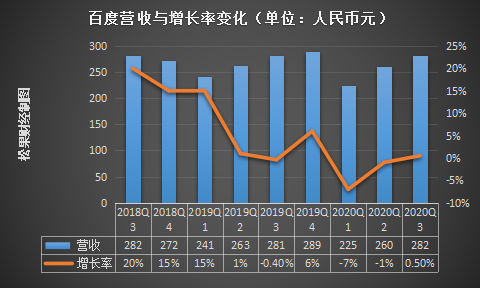

Financial report data shows: Baidu’s Q3 revenue in 2020 was 28.2 billion yuan, a year-on-year increase of 1%; in fact, from the listing of Baidu in 2005 to 2018, Baidu’s revenue has maintained a growth rate of more than 20 % year after year , reaching the fastest By 170%.

In addition, under the slowdown in revenue, Baidu experienced its first loss year. In Q1 of 2019, Baidu lost 327 million yuan, a year-on-year decrease of 104.89%. The reason is mainly due to the continuity of costs and the increase in one-time expenses. The content cost in the quarter was 6.157 billion yuan, a year-on-year increase of 47%. This cost accounted for 25% of operating costs.

Furthermore, Baidu’s performance in reducing costs to increase revenue in 2020 is obvious. From Q1 to Q3 of 2020, Baidu’s three expenses (marketing, administration, and R&D) total 8.29 billion yuan, 9.26 billion yuan, and 9.3 billion yuan, with a year-on-year growth rate of -18.84%, -7.23%, 0.92%. However, the slowdown in revenue growth has not yet eased.

The "true culprit" that caused Baidu to fall behind may be in the following aspects:

1. In the context of the ebb of the search era and the rise of the mobile Internet era, Baidu's two core business search and information flow increase gradually peaked. In addition, Bytedance has become the number one enemy of Baidu's core business, further suppressing the growth of Baidu's core business. However, under the change of traffic path in the mobile era, Baidu has not kept up with the rhythm of the times, leading to a serious departure.

2. In the search era, Baidu’s over-commercialization has also resulted in damage to its brand image , while Baidu’s advertising revenue mainly comes from the search’s bidding ranking model, but under the chaos of this model, the scandals caused damage to the brand image of Baidu , And now the haze is lingering. The Wei Zexi incident is a typical example. Nowadays, the problem of Baidu search bid advertising still exists.

3. Because the main search business cannot keep up with the times, Baidu is moving towards diversification, but the results are too late and insufficient. Baidu has frequently carried out diversified layouts over the years, experimenting with areas including e-commerce, payment, social networking, games, O2O, artificial intelligence, and autonomous driving. Among them, e-commerce, payment and social Baidu were not effective, let alone compete with the leading brands in the field, Ali and Tencent; and the O2O field also missed, and eventually sold Baidu Waimai and Qunar.

4. In addition, Baidu's internal turmoil has continued, and executives have frequently resigned. In August 2020, Wu Haifeng, former vice president of Baidu, and Sun Wenyu, former executive director of Baidu, joined Bytedance. News of frequent changes in executives is bound to affect the company's internal development and the implementation of the next strategy.

It can be seen that Baidu has "left behind" under the mobile Internet, and the previous multi-service attempts have also failed; however, Baidu now has artificial intelligence and autonomous driving services. Is this an opportunity for Baidu to stand up? ?

Baidu's B side

Over the years, Baidu has been in a "mercurial retrograde", but looking back on Baidu's 2020, it seems to be particularly quiet, as if waiting for an opportunity to comeback.

In 2020, in addition to Baidu, when Internet giants such as Alibaba, JD.com and Meituan are focusing on the "vegetable basket", what is Baidu doing? It is doing artificial intelligence, autonomous driving, new energy vehicles, etc., and it wants to rely on science and technology to gain an opportunity to stand up.

As early as June 2016, Baidu Chairman Robin Li identified AI as a company-level strategy at the company's alliance summit. Later, in 2017, he hired "Arabic" Lu Qi and put forward the "All in AI" slogan to help Baidu change.

At present, artificial intelligence has become Baidu's label , and Baidu is also the earliest Internet manufacturer in the domestic BAT to carry out artificial intelligence transformation. Today, Baidu, Google, Microsoft, and Amazon are the four major AI giants globally recognized.

In addition, Baidu has new energy and autonomous driving technologies. Among them, Baidu's autonomous driving technology is in a leading position in the world. According to the self-driving competitiveness list released by the international authority Navigant Research, Baidu, Waymo, Cruise, and Ford Autonomous Vehicles are included in the first echelon.

At the same time, Baidu's Apollo autonomous driving business is also accelerating its landing . In April 2020, Baidu's Apollo Robotaxi autonomous driving taxi has already landed in Changsha. Up to now, Baidu has established cooperative relationships with nearly 200 major companies in the global automotive ecosystem, and has more than 1,900 global patent applications for autonomous driving, ranking first in China.

Nowadays, Baidu's deep cultivation of technology may have achieved initial results. Recently, it has also been praised by the CCTV media, while other Internet giants are facing anti-monopoly turmoil due to their "vegetable basket" focusing on the people.

Therefore, in the second half of 2020, Baidu's stock price began to "recover", and it began to be rated as "Strong Buy" by many investment research institutions at home and abroad. All this is attributed to the start of the growth of Baidu's core business in the mobile ecosystem and the accelerated implementation of artificial intelligence and other businesses and favorable policies.

However, this is another long road in artificial intelligence and autonomous driving.

As we all know, artificial intelligence and autonomous driving are difficult to develop, the cost of research and development is also high, the scene is insufficient, and the implementation is difficult. In addition, the competition between AI and autonomous driving is equally fierce, and it is not yet known who can dominate the market in the future.

For example, in the field of smart speakers, although Baidu's smart speaker Xiaodu has become the top three in the domestic market, Internet giants are closely watching this market, including foreign Google and Apple, domestic Ali, Xiaomi, Jingdong, etc.; and In the field of autonomous driving, now not only Ali and Tencent have entered the game, but also traditional car companies and emerging car companies are gearing up.

On the whole, Baidu is focusing on artificial intelligence, but the end of this long road is not yet known, but it is foreseeable that Baidu will move in this direction and more and more supporters. So, will the return to Hong Kong bring any new stories to Baidu? Can you help Baidu fight a beautiful turnaround?

Will it be possible to fight a beautiful "turn over" when returning to Hong Kong?

Returning to Hong Kong to be listed may not cure Baidu's "illness", but it may save Baidu's "life".

For Chinese concept stock companies, the benefits of returning to Hong Kong for listing are in two aspects: on the one hand, it raises funds to invest in the company's business, and increases the liquidity of stock exchanges, thereby prompting a rapid increase in the stock prices of listed companies returning to Hong Kong. For example, after NetEase and JD returned to Hong Kong last year, their share prices have increased significantly.

On the other hand, returning to Hong Kong for listing can be closer to the local market, and there will be more RMB investors, and these investors are often more familiar with the business of Chinese companies, and everyone can understand the company's value and market position from more dimensions.

At a time when Baidu heavily bet on technology and artificial intelligence, Baidu's market value has always been underestimated by the market. According to the "2020-2021 China Artificial Intelligence Computing Power Development Evaluation Report" released by the global market analysis agency IDC, China's artificial intelligence infrastructure market will reach 3.93 billion US dollars in 2020, a year-on-year increase of 26.8%; China's artificial intelligence is expected to be 2021 The overall market size is about 6.3 billion U.S. dollars and will reach 17.2 billion U.S. dollars in 2024.

It can be seen that the track that Baidu is developing has great potential. In addition, Baidu's autonomous driving technology ranks first in China, which also determines its chance of returning to the first echelon of the Internet in the future.

It can be seen that Baidu can enjoy a higher valuation premium by returning to Hong Kong to get listed, and get rid of the worries of being undervalued by the US stock market in recent years. In addition, the all-weather stock circulation system formed on the basis of being close to domestic investors, Baidu's stock activity may also be greatly increased to promote the development of local business, and also a lot of gains for the return of funds.

But risks and hidden dangers also exist. The closer you are to the Chinese market, it also means that the public opinion environment will have a greater impact on Baidu. The negative influence of public opinion brought about by Baidu’s previous Wei Zexi incident and the public opinion brought about by frequent changes in executives will affect the fluctuation of stock prices.

In the future, can Baidu stabilize the Hong Kong stock market, prevent the difficulties and public opinion in the "mercurial retrograde" period from further affecting the company, and let the diversified development of artificial intelligence and autonomous driving help companies fight a beautiful turnaround , Let us wait and see.

Author: Yexiao An

Article source: Songguo Finance, please indicate the copyright for reprinting.